For investors looking to balance the search for high-growth companies with fundamental caution, the "Affordable Growth" or "Growth at a Reasonable Price" (GARP) method offers a practical middle path. This method seeks to find companies with strong growth paths, but whose stock prices do not yet fully reflect that future promise, providing a more sensible entry point than highly valued counterparts. The method usually screens for stocks with good growth measures, firm underlying profitability, a sound financial position, and, importantly, a valuation that does not seem excessive. By concentrating on these combined elements, investors can search for chances where the market may not completely recognize a company's future earnings capacity, possibly providing a good balance of risk and reward.

TransMedics Group Inc (NASDAQ:TMDX) serves as an example for this investment method. The medical technology company, which focuses on portable organ perfusion systems for transplantation, has recently been identified by an Affordable Growth screen. According to a detailed fundamental analysis report, TMDX receives an overall fundamental rating of 6 out of 10, with its profile indicating clear positives in growth and financial condition, together with a valuation that seems acceptable given its high-growth setting.

Growth: The Main Factor

The most notable part of TransMedics is its outstanding growth profile, which receives a high rating of 8. This score represents very strong recent results and good future estimates, which are the main drivers for any GARP investment.

- Very Strong Recent Results: Over the last year, the company's Earnings Per Share (EPS) increased by 162.77%, while Revenue expanded by 41.20%. Looking further back, the average yearly Revenue expansion in recent years is 79.64%.

- Good Forward Estimates: The growth narrative is projected to persist. Analysts estimate EPS will expand by 33.25% each year in the near future, with Revenue expected to rise at an average rate of 21.23% per year.

This mix of confirmed high growth and a good forecast is necessary for the Affordable Growth method, as it supplies the fundamental "growth" premise for which investors are paying.

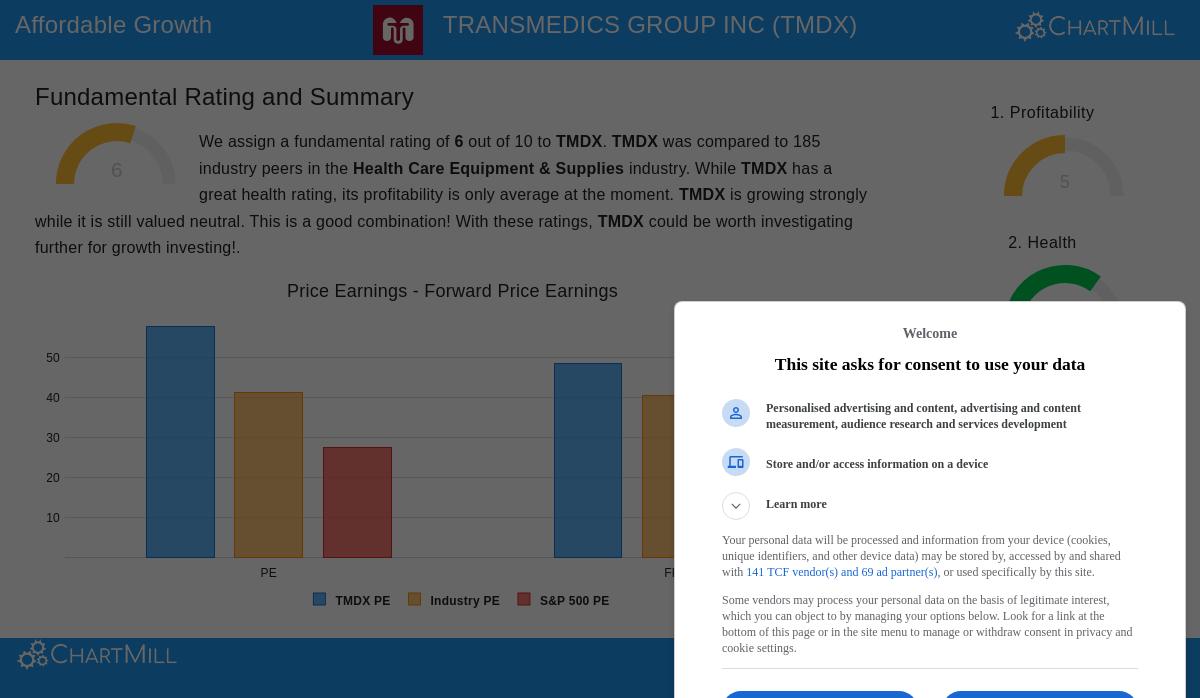

Valuation: Evaluating the Cost of Growth

A stock with good growth can still be a bad investment if bought at too high a price. This is where the valuation review becomes vital. TMDX gets a valuation rating of 5, showing a varied but ultimately acceptable situation when balanced against its growth.

- Absolute Multiples: On an absolute basis, TMDX trades at a Price/Earnings (P/E) ratio of 57.78 and a Forward P/E of 48.30, which are elevated compared to the wider S&P 500 average.

- Relative and Growth-Considered View: The setting is important. Within its industry (Health Care Equipment & Supplies), TMDX is less expensive than about 68-69% of similar companies based on these P/E ratios. More importantly, its low PEG ratio—which modifies the P/E for estimated earnings expansion—implies the current valuation could be warranted, or even interesting, considering the company's projected expansion rate of over 53% for the next year.

For the Affordable Growth screen, a valuation score above 5 indicates the stock is not in the costliest group, particularly when its industry counterparts and growth outlook are accounted for, rendering it "not overvalued" within the method's limits.

Financial Condition and Profitability: The Supporting Base

While growth and valuation are the primary criteria, the method also asks for acceptable scores in financial condition and profitability. These elements help confirm the company has the steadiness to deliver its growth plans and is producing quality earnings.

- Financial Condition (Rating: 7): TMDX shows a very strong liquidity situation, with a Current Ratio of 7.69 and a Quick Ratio of 7.13, doing better than most industry counterparts. This signals strong ability to meet near-term requirements. Its solvency measures are mixed, with a good Altman-Z score indicating low bankruptcy risk, but a somewhat high Debt/Equity ratio showing a notable use of debt financing.

- Profitability (Rating: 5): The company's profitability is changing. After periods of losses as it brought its technology to market, TMDX has recently become profitable. Its present margins are very good, with Profit Margin (16.20%) and Operating Margin (16.94%) placed in the top part of its industry. The average rating mirrors this positive recent shift against a background of past negative earnings.

These acceptable scores in condition and profitability give assurance that the company's growth is supported by a more solid operational and financial base, lowering the chance that it is expanding in an unstable way.

Conclusion

TransMedics Group Inc demonstrates the kind of chance sought by an Affordable Growth method: a company with confirmed, high-speed growth in both its past performance and future estimates, matched with a valuation that is acceptable relative to that growth possibility and its industry setting. Its sound financial condition offers a cushion, and its recent shift to good profitability is a positive indicator of business model development. While the debt level and past losses merit notice, the complete fundamental view suggests a business delivering on a major growth plan without being valued for flawless execution.

For investors wanting to examine other companies that match this profile of solid growth, acceptable valuation, and acceptable fundamentals, more outcomes are available by checking the Affordable Growth screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.