For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish truly lasting dividend payers from risky high-yield situations. One useful technique involves selecting for companies that provide a good dividend and also have the basic financial capacity to keep and possibly increase those payments. This method focuses on a high ChartMill Dividend Rating, which combines important measures like yield, growth, and payout safety, while also setting basic requirements for earnings and financial soundness. This multi-step process aids in finding companies where the dividend is backed by a strong business, instead of being a temporary feature of a company in trouble.

THOMSON REUTERS CORP (NASDAQ:TRI) appears as a notable candidate from such a filter, making an argument for dividend investors to review.

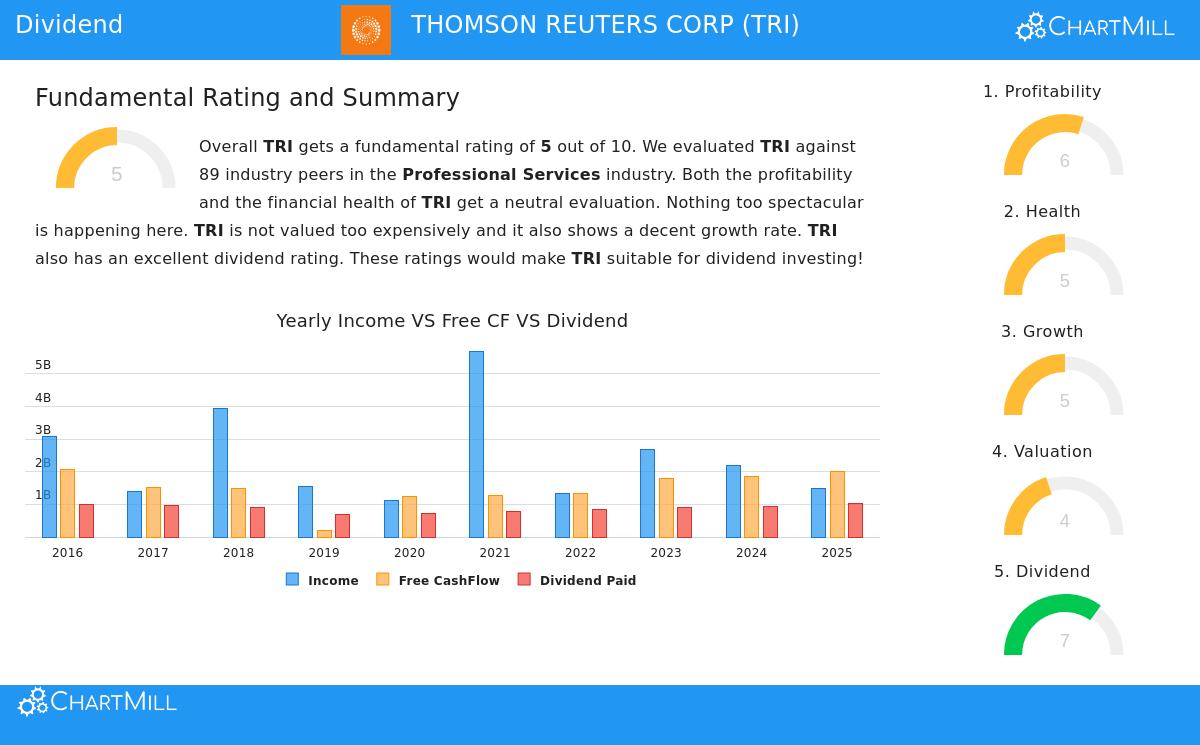

Dividend Attraction: A High Yield with History

The foundation of TRI's attraction for income-focused investors is its dividend profile, which earns a solid 7 out of 10 on the ChartMill Dividend Rating. This score rests on several good points:

- Good Yield: The company now provides a yearly dividend yield of 6.29%, which is much higher than both the industry average (1.53%) and the wider S&P 500 average. For investors looking for current income, this is a direct point of appeal.

- Dependable and Increasing Payouts: TRI has built a dependable history, having paid dividends for at least ten straight years. Also, it has shown a dedication to giving more to shareholders over time, with an average yearly dividend increase rate of 8.41% over the last five years.

- Growth Safety: A vital test for any high-yielding stock is if the dividend increase is backed by business expansion. For TRI, the basic report notes that while earnings are rising at a good rate, the dividend is rising a bit more slowly. This situation implies the present dividend increase path is safe, as it is not exceeding the company's capacity to produce earnings.

Supporting Basics: Earnings and Soundness

A high dividend yield is less appealing if the company's base is weak. The filter requirements of acceptable earnings and soundness are important because they evaluate the company's capacity to pay its dividend from normal business and handle economic stress. TRI's scores in these areas give background for its dividend quality.

Earnings (Score: 6/10): TRI works with notable efficiency, a main sign of a business that can regularly produce cash for shareholders. Its profit margin of 20.04% and operating margin of 26.62% place it with the better performers in its field. Good returns on assets and invested capital further show the company is skilled at turning its resources into profits. This high level of earnings is the source that pays the dividend and makes the payout ratio of 69.36%, while elevated, more acceptable than it would be for a less profitable company.

Financial Soundness (Score: 5/10): The soundness score shows a varied but finally steady picture. On the good side, TRI displays very good solvency. It has little debt, with a very low Debt/Equity ratio, and its Altman-Z score shows no short-term bankruptcy concern. The company could settle its current debt with just over a year's worth of free cash flow, showing good balance sheet quality.

However, investors should note a point of care in the liquidity review. The company's current and quick ratios are below 1.0, which is viewed as low and implies it may have less buffer to meet immediate needs without using operational cash flow. This is a typical trait in some business models but is a factor to watch, particularly when interest rates are rising.

Price and Growth Background

With a basic rating of 5/10, TRI sits in the middle overall. Its price is not a clear discount but seems fair compared to the market. Its P/E ratio is a bit under the S&P 500 average, and its price-to-free-cash-flow ratio is more appealing than many industry counterparts. Looking forward, analysts forecast good growth, with expected yearly rises of 11.90% in earnings per share and 8.35% in revenue. This expected growth backs the idea that the company can continue its path of dividend raises.

A Candidate for More Review

For dividend investors using a quality-and-yield method, THOMSON REUTERS CORP shows a significant profile. It joins a high, well-backed yield with a history of growth, supported by good earnings and a firm, long-term debt position. The lower liquidity measures deserve notice but are offset by the company's strong cash production. As with any investment, this filter-based finding is a beginning for more detailed investigation.

Interested in seeing other stocks that meet similar dividend quality filters? You can see the complete list of candidates by going to the pre-set "Best Dividend Stocks" screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any securities. The review is based on data and scores from ChartMill, which looks at past and present basics. Investors should do their own complete research, thinking about their personal financial position and risk comfort, before making any investment choices. Past results do not guarantee future outcomes.