The search for undervalued stocks is a foundation of value investing, a strategy that aims to find companies trading below their intrinsic worth. This method, supported by figures like Benjamin Graham and Warren Buffett, requires detailed fundamental analysis to find opportunities where the market price does not match the underlying business quality. One way to simplify this search is by using systematic screens that sort for particular financial criteria. A "Decent Value" screen, for example, seeks stocks with good valuation metrics, indicating they are priced low, while also holding acceptable scores in profitability, financial condition, and growth. This balanced filter tries to point out companies that are not only low-priced but also operationally stable, possibly sidestepping the problems of "value traps."

RANGE RESOURCES CORP (NYSE:RRC), an independent natural gas and oil company focused on the Appalachian region, recently appeared from such a screening process. Its fundamental profile suggests it may deserve additional examination from investors using a value-focused approach.

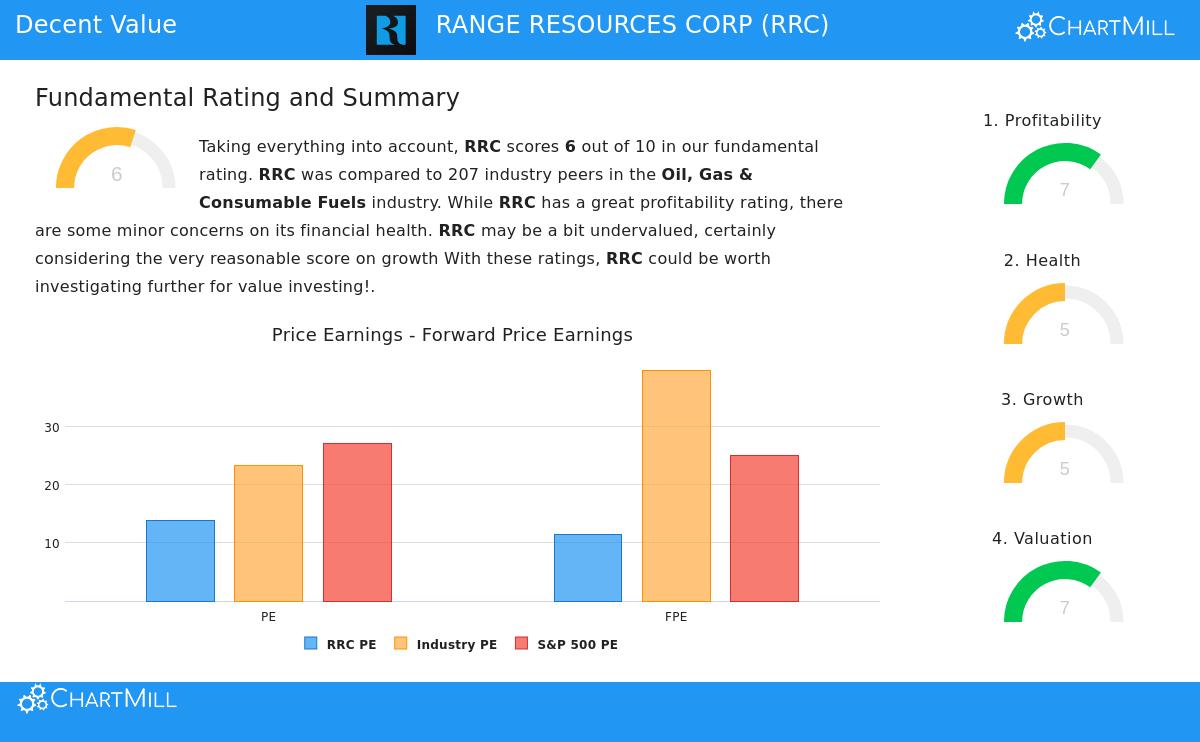

Valuation Metrics: The Center of the Value Case

The main draw for a value investor is a stock's price compared to its financial performance. RRC's valuation metrics create a strong argument for being undervalued. The company's ChartMill Valuation Rating is a good 7 out of 10, showing it is priced more favorably than many similar companies.

- Price-to-Earnings (P/E): At 13.80, RRC's P/E ratio is much lower than the S&P 500 average of 27.03. It is also less expensive than about 69% of companies in the competitive Oil, Gas & Consumable Fuels industry.

- Forward P/E: An even more informative metric is the forward P/E ratio of 11.46, which uses future earnings estimates. This is well below the industry average and indicates the market is pricing RRC's near-term profit potential at a large discount.

- Price-to-Free-Cash-Flow: The ratio shows a fairly low valuation, with RRC being less costly than more than 60% of its industry peers. Good free cash flow production is important as it gives a company options for dividends, debt payment, and reinvestment.

For a value strategy, these ratios are key. They give a numerical beginning, implying the market may be mispricing the company's earnings capability. A low P/E alongside acceptable fundamentals can indicate a chance for the price to adjust to a higher intrinsic value later.

Financial Health & Profitability: Evaluating the Base

A low valuation by itself is insufficient; a company must be in good financial condition to be a genuine value candidate instead of a troubled asset. RRC's ChartMill Health Rating of 5 and Profitability Rating of 7 describe a steady, profitable business with some points to watch.

Financial Health Positives and Points to Watch: The company shows good solvency, an important element for lasting stability.

- Its Debt-to-Equity ratio of 0.28 shows a careful balance sheet with a suitable mix of debt and equity financing.

- The Debt-to-Free-Cash-Flow ratio of 2.26 is very good, meaning it would take slightly over two years of current cash flow to repay all debt, doing better than 83% of the industry.

Still, investors should be aware of a worry in liquidity:

- The Current and Quick Ratios are both 0.67, which is modest and implies the company could have difficulties covering immediate liabilities without using extra credit or cash flow. This is an area for continued attention.

Profitability Positive: RRC's profitability profile is a definite positive, supporting a higher valuation than its current one.

- The company shows notable returns, with a Return on Invested Capital (ROIC) of 10.18%, doing better than 85% of its industry. This shows effective use of capital to create profits.

- Margins are strong, with a Profit Margin of 21.93% and a Gross Margin above 90%, both placed in the higher ranks of the industry.

For the value investor, good profitability confirms the business model. High returns on capital and solid margins suggest the company has a competitive position and pricing ability, which are lasting traits that help intrinsic value estimates.

Growth Path: The Driver for Future Worth

While strict value investing often concentrates on current assets and earnings, lasting growth is what can drive a reassessment of the stock price. RRC's ChartMill Growth Rating of 5 shows a varied but encouraging situation.

- Revenue Growth: The company has shown a good historical revenue growth rate of almost 11% per year over recent years. Looking forward, analysts expect revenue to keep growing at an average rate of more than 9% each year.

- Earnings Growth Background: The past year saw a notable 30% growth in Earnings Per Share (EPS). However, this comes after a time of decrease, leading to a negative 5-year CAGR. Future EPS estimates are currently unchanged to slightly negative, which probably adds to the stock's low valuation.

This growth profile is important for the value argument. The acceptable and expected revenue growth supplies a base for future earnings increase. If the company can turn its high margins and effective capital use into a new period of EPS growth, the current low valuation multiples could improve.

Conclusion and Next Steps

RANGE RESOURCES CORP offers an example in balanced value screening. It trades at a noticeable discount to the wider market and its industry based on common earnings multiples, fitting the main requirement for a value investment. This discount is set next to a base of good profitability and a fairly sound balance sheet, especially concerning long-term solvency. The growth story, supported by acceptable revenue increase, provides a possible reason for the market to reconsider its price.

The screen that found RRC was made to locate precisely this kind of profile: undervalued yet operationally stable. For investors wanting to examine similar opportunities, you can see the full fundamental analysis report for RRC here.

Find Other Possible Value Stocks This review of RRC came from a systematic "Decent Value" screen. If you want to find other companies that fit similar standards of appealing valuation combined with acceptable fundamentals, you can view and adjust this screen for yourself here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy, sell, or hold any security, or an endorsement of any investment strategy. The analysis is based on data and ratings provided by ChartMill, and investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.