The investment philosophy of Peter Lynch, legendary manager of the Fidelity Magellan Fund, focuses on finding well-run, growing companies trading at reasonable prices, a strategy often termed Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on fundamental health and sustainable growth instead of market timing. His process uses specific filters to find companies with strong profitability, solid financial footing, and valuations that do not overpay for future prospects. A recent screen built on these ideas has identified Perma-Pipe International Holdings (NASDAQ:PPIH) as a possible candidate for investors following this strategy.

Alignment with Lynch's Core Criteria

The screen uses several quantitative rules taken from Lynch's philosophy. Perma-Pipe's financial profile shows a clear alignment with these important benchmarks:

- Sustainable Earnings Growth: Lynch looked for companies growing earnings steadily, but not at an unsustainably fast pace. The screen needs a 5-year EPS growth rate between 15% and 30%. Perma-Pipe's EPS has grown at an average yearly rate of 21.7% over this period, putting it within this target range and indicating a history of manageable, consistent expansion.

- Reasonable Valuation (PEG Ratio): Perhaps the central part of Lynch's valuation method is the PEG ratio, which compares the Price-to-Earnings (P/E) ratio to the earnings growth rate. A PEG of 1 or less suggests the market price may not be fully accounting for the growth potential. Perma-Pipe's PEG ratio, based on its past 5-year growth, is 0.80, indicating the stock could be fairly priced relative to its historical growth path.

- Strong Profitability (Return on Equity): Lynch preferred companies that generate high returns on shareholder equity. The screen requires an ROE above 15%. Perma-Pipe's ROE of 16.2% meets this level, showing efficient use of investor capital to produce profits.

- Financial Health (Debt & Liquidity): A conservative balance sheet was important for Lynch. The screen looks for a Debt-to-Equity ratio below 0.6 and a Current Ratio of at least 1. Perma-Pipe meets these, with a very low Debt/Equity ratio of 0.15 and a Current Ratio of 1.76. This indicates a company funded mainly by equity, not debt, with sufficient liquidity to meet short-term obligations, a sign of financial strength.

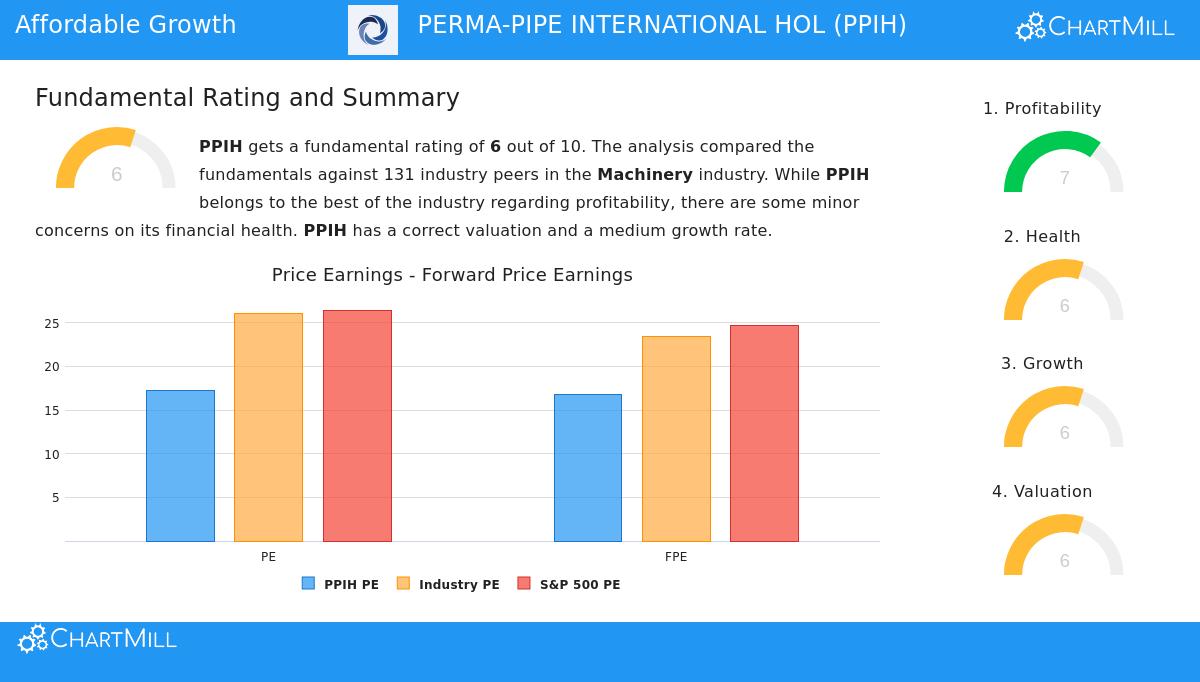

Fundamental Health Check

A wider view of Perma-Pipe's fundamental analysis report, which can be found here, gives a more detailed picture that mainly supports the Lynch screen's findings. The company gets an overall fundamental rating of 6 out of 10.

- Profitability is a clear positive, with a score of 7/10. The company shows very good returns on invested capital (15.1%) and improving operating margins. While the past year's EPS saw a decrease, the strong multi-year growth trend and positive future EPS expectations help explain this.

- Financial Health is rated 6/10. The very low debt levels and positive trends like share count reduction are important positives that fit with Lynch's preferences. The report notes some smaller concerns about liquidity ratios compared to industry peers, but the overall solvency picture, supported by a healthy Altman-Z score, stays firm.

- Valuation scores 6/10, described as "correct." While the standard P/E ratio seems high on its own, the analysis confirms that when compared to the industry and the S&P 500, and, importantly, when adjusted for growth via the PEG ratio, the valuation seems more favorable.

- Growth receives a neutral score of 6/10. The story here is mixed but leans positive for a GARP investor. The company has shown very strong revenue growth over the past year and is expected to increase both revenue and earnings growth in the coming years, which may support its current valuation multiple.

The GARP Investment Thesis

For an investor using Peter Lynch's GARP framework, Perma-Pipe presents a strong case. It works in the essential, if unexciting, sector of specialty piping systems, exactly the type of "dull" business Lynch thought could be a good investment. The quantitative screen confirms it has the key traits Lynch valued: a history of sustainable earnings growth, high profitability on equity, a very strong balance sheet with little debt, and a valuation that accounts for its growth profile.

The fundamental report adds detail, pointing out strong operational execution through high returns on capital and confirming that future growth expectations are healthy. The minor points of concern, such as recent liquidity metrics, are likely less important for a long-term holder focused on the company's lasting competitive strengths and financial discipline.

Exploring Further

The Peter Lynch strategy screen that found Perma-Pipe International Holdings can produce other possible investment ideas. Investors curious about finding more companies that match this disciplined growth-at-a-reasonable-price model can view the full screen results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and a predefined screening method; it does not consider your individual investment objectives, financial situation, or needs. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.