Investors looking for growth chances often meet the task of weighing a company's expansion prospects against its present market price. The "Growth at a Reasonable Price" (GARP) method addresses this by focusing on companies that show solid, lasting growth but are not priced at extreme levels. One way to find these options is through a basic screening process that reviews stocks using five main areas: Growth, Valuation, Health, Profitability, and Dividend. A stock that performs strongly on growth and keeps good marks in health and profitability, while also being seen as fairly priced, can be an interesting option for this method. VICOR CORP (NASDAQ:VICR), a designer and maker of modular power components, recently appeared from this "Affordable Growth" screen, indicating it may deserve further examination by investors focused on GARP.

Growth Path and Momentum

The central idea of any growth investment is a company's capacity to increase its earnings and revenue. Vicor's fundamental report points out notable strength here, which is important for the affordable growth method as it looks for companies with a clear and speeding expansion story.

- Earnings Growth: The company's Earnings Per Share (EPS) increased by a notable 211.54% over the previous year. More indicative of sustainability, the average yearly EPS growth over multiple years is 30.38%.

- Revenue Increase: Revenue rose by 13.55% in the last year, with a steady multi-year average growth rate of 6.57%.

- Future Outlook: Analysts forecast this pace to persist, with EPS predicted to grow about 55.74% each year in the near future, and revenue growth speeding up to a projected 17.10%. The report mentions that both EPS and revenue growth rates are speeding up, a good signal for future possibility.

This mix of solid past results and stronger future forecasts provides Vicor a high Growth score of 8 out of 10, directly fitting the "good growth" requirement needed for this screening method.

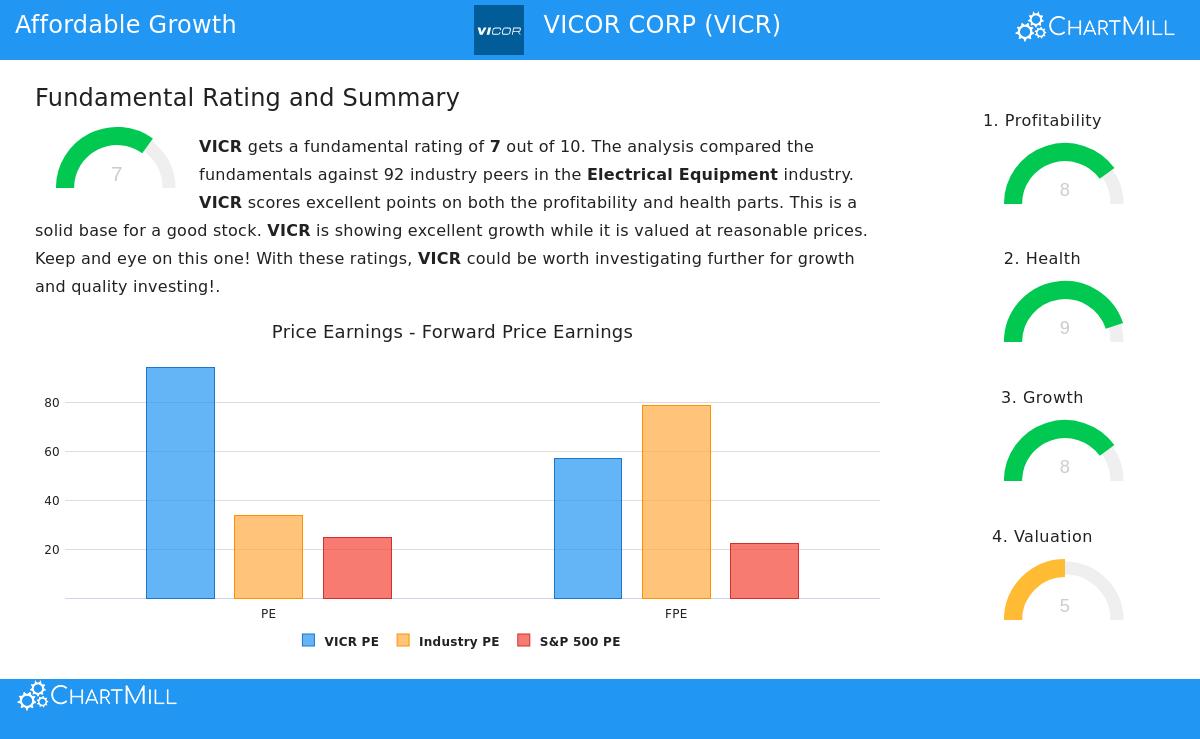

Valuation with Perspective

While growth is key, paying a fair price for that growth is what shapes the GARP method and avoids too much exposure to speculative excess. Valuation is where the study becomes detailed. Vicor's Valuation score is a 5 out of 10, showing a varied situation that needs perspective.

On the surface, standard measures seem elevated. The company's Price/Earnings (P/E) ratio of 94.46 and Forward P/E of 56.90 are high, both on their own and compared to the wider S&P 500. However, the screening logic stresses comparative valuation inside its industry. Here, Vicor offers a more fair case:

- Its P/E ratio is lower than around 66% of similar companies in the Electrical Equipment industry.

- Its Forward P/E is lower than about 64% of industry rivals.

- Other measures like Enterprise Value to EBITDA and Price/Free Cash Flow also show Vicor is priced more affordably than most of its industry.

Most significantly, the valuation review considers the company's outstanding growth and profitability. The report says the PEG ratio, which includes growth, implies a proper valuation, and that the high forecasted earnings growth may support the present multiples. This perspective-based study backs the screen's conclusion that the stock is "not overvalued" within its competitive field.

Supporting Financial Soundness

An affordable growth stock must be more than a quickly expanding company at a fair price; it requires the financial base to maintain its growth. This is where Vicor's profile becomes especially interesting, as it performs well in the areas of Health and Profitability.

Financial Health (Score: 9/10): Vicor’s balance sheet is a major positive. The company has no debt, putting it in a top position within its field for financial options and risk control. This is supported by very good liquidity, with a Current Ratio of 8.99 and a Quick Ratio of 7.59, showing more than enough means to meet short-term needs. These measures lead to an excellent Altman-Z score of 58.30, pointing to very low near-term bankruptcy danger.

Profitability (Score: 8/10): The company turns its sales into earnings effectively. Vicor has a strong Profit Margin of 29.08%, doing better than almost 97% of its industry. Its Gross Margin of 52.59% is also with the best in the field. Also, key return measures like Return on Assets (15.09%) and Return on Equity (16.66%) are in the high ranks of the industry, showing good use of capital.

These high scores in Health and Profitability are not minor to the screening method; they are its protection. They make sure the found growth is supported by a sound and well-run business, lowering the chance that the company will falter from financial pressure or weak operational performance.

Summary

VICOR CORP shows an example of the kind of company an "Affordable Growth" or GARP screen aims to find. It shows strong, speeding growth in earnings and revenue, supported by analyst confidence for what is ahead. While its absolute valuation multiples are high, they are viewed as fair compared to its industry peers and when weighed against its growth path and better profitability. Importantly, this growth story is built on a very firm financial base of no debt and high liquidity, giving stability and endurance.

For investors curious about finding other companies that match this profile of good growth, fair valuation, and stable basics, more outcomes can be seen by checking the Affordable Growth screen on ChartMill. A full look at Vicor's separate fundamental measures is in its complete Fundamental Analysis Report.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.