For investors aiming to assemble a portfolio of durable, high-grade businesses, the quality investing approach provides a structured system. This method centers on finding companies with lasting competitive strengths, sound financial condition, and a history of earnings growth, with the plan of owning them for many years. The "Caviar Cruise" stock screen puts this thinking into practice by selecting for firms that show consistent past results in sales and earnings growth, high returns on capital, strong cash generation, and reasonable debt. The aim is not to locate temporary discounts, but to identify enterprises constructed to last and increase wealth over years.

One firm that now meets this strict group of filters is Rollins Inc. (NYSE:ROL), a worldwide top provider in pest and termite control services. By reviewing how Rollins fits the main principles of the Caviar Cruise screen, we can see why it may deserve more attention from investors focused on quality.

Matching the Main Standards for Quality

The Caviar Cruise screen sets multiple numerical barriers meant to distinguish outstanding businesses from the average. Rollins satisfies or passes these important measures, as shown by the given data.

-

Continued and Earnings Growth: The screen asks for at least a 5% compound annual growth rate (CAGR) for both sales and EBIT (earnings before interest and taxes) over five years. Rollins performs well here, with a sales CAGR of 8.08% and a higher EBIT CAGR of 14.97%. Importantly, EBIT growth exceeding sales growth—a main filter in the screen—points to better operational efficiency and pricing ability, indicating the firm is growing profitably.

-

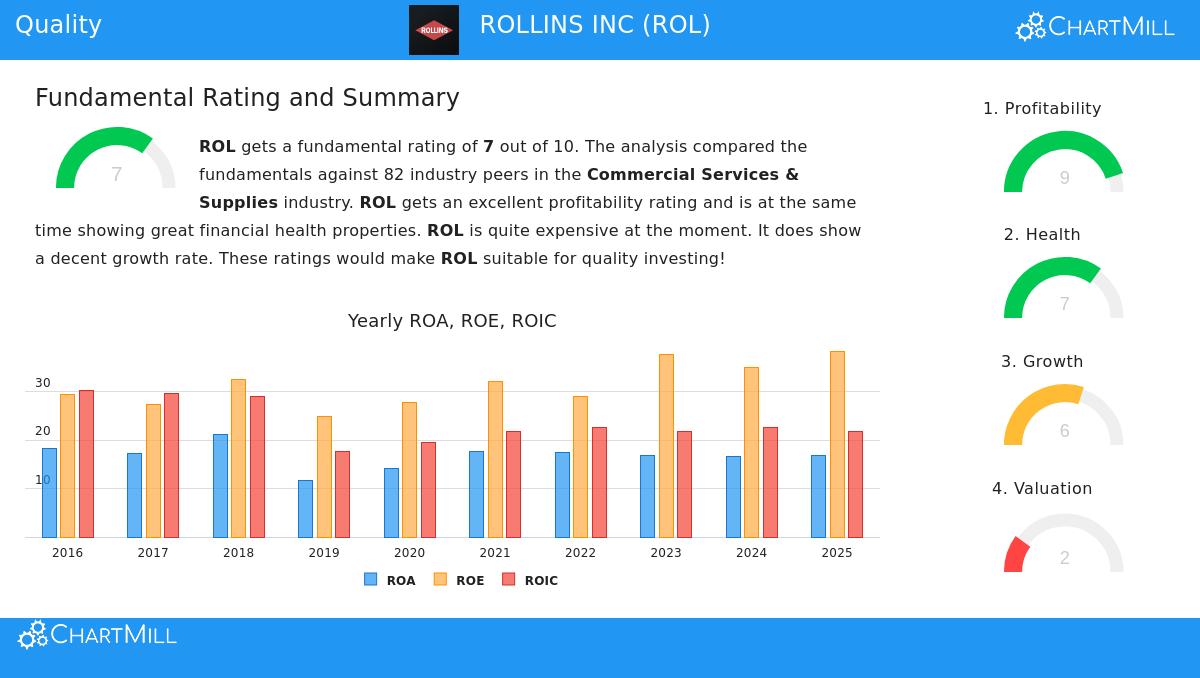

High Capital Use: Maybe the most important measure for quality investors is Return on Invested Capital (ROIC), which calculates how well a company produces earnings from its capital. The screen requires an ROIC (leaving out cash, goodwill, and intangibles) over 15%. Rollins reports a notable number of 128.42%, showing a model with few physical assets and high efficiency that creates large returns on each dollar invested. This is a sign of a wide economic moat.

-

Financial Stability and Cash Flow Strength: The method stresses financial soundness by requiring debt to be below five times free cash flow (FCF), enabling fast debt reduction if necessary. Rollins is very solid here, with a Debt/FCF ratio of 0.94, meaning it could pay off all debt in less than a year using its present cash flow. Also, the screen checks for "quality" earnings by requiring a five-year average ratio of FCF to net income above 75%. Rollins's number of 117% shows it turns all of its accounting profit into actual, usable cash—and more—pointing to high earnings quality and no need for aggressive accounting.

A Top-Level Fundamental View

A look at Rollins's detailed fundamental analysis report supports the results from the screen. The report gives the firm a good total rating of 7 out of 10, with special force in two areas key to quality investing:

-

Outstanding Profitability: Rollins receives a profitability grade of 9, nearly perfect. It is best in its field for main measures like Return on Equity (38.32%), Profit Margin (14.00%), and Operating Margin (19.30%). The report states these margins have been increasing in recent years, supporting the trend of better efficiency found by the screen.

-

Sound Financial Condition: With a health grade of 7, the company shows solid footing. Its Altman-Z score indicates a very small chance of bankruptcy, and its low Debt/Equity ratio confirms it does not depend too much on loans. While standard liquidity ratios (Current and Quick Ratio) seem low, the report explains this by noting the company's very good solvency and profitability, suggesting the ratios may be less important for this particular, steady service-business model.

The main warning, as is common with high-grade franchises, is price. The report gives a low valuation grade of 2, stating Rollins sells at a higher price than both the wider market and its industry based on P/E ratios. For the quality investor, this highlights the method's central idea: one must accept paying a reasonable price for a superior business, but the higher price requires belief in the firm's long-term lasting strengths.

Is Rollins a "Caviar Cruise" Stock?

Judging by the numerical filters of the Caviar Cruise method, Rollins Inc. shows a strong case for quality investors. It displays the wanted mix of stable growth, high profitability through large returns on capital, very strong financial condition, and excellent cash flow conversion. These are the clear signs of a business with a firm competitive place in the necessary pest control market—a service with repeating income traits that is mostly unaffected by economic shifts.

While the present market price seems high, the quality investing method is essentially about long-term ownership of better companies. The measures suggest Rollins has the operational and financial capacity to possibly validate that higher price over time through steady performance.

Interested in reviewing other firms that meet the Caviar Cruise quality screen? You can locate and adjust the screen for your own study here.

Disclaimer: This article is for information and learning only. It is not meant as investment guidance, a suggestion, or an offer or request to buy or sell any securities. The study is based on given data and described screens, which may update. Investors should do their own complete research and review, thinking about their personal financial situation and risk comfort, before making any investment choices.