Investors looking for a disciplined, long-term method for choosing stocks frequently use the ideas of famous fund manager Peter Lynch. His plan, explained in his book One Up on Wall Street, centers on finding companies with good, lasting growth that are available at sensible prices. It is a traditional "growth at a reasonable price" (GARP) method, mixing parts of growth and value investing. The central thought is to locate profitable, financially sound businesses that are increasing earnings at a steady rate—not a very fast, unstable speed—and to buy them when their price, compared to that growth, seems appealing. A stock filter built on Lynch's guidelines can help find such prospects, and one firm that recently met this filter is Valmont Industries (NYSE:VMI).

Examining Valmont Industries

Valmont Industries is a producer making necessary goods and services for infrastructure and farming areas. Based in Omaha, Nebraska, the firm works through two primary parts: Infrastructure, covering utility, lighting, transportation, and communications products, and Agriculture, where it is a top maker of center pivot and linear irrigation systems. This operational design, centered on important but often "ordinary" fields like utility support and farm irrigation, fits with Lynch's liking for clear companies in stable businesses. The company's goods are fundamental to modern agriculture and construction, pointing to a lasting need that is not tied to temporary consumer trends.

How Valmont Fits Important Lynch Guidelines

The Peter Lynch filter uses particular financial tests to find companies with the correct profile for long-term investment. Valmont Industries satisfies these central requirements, which are made to locate expanding, profitable, and financially stable businesses at a fair price.

- Lasting Earnings Growth: Lynch wanted companies with a confirmed history of growth, but he was cautious of extreme growth that could not continue. The filter needs a 5-year average yearly EPS growth between 15% and 30%. Valmont's EPS has increased at an average speed of 22.99% over the last five years, putting it directly within this preferred band. This shows a good and regular rise in profitability.

- Sensible Price Compared to Growth: Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock by including its earnings growth. A PEG ratio of 1 or below is seen as good, hinting the market may not be completely valuing the company's growth path. Valmont's PEG ratio, using its past five-year growth, is 0.87, indicating a possibly sensible price when its historical growth is reviewed.

- Good Profitability: Lynch preferred companies that effectively produce profits from shareholder equity. The filter requires a Return on Equity (ROE) above 15%. Valmont's ROE of 19.85% easily passes this limit, showing management is successfully using invested money to create earnings.

- Stable Financial Condition: To limit high risk, the method stresses companies with good balance sheets. Two key tests are a Debt-to-Equity ratio below 0.6 and a Current Ratio of at least 1. Valmont shows careful financial management with a Debt-to-Equity ratio of 0.49 and a solid Current Ratio of 2.35. This signals a sound balance between debt and equity funding and a good ability to meet near-term responsibilities.

Fundamental Condition Review: A Summary

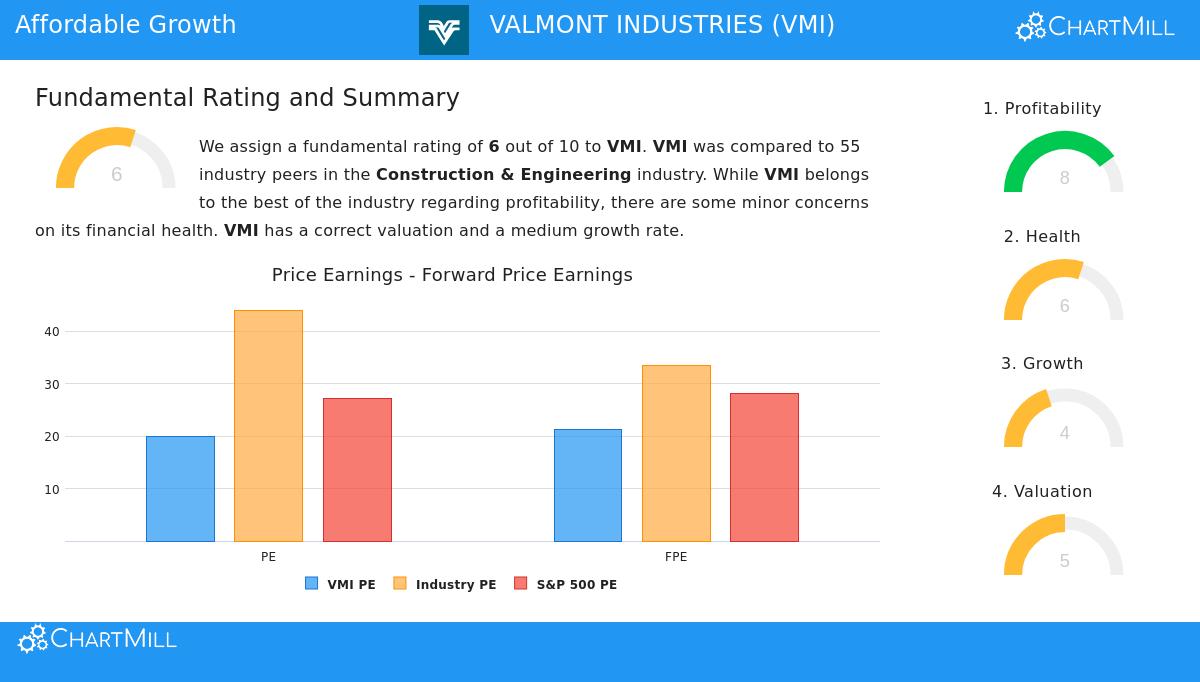

A wider fundamental review of Valmont Industries gives setting beyond the specific filter requirements. The company gets a total fundamental score of 6 out of 10, which puts it in a firm spot next to similar companies in the Construction & Engineering field.

The review points out several positive points:

- Very Good Profitability: Valmont gets an 8 out of 10 for profitability, with high scores for its Return on Assets, Return on Invested Capital (ROIC), and growing profit and operating margins.

- Acceptable Financial Condition: With a score of 6, the company's condition is satisfactory. It has a very good Current Ratio and a workable debt amount, though the report mentions a recent small weakening in its debt-to-assets ratio.

- Sensible Price: The price score of 5 shows a varied situation. While its P/E ratio of 19.94 seems high on its own, it is lower than most of its industry peers and the wider S&P 500, particularly when seen using its forward P/E and enterprise value measures.

Points for investor thought include a small dividend yield and forecasts for a reduction in both sales and earnings growth in the next years compared to its past speed. You can see the complete, thorough fundamental report for Valmont Industries here.

Is Valmont a Lynch-Type Prospect?

For investors following Peter Lynch's thinking, Valmont Industries offers an interesting example. It works in necessary, clear fields, shows a background of good and lasting earnings growth, and keeps a sound balance sheet. Most significantly, its stock price, when judged by the PEG ratio, does not seem to have risen too high compared to that historical growth. This mix of features is exactly what the GARP method tries to find: a reliable company that is expanding, but not at a risky high price.

While past results do not assure future outcomes, and investors must always do their own complete study, Valmont's financial picture matches well with a disciplined, long-term investment plan focused on fundamental soundness and sensible pricing.

Find Other Possible Prospects The Peter Lynch method filter can be a useful beginning step for making a watchlist. Valmont Industries is only one of the companies that presently meets this group of tests. To see other stocks that fit these standards for lasting growth at a sensible price, you can view the live filter here.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any security. Investing holds risk, including the possible loss of principal. You should do your own study and talk with a qualified financial advisor before making any investment choices.