For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) method presents a practical middle path. This method tries to find companies that are increasing their earnings and sales at a good rate, but whose stock prices are not excessively high. It steers clear of the speculative edges of expensive, unprofitable growth companies on one side and very cheap but slow-moving businesses on the other. By applying a methodical filter to sort for stocks with good growth grades, acceptable financial condition and earnings, and a fair valuation grade, investors can effectively find possible GARP selections. One company that appears from this filter is Primoris Services Corp (NYSE:PRIM), a national specialty contractor working in the utility and energy infrastructure sectors.

Growth Path: A Main Asset

The main attraction of Primoris for a GARP method is its clear and solid growth, which gives the company a ChartMill Growth Grade of 7 out of 10. The company's latest financial results display notable forward movement, an important element for any investment focused on growth.

- Earnings Increase: Primoris has reported notable profit growth, with Earnings Per Share (EPS) rising 65.79% over the previous year. This is not an isolated occurrence; the company has kept a good average yearly EPS growth rate of almost 19% over recent years.

- Sales Movement: Sales growth is similarly strong. Revenue grew by 21.45% in the last year, aided by a firm multi-year average growth rate above 15%.

- Future Projection: Analysts believe this favorable pattern will persist, with predicted average yearly growth rates of about 15% for EPS and 9% for revenue in the next few years.

This steady history of turning sales increases into even quicker profit growth is a sign of a business scaling effectively, making it a valid selection for portfolios focused on growth.

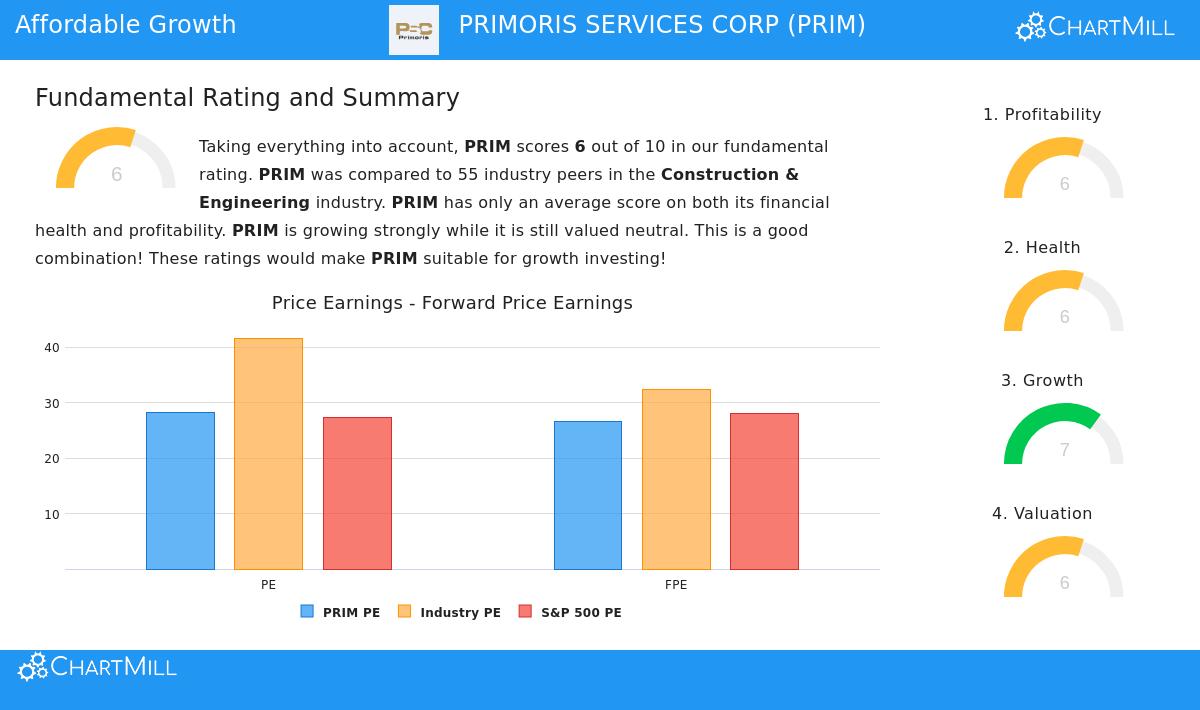

Valuation: Fair Given the Situation

A stock with good growth can still be a bad investment if the cost is too great. This is where the "reasonable price" part of the GARP method is essential. Primoris gets a ChartMill Valuation Grade of 6, suggesting a balanced, if not low, price when considered from different angles.

- Absolute vs. Relative P/E: Initially, a trailing Price-to-Earnings (P/E) ratio of 28.29 might appear high. However, the situation matters. This price is meaningfully lower than the industry average, with almost 75% of its construction and engineering competitors trading at higher P/E multiples. It is also about the same as the wider S&P 500.

- Cash Flow and EBITDA Measures: More indicative are the prices based on cash production. Primoris trades at a good discount to the industry based on its Price-to-Free-Cash-Flow and Enterprise Value-to-EBITDA ratios, doing better than over 85% and 63% of competitors, in that order.

- Growth Consideration: Maybe the most applicable measure for a GARP investor is the PEG ratio, which modifies the P/E for anticipated earnings growth. Primoris's low PEG ratio indicates the market's current price does not completely account for its expected growth path, a good sign for investors mindful of value.

Supporting Basics: Condition and Earnings

For growth to be lasting and the price to be valid, a company must rest on a firm operational and financial base. Primoris's grades in these areas, while not outstanding, offer needed support for the GARP argument.

The company receives a ChartMill Profitability Grade of 6. Its profit measures—Return on Assets (5.96%), Return on Equity (17.03%), and Return on Invested Capital (12.01%)—all put it in the top half of its industry. While its gross profits are somewhat narrow, a typical feature in contracting, its operating profit has displayed good progress. The important point is that Primoris is clearly profitable and produces returns above its capital costs, creating real value for shareholders as it expands.

Financial condition, with a grade of 6, is satisfactory. The balance sheet indicates an acceptable Debt-to-Equity ratio of 0.26, which is superior to most industry competitors. Its Debt-to-Free-Cash-Flow ratio is a very good 0.99, showing it could pay off all debt in under a year with its present cash flow. Liquidity, as shown by current and quick ratios, is enough but not a key asset. In summary, the company does not seem to have too much debt, lowering the chance that its growth plans could be interrupted by financial pressure.

Conclusion

Primoris Services Corp illustrates the affordable growth filtering idea. It has the essential element of good, clear growth in both sales and earnings, supported by favorable future projections. Importantly, this growth is not combined with a speculative price; instead, the stock seems fairly valued compared to its industry and future possibility when examined using cash flow and growth-modified measures. Supported by satisfactory earnings and a financially steady situation, Primoris fits the GARP goal of finding active companies without paying a high cost that allows no margin for mistake.

For investors wanting to examine the complete basic analysis that forms the basis for these grades, a complete report is accessible here.

This review of Primoris came from a particular filter for affordable growth stocks. Investors searching to find other companies that fit similar standards of good growth, fair valuation, and firm basics can examine the filter for more possible selections here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a proposal or request to purchase or sell any securities. The review uses data and grades from ChartMill, and investors should perform their own research and talk with a qualified financial consultant before making any investment choices. Previous results do not guarantee future outcomes.