For investors aiming to assemble a portfolio of lasting, high-achieving businesses, the quality investing method provides a structured system. This system targets finding companies with durable competitive strengths, sound financial condition, and a consistent record of creating high returns on capital over many years. The "Caviar Cruise" stock screen puts this thinking into practice by selecting for firms with a record of solid revenue and profit increase, high profitability measures, good cash flow generation, and reasonable debt. The aim is not to locate temporary discounts, but to discover businesses deserving of lasting commitment.

One firm that now meets this strict screen is SOUTHERN COPPER CORP (NYSE:SCCO), a leading worldwide entity in extracting copper, molybdenum, zinc, and silver. For quality investors, a mining firm may appear an unusual choice because of the recurring pattern of commodity prices. Yet, an examination of SCCO's financial measures shows a business that displays many traits of a quality firm, especially in its outstanding profitability and financial control.

Matching the Main Quality Standards

The Caviar Cruise screen is constructed on multiple key filters intended to distinguish outstanding businesses from others. Southern Copper's financial picture matches these main needs well:

-

High Return on Capital: A central part of quality investing is a high Return on Invested Capital (ROIC), which calculates how well a company creates profits from its capital foundation. SCCO states an ROIC (leaving out cash, goodwill, and intangibles) of 31.2%, much higher than the screen's 15% limit. This shows that the company's mines and activities are highly productive and that leadership has a confirmed history of using capital well.

-

Solid and Rising Profitability Increase: The screen requires that a company's Earnings Before Interest and Taxes (EBIT) rise quicker than its revenue over a five-year span, indicating gaining operational effectiveness and pricing ability. SCCO's measures are strong here:

- Revenue Increase (5Y CAGR): 12.3%

- EBIT Increase (5Y CAGR): 17.3% This difference verifies that the company's profit increase is not only from selling more metal, but also from handling its expenses and operations with greater skill.

-

Sound Financial Condition and Cash Flow: Quality companies are not weighed down by debt and produce sufficient cash. The screen employs a Debt-to-Free Cash Flow (FCF) ratio under 5 years to evaluate how fast a company could ideally settle its debts. SCCO's ratio of 2.0 is very sound, indicating high solvency and financial room. Also, its average Profit Quality—the change of net income into free cash flow—over the last five years is 91.1%, above the 75% standard. This means the profits stated on its income statement are regularly received as actual cash, a main sign of earnings integrity and financial toughness.

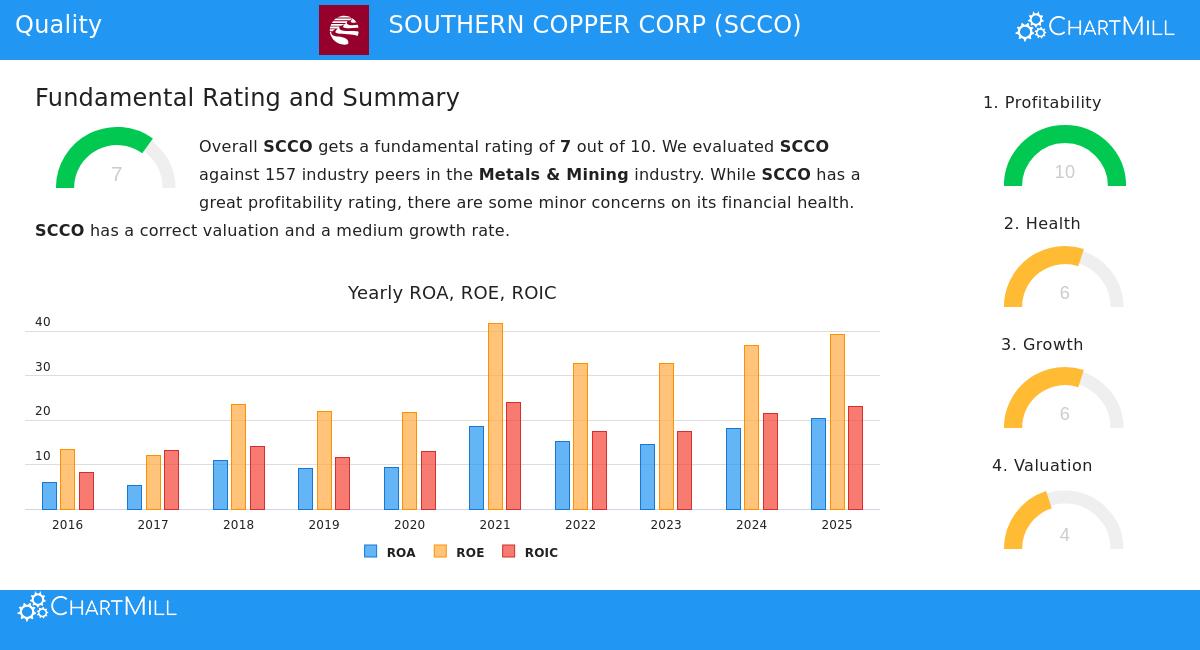

Fundamental Rating Summary

A look at SCCO's full fundamental analysis report gives a wider view for these screen outcomes. The report gives SCCO a total rating of 7 out of 10, noting a firm with definite positives and some points to note.

The prominent trait is SCCO's high profitability, which receives a top score of 10. The company is best in its field in key margins (Gross, Operating, and Profit Margin) and provides leading returns on assets, equity, and invested capital. These measures are the foundation of the quality investment argument.

Its financial condition scores a good 6, helped by very good liquidity ratios and the positive Debt/FCF ratio mentioned before. A middling debt-to-equity ratio is a small note but is balanced by the company's large cash-producing capacity. The increase rating is also a 6, showing a solid historical performance in both revenue and earnings, though analyst forecasts for future earnings increase are more measured.

The main area of attention is in valuation. With a Price-to-Earnings (P/E) ratio over 36, the stock seems costly on a plain basis, though it is priced better relative to its industry group. This highlights a main idea of quality investing: while investors often accept a higher price for better businesses, valuation remains important and needs thoughtful assessment.

Investment Argument and Points

For a quality investor, Southern Copper offers an argument based on holding a top-tier operator in a necessary industry. The company's huge size, low-cost activities, and long-term mineral resources supply a lasting competitive edge. Its excellent ROIC and profit margins show this edge in financial figures. The good cash flow production backs a steady and rising dividend, with a history of raises over the last ten years.

Still, this investment argument is tied to the long-term need for copper, which is greatly affected by worldwide economic patterns and the shift in energy sources. While quality measures center on the company's performance, investors must still develop a perspective on the basic commodity's foundations. The present high valuation also implies that much of the company's strength is already priced by the market, possibly reducing short-term room for error.

Finding Other Quality Prospects

Southern Copper Corp shows the kind of firm the Caviar Cruise screen is made to find: one with high operational skill and financial soundness. Investors wanting to use this system to locate other possible prospects can view the complete screen settings and outcomes through this link: Caviar Cruise Quality Stock Screen.

Disclaimer: This article is for informational and educational reasons only and does not form investment guidance, a suggestion, or an offer or request to purchase or sell any securities. The information shown should not be used as the only basis for any investment choice. Investors should perform their own separate research and review and speak with a skilled financial expert before making any investment. Previous results do not guarantee future outcomes.