For investors looking to create passive income from the stock market, a systematic selection process is important. One useful tactic is to search for companies that provide a good dividend now and also have the basic financial soundness to maintain and possibly raise those payments in the future. This method focuses on quality and longevity instead of pursuing the highest available yield, which can sometimes indicate problems in a business. A real-world use of this tactic is a multi-factor filter that finds stocks with good dividend ratings while also needing acceptable marks in earnings and balance sheet strength. This mixes income creation with basic soundness.

One company that comes from such a systematic filter is Shell PLC (NYSE:SHEL), the large worldwide energy company. The company's presence on a "Best Dividend" filter suggests it deserves more examination by income-seeking investors, as it seems to fit the main requirements of a steady payer with a good base.

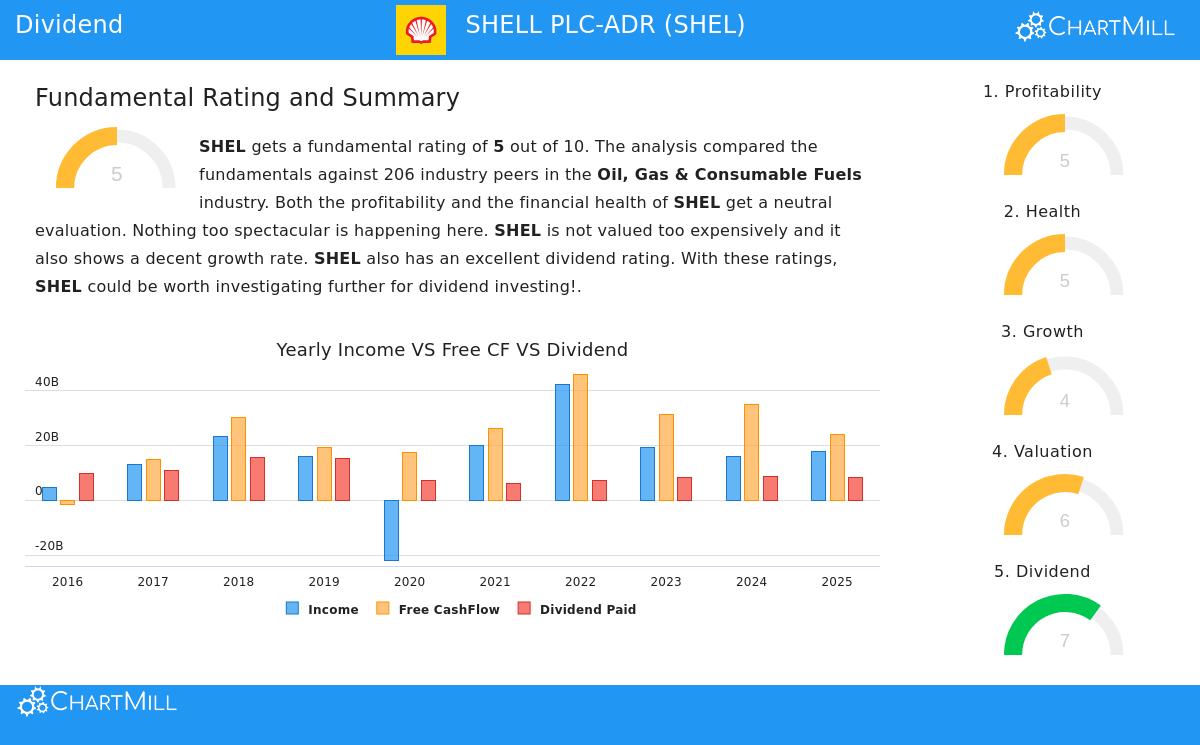

Dividend Profile: A Steady Payer with Potential for Increase

The main attraction for dividend investors is Shell's long-standing payment. The company's dividend traits, which lead to its solid ChartMill Dividend Rating of 7, show a dedication to giving cash to shareholders.

- Good and Higher-Than-Average Yield: Shell now has a dividend yield of 3.74%. This is greater than the typical yield of the S&P 500 (about 1.80%) and is also a bit higher than the average for similar companies in Oil, Gas & Consumable Fuels.

- Long History of Increase: Steadiness is supported by past performance. Shell has given a dividend for at least ten years, offering a long history. Also, it has shown an ability to raise the payment, with an average yearly dividend increase rate of 8.63% in recent years.

- Manageable Payout Ratio: A key test for longevity is the payout ratio, which shows the part of earnings given as dividends. Shell's ratio is about 47.5%. While this is toward the higher end of acceptable, it is usually seen as workable, particularly since the company's earnings are now rising quicker than its dividend. This situation indicates the present payment level is lasting and allows for possible future raises.

Supporting Basics: Earnings and Balance Sheet Strength

A high dividend is only as reliable as the company's skill to pay for it. This is where the filter's extra requirements for acceptable earnings and strength matter, and Shell's marks of 5 in both areas give important background. These ratings show the company has the operational and balance sheet support to maintain its shareholder payments.

Earnings (Rating: 5) Shell's earnings measures present a varied but overall sufficient view. The company is regularly profitable and creates positive cash flow, a basic need for any steady dividend payer. Its Return on Equity (ROE) of 10.23% and Return on Assets (ROA) of 4.82% are good, doing better than most of its industry peers. While its profit margins have been challenged lately, its operating margin has gotten better. For a dividend investor, the important points are continued profits and good returns on capital, which supply the earnings foundation from which dividends are paid.

Balance Sheet Strength (Rating: 5) Balance sheet strength is critical to make sure a company can handle economic lows without risking its dividend. Shell's balance sheet displays both positive points and areas to note. On the good side, it keeps a careful Debt-to-Equity ratio of 0.38, showing it is not too dependent on debt. Its liquidity ratios (Current and Quick ratios) are within standard limits, suggesting it can cover near-term debts. A clear positive is its good Debt-to-Free-Cash-Flow ratio of 3.16, meaning it could pay off all its debt with just over three years of its present cash flow creation, a signal of sound cash-based strength. Investors should be aware, however, that the report notes the company's return on invested capital is now below its cost of capital, showing space for better efficiency in creating value.

Price: A Reasonable Starting Point

For investors thinking about buying, price is a key factor. Shell seems fairly valued, trading at a P/E ratio of 10.25 and a forward P/E of 11.85. These numbers are much lower than the wider S&P 500 and are also on the more appealing side of its own industry range. This fair price, combined with the dividend yield, can give investors a good mix of income and possible price gain without paying a high price for the stock.

Conclusion

Shell PLC makes a strong argument for dividend investors using a quality-centered filter strategy. It provides a higher-than-average yield supported by a ten-year payment history and a sound increase rate in the dividend itself. Importantly, this income is backed by sufficient earnings and a balance sheet strength profile that, while not perfect, displays good liquidity and workable debt, exactly the sort of basic support the filter method aims to find. The stock's fair price further increases its attraction for those aiming to create or increase an income-producing portfolio.

Want to look at other stocks that pass similar quality dividend filters? You can see the complete list of results and adjust the filters yourself by going to the Best Dividend Stocks screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any securities. Investors should do their own study and think about their personal money situation before making any investment choices. Past results do not guarantee future outcomes.