Visteon Corp (NASDAQ:VC) has appeared as a possible choice for investors using a careful value method. This method, based on the ideas of Benjamin Graham and made common by Warren Buffett, aims to find companies selling for less than their true value. The central concept is to buy shares of a business with sound foundations when the market sets a low price, offering a "margin of safety." A main difficulty is finding such chances in an organized way while avoiding "value traps," stocks that are low-priced for a cause, frequently because of worsening foundations. To manage this, filters can be set to select for companies that are not only low-cost on common value measures but also show good financial condition and earnings, confirming the low price is a chance and not a problem.

A Closer Look at the Foundations

A check of Visteon's detailed fundamental analysis report shows a profile that fits well with the needs of a "good value" filter. The company, a worldwide automotive electronics supplier, is rated well in a number of important areas while showing a very low price.

Notable Value Measures

The most noticeable part of Visteon's report is its Valuation Rating of 8 out of 10. The company seems priced very low compared to both its industry and the wider market, a main sign for value investors.

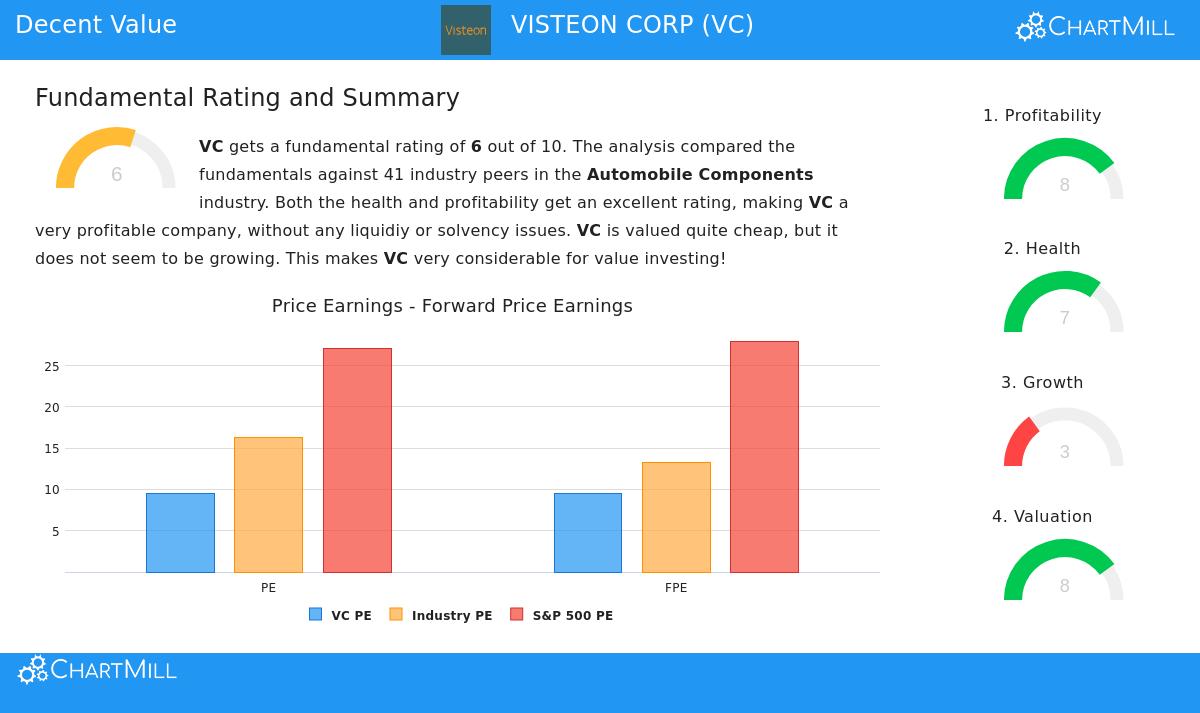

- Price-to-Earnings (P/E): At 9.49, VC's P/E ratio is lower than 95% of similar companies in the Automobile Components industry and sits far below the present S&P 500 average of 27.09.

- Forward P/E: The price stays good looking forward, with a Forward P/E of 9.52. This is lower than 83% of industry rivals and under a third of the S&P 500's forward average.

- Cash Flow & EBITDA Multiples: The low price continues with cash-based measures. VC is valued lower than 93% of the industry on its Price/Free Cash Flow ratio and lower than 90% on its Enterprise Value to EBITDA ratio.

For a value investor, these measures indicate the market may not fully recognize Visteon's basic earnings ability, creating the possible difference between price and true value that the method looks to use.

Good Earnings and Financial Condition

A low price by itself is insufficient; it must be combined with a sound business. This is where Visteon's foundations give important support, reducing the danger of a value trap. The company receives a high Profitability Rating of 8 and a good Health Rating of 7.

-

Earnings Strength:

- High Returns: The company produces a good Return on Equity of 20.84%, doing better than 95% of its industry, and a sound Return on Invested Capital of 11.95%.

- Getting Better Margins: Both its Profit Margin (8.22%) and Operating Margin (9.31%) are in the top group of the industry and have shown positive changes in recent years.

-

Financial Strength:

- Careful Balance Sheet: Visteon keeps a very workable Debt/Equity ratio of 0.19 and has a Debt to Free Cash Flow ratio of only 0.84, showing it could clear all its debt in under a year with its present cash flow. This degree of financial soundness is better than most of its peers.

- Low Failure Risk: An Altman-Z score of 3.86 shows financial steadiness and a low short-term risk of financial trouble.

These points are necessary for the value method. Good earnings show the company can increase its true value over time, while a solid balance sheet provides strength in economic declines, guarding the investor's margin of safety.

Points for Review: Growth and Dividend

The analysis does note areas where Visteon's profile is less clear, which is common for many value stocks.

- Growth Path: The company's Growth Rating is a moderate 3. While past Earnings Per Share (EPS) growth has been very good over several years, it fell a little over the last year. Looking forward, experts anticipate a reasonable EPS growth of about 12% each year, though this is a slowdown from the past fast rate. For a value investor, this adequate but not outstanding growth view is often included, as very high-growth companies seldom trade at large discounts.

- Dividend Profile: With a Dividend Rating of 2, income is not a main attraction. The yield is near 1.06%, which is more than the industry average but less than the S&P 500. Also, the company has a brief dividend history. Value investors often like dividend payers, but a focus on price gains from a closing value difference can be the main source of return.

Conclusion

Visteon Corp presents a situation where traditional value investing measures meet good basic business foundations. Its very low price measures, when compared with its high earnings and good financial condition, suggest the stock may be priced too low by the market. The company’s role as an important electronics supplier in the changing automotive field gives a business reason for its earnings ability. While its growth is anticipated to become more standard and it is not a high-payout income stock, these are usual exchanges when looking for low-priced chances.

For investors wanting to use this organized search for value, the filter that found Visteon can be a helpful beginning. You can find more stocks that fit similar needs of good price, earnings, health, and growth by reviewing this Good Value Stocks filter.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and sources believed to be reliable, but its accuracy cannot be guaranteed. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.