For investors looking for a disciplined, long-term way to build wealth, few strategies have the substance of Peter Lynch's method. The famous manager of the Fidelity Magellan Fund supported a "growth at a reasonable price" (GARP) idea, concentrating on companies with solid, lasting earnings growth that trade at prices connected to their basics. His method stresses financial soundness, earnings power, and a clear plan for operations, preferring consistent performers over risky ventures. A filter using Lynch's main ideas recently found Parsons Corp (NYSE:PSN) as a possible option, deserving more study for investors who follow this careful, price-aware growth investment method.

Matching the Lynch Standards

Parsons seems to fit several of Peter Lynch's number-based filters, which are made to find sound, expanding companies without paying too much for that expansion. The given information shows the company reaches important marks:

- Lasting Earnings Growth: Lynch looked for companies with a shown history of growth, but was cautious of very high rates. Parsons' five-year average EPS growth of 26.7% easily passes Lynch's lowest point of 15%, while staying under his higher warning line of 30%. This points to a past of good, yet possibly steady, increase.

- Sensible Price via PEG: A central part of the Lynch method is the Price/Earnings to Growth (PEG) ratio, which tries to place a stock's P/E ratio next to its growth rate. A PEG ratio at or under 1.0 implies the market may not be completely counting the company's growth path. Parsons' PEG ratio of 0.71, based on its past five-year growth, shows it could be trading at a sensible, or even interesting, price next to its historical earnings increase.

- Good Earnings Power (ROE): Lynch liked companies that effectively produce profits from shareholder money. A Return on Equity (ROE) above 15% is a sign of this effectiveness. Parsons' ROE of 15.1% meets this mark, suggesting leadership is using capital well to build value for shareholders.

- Sound Financial Health: To limit high risk, Lynch focused on balance sheet firmness. His filters often asked for a Debt-to-Equity ratio under 0.6 and a Current Ratio above 1.0. Parsons shows care here too, with a Debt/Equity ratio of 0.49 and a Current Ratio of 1.67. These numbers indicate a controlled debt amount and enough cash to meet near-term needs, lowering money risk for long-term owners.

Company Outline and Basic Summary

Parsons Corp works as a technology company in national security and important infrastructure markets. Its tasks include cyber and intelligence, missile defense, transportation, and environmental cleanup, mainly helping U.S. government groups and worldwide infrastructure customers. This plan for operations fits with Lynch's liking for clear, if not always exciting, businesses that offer necessary services. The company's combined focus on lasting government needs and updating worldwide infrastructure hints at a path for ongoing, steady demand.

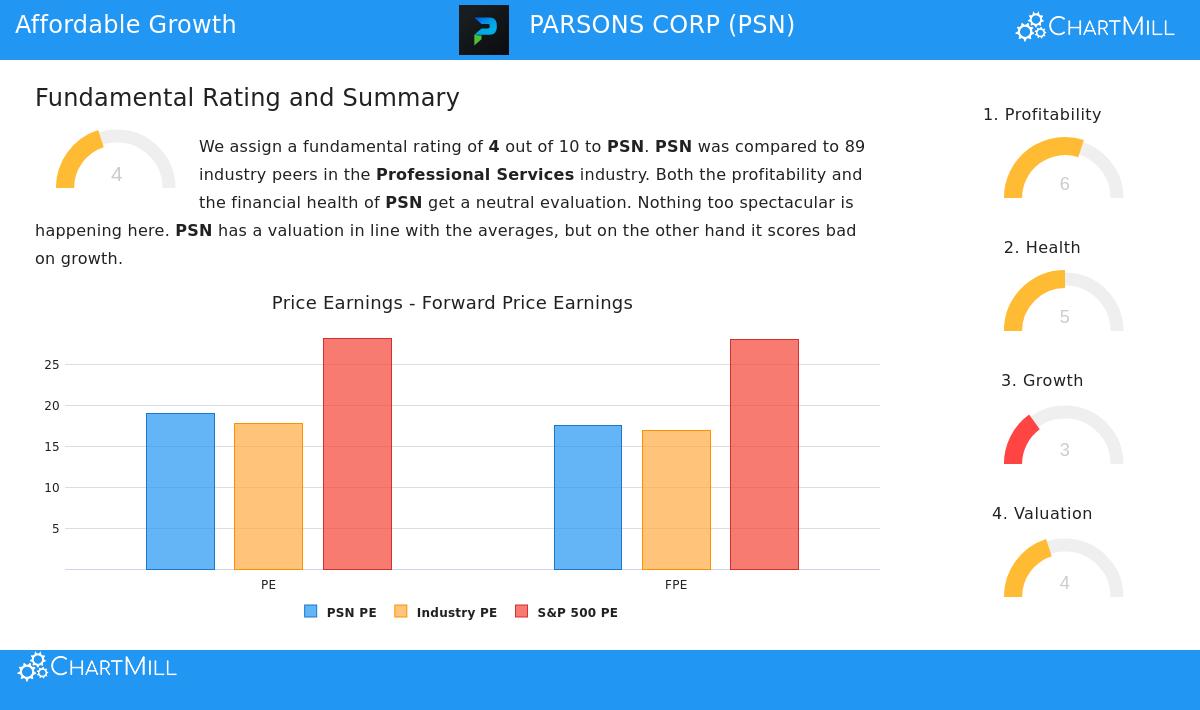

A top-level check of the company's basic study report gives an even view. The report gives Parsons a total score of 4 out of 10, seeing average financial health and earnings power but an absence of strong recent growth speed.

- Earnings Power is seen as a relative plus (score of 6/10), with good notes for steady profits, solid Return on Equity, and getting better margins over time.

- Financial Health gets a medium score (5/10). The company's ability to pay debts, including its low debt amounts, are seen positively, though the report notes the Return on Invested Capital (ROIC) is now under its cost of capital.

- Price is viewed as acceptable (score of 4/10). While its P/E ratio is seen as high next to its own history, it looks more sensible compared to both the wider S&P 500 and its industry group, especially when thinking about its growth picture.

- Growth is the part noted for watch (score of 3/10). Although the company has a very good long-term EPS growth rate, earnings shrank a little over the past year. Future guesses point to a more measured, though still sound, growth rate in the low double-digits.

Fit for GARP Investors

For the growth-at-a-sensible-price investor, Parsons offers an interesting example. It represents the Lynch model of a company with a shown history of large earnings growth (the "G" in GARP) that is now trading at a PEG ratio hinting the market may not be overpricing that past result. The company's good ROE and careful balance sheet meet the quality checks that are key for long-term keeping, limiting risk while letting investors take part in the company's future.

The basic report's notes on dropping growth speed are a key part of the study. A true GARP investor must judge if the recent slowing is a short break or a new standard, and if the present price (PEG of 0.71) properly makes up for this changed growth view. The company's place in steady, government-related areas may give some trust in the lasting nature of its future money flows.

Finding More Investment Options

Parsons Corp came from a specific filter built on Peter Lynch's ideas. For investors wanting to find other companies that pass similar checks for lasting growth, sensible price, and financial firmness, the filter is a helpful beginning for more study.

You can find the full filter and its present results here: Peter Lynch Strategy Stock Filter.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a deal or request to buy or sell any securities. The study is based on given information and shows a specific investment plan. Investors should do their own full study and think about their personal money situation before making any investment choices.