The investment philosophy of Peter Lynch, the legendary manager of Fidelity's Magellan Fund, focuses on finding companies with durable growth that are trading at sensible prices. This "growth at a reasonable price" (GARP) method steers clear of speculative high-priced stocks and stagnant low-growth companies. Lynch’s method, described in his book One Up on Wall Street, employs a group of fundamental filters to find these companies, concentrating on earnings growth, valuation, profitability, and financial soundness. A recent filter using these Lynch principles has identified one name for further review: TaskUs Inc-A (NASDAQ:TASK).

A Lynch Profile: Reviewing the Main Criteria

The center of Lynch's filter searches for a particular financial picture. TaskUs, a company offering digital outsourcing services for customer experience, content moderation, and AI operations, seems to match these numerical standards closely. The company's stated numbers speak directly to the important rules of the method.

- Durable Earnings Growth: Lynch wanted companies increasing earnings per share (EPS) between 15% and 30% each year over five years, thinking growth outside this band was either too low or not durable. TaskUs states a five-year EPS growth rate of 25.7%, putting it solidly inside this preferred zone of sound and possibly continued increase.

- Appealing Valuation via PEG: Maybe the most important Lynch number is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price matches the growth rate. A PEG of 1 or below is seen as appealing. TaskUs stands out here, with a PEG ratio calculated from its five-year growth near 0.27. This shows the market is pricing its shares at a notable markdown compared to its past earnings growth path.

- Sound Profitability (ROE): Lynch demanded a high return on equity (ROE) to make sure management was using investor money effectively. His lowest limit was 15%. TaskUs is above this with an ROE of 17.05%, indicating the company is producing good profits from its equity.

- Cautious Financial Soundness: To limit high risk, Lynch preferred companies with firm balance sheets. His filter uses a Debt/Equity ratio below 0.6 (with a personal liking for under 0.25) and a Current Ratio above 1. TaskUs satisfies both conditions easily, with a Debt/Equity ratio of 0.37 and a very sound Current Ratio of 3.12. This shows little dependence on debt and sufficient cash to meet near-term needs.

Fundamental Soundness Review: Looking Past the Filter

While the filter gives a good beginning point, Lynch supported more detailed investigation. A look at TaskUs's detailed fundamental analysis report gives a wider picture that mainly supports the initial filter findings.

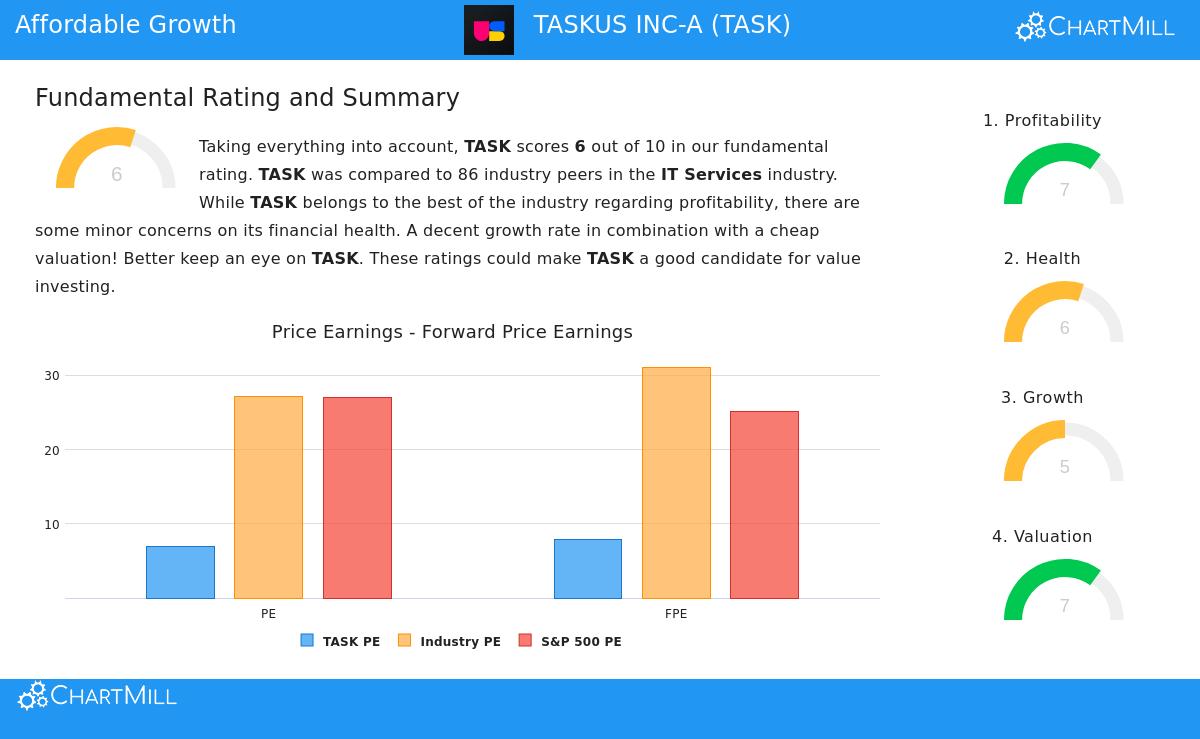

The report gives TaskUs a total fundamental score of 6 out of 10, calling it a possibly "interesting mix" for investors focused on price. The details show main positives and points to watch:

- Profitability is a Definite Positive: The company scores well here (7/10), with excellent numbers. Its Return on Equity, Return on Invested Capital (10.87%), and operating margins all sit in the top group of its IT Services industry. Profit and operating margins have gotten better in recent years.

- Valuation Stays Appealing: Scoring 7/10, the valuation review supports the filter's discovery. TaskUs trades at a P/E ratio of 6.9 and a forward P/E of 7.84, making it less expensive than more than 90% of its industry rivals and the wider S&P 500.

- Financial Soundness is Firm: With a score of 6/10, the balance sheet is seen as sound. The low Debt/Equity and high Current and Quick Ratios confirm good solvency and liquidity, as found in the filter.

- Growth Shows a Varied View: This is the area for investor attention, scoring 5/10. The past is strong, with notable historical growth in both EPS and Revenue. However, analyst forecasts point to a marked slowing in the next few years, with expected EPS and revenue growth in the low-to-mid single digits. This forward-looking reduction is the main element lowering the total growth score and is a key point for any long-term view.

Is TaskUs a Lynch-Method Chance?

For an investor using a GARP method drawn from Peter Lynch, TaskUs offers an interesting example. It succeeds in the initial numerical filter very well, showing the precise picture of a profitable, financially firm company increasing at a durable historical rate and trading at a very sensible price. The very low PEG ratio is especially noteworthy.

The more detailed fundamental analysis confirms the company's operational positives and cautious financing. The main question for a long-term owner, however, will concern the future growth path. Lynch stressed knowing how and why past growth happened and judging if it can persist. Investors need to study whether the forecasted slowing is a short-term industry challenge or a more lasting change, and whether TaskUs's services in digital CX, trust & safety, and AI operations place it to grow faster again over a multi-year period.

If you want to look at other companies that match this careful growth-at-a-sensible-price method, you can see the complete list of results from the Peter Lynch strategy filter here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. Investing involves risk, including the potential loss of principal. You should conduct your own thorough research and consider consulting with a qualified financial advisor before making any investment decisions.