For investors looking for a dependable source of passive income, a systematic selection method is important to distinguish truly lasting dividend payers from unreliable high-yield options. One useful technique focuses on finding companies that have both a good dividend score and also show firm basic financial condition and earnings. This method emphasizes the longevity of the dividend, confirming the company has the business ability and cash generation to continue and possibly increase its distributions over the long term, instead of only pursuing the largest stated yield.

PRIMORIS SERVICES CORP (NYSE:PRIM) results from such a filter as a possibility deserving more study for dividend-oriented investors. The Dallas-based construction and engineering services company works through its Utilities and Energy divisions, catering to a varied group of clients in North America.

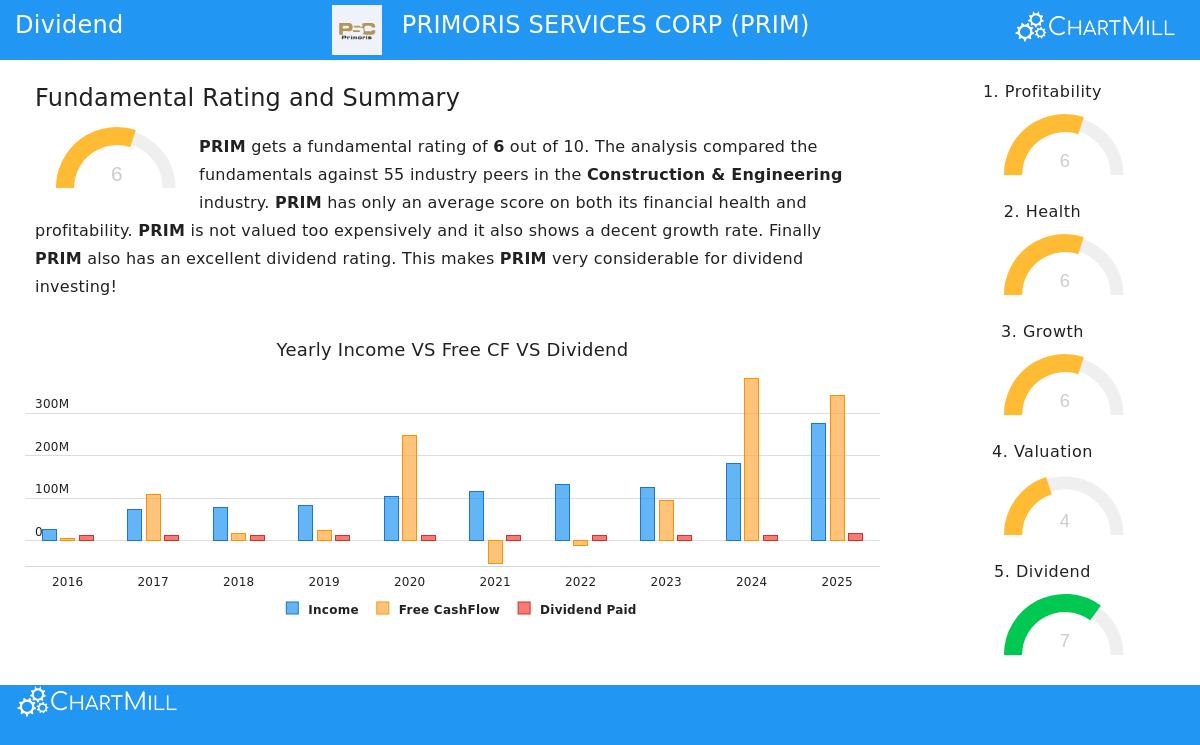

Examining the Dividend Details

The main attraction for income investors is found in PRIM's dividend traits, which are assessed in its fundamental analysis report. The company receives a solid ChartMill Dividend Rating of 7 out of 10, representing a measured review of yield, increase, and security.

- Dependable History: PRIM has a respectable dividend record, having distributed and, importantly, not reduced its dividend for a minimum of ten straight years. This regularity fosters investor trust in management's dedication to sharing capital.

- Secure Increase: The dividend displays a sound, stable rising path, with a typical yearly increase rate near 6% over the last five years. This rise is backed by profits that are rising at a quicker rate, showing the raises are adequately supported and not overextending the company's resources.

- Cautious Payout Ratio: Possibly the most important measure for security is the payout ratio. PRIM distributes only around 6.3% of its net profit as dividends. This very small ratio offers a wide safety margin, making the dividend safe even if profits experience short-term challenges and allowing significant space for putting money back into the business and future dividend raises.

While its total dividend yield of 0.22% is low relative to the wider S&P 500 average, it is useful to consider this within its setting. Inside its own Construction & Engineering field, PRIM’s yield is in fact appealing, positioned above 85% of similar companies. This shows the filter method's benefit: it finds companies with strong dividend caliber inside their industry, instead of only pointing out the largest yields that might involve more danger.

Backing Basics: Earnings and Financial Condition

A lasting dividend needs a profitable and financially stable business. This is why the filter rules require "acceptable" scores in these parts, and PRIM meets this.

Earnings are satisfactory, with a ChartMill Profitability Rating of 6. The company is regularly profitable and produces positive cash flow. Important return measures like Return on Equity (16.35%) and Return on Invested Capital (11.53%) stack up well against industry counterparts, showing productive use of investor capital. While gross margins are somewhat narrow,a trait of the contract-based construction business,operating and net margins have displayed good progress in recent periods.

Financial Condition is similarly rated a 6, showing a steady balance sheet. The review shows multiple positive points:

- A good Altman-Z score of 4.35 implies a very small short-term bankruptcy danger.

- A small Debt-to-Equity ratio of 0.24 and a very good Debt-to-Free-Cash-Flow ratio of 1.38 indicate the company is not excessively indebted and can settle its debts promptly from operational cash flow.

- Liquidity measures are consistent with industry norms, showing enough ability to handle immediate requirements.

These aspects in earnings and condition are not just theoretical scores; they are the basic supports that let PRIM reliably maintain its long-term dividend plan. A firm balance sheet means the dividend is less probable to be reduced during a sector slump, and steady earnings supplies the profits to finance it.

Price and Expansion Factors

From a price standpoint, PRIM seems fairly valued inside its sector. Its Price-to-Earnings ratio is smaller than almost 75% of its industry counterparts, hinting it is not excessively priced in spite of its dependable features. The company also shows firm expansion, with sales and earnings per share having risen markedly over the previous year and longer spans. While experts anticipate this expansion speed to slow in the future, the forecasted numbers stay positive, backing the argument for ongoing dividend steadiness.

Is PRIM Suitable for a Dividend Portfolio?

PRIMORIS SERVICES CORP offers a persuasive argument for investors whose plan stresses dividend dependability and increase over seeking large, possibly dangerous yields. It illustrates the product of a careful filter method: a company with an extended, uninterrupted history of dividend distributions, a very cautious payout ratio that guarantees security, and the basic earnings and financial condition to maintain its capital return plan through economic variations. It is a stock that appears designed for the "purchase and keep" portion of a varied income portfolio.

For investors wanting to investigate other companies that meet comparable strict filters for dividend caliber, condition, and earnings, the ready-made Best Dividend Stocks screen gives a prepared beginning point for more investigation.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and ratings provided by ChartMill, which are derived from historical and estimated figures. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions. Past performance is not indicative of future results.