For investors looking for chances in the market, the principles of value investing provide a proven structure. Fundamentally, this method is about finding companies trading for less than their intrinsic value, that is, locating stocks the market has valued lower than the basic business is likely worth. This method, established by Benjamin Graham and notably used by Warren Buffett, stresses a margin of safety and a concentration on basic business strength instead of short-term price changes. A systematic way to use this method is to filter for companies that are basically inexpensive according to valuation measures, but still show good basic business results regarding earnings, financial strength, and expansion. One stock that recently appeared from such a filtering process is Pilgrim's Pride Corp (NASDAQ:PPC).

Examining the Valuation

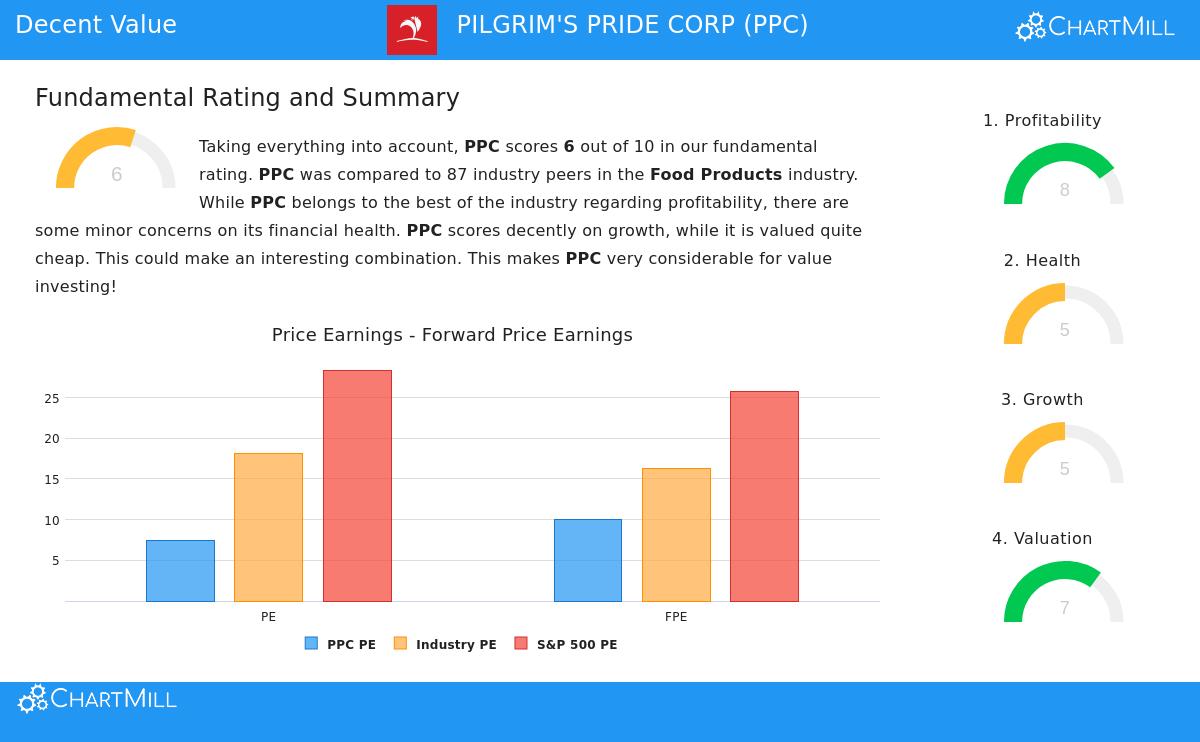

The main attraction of PPC for a value-focused investor is found in its notable valuation measures. According to ChartMill's basic analysis, the stock receives a good Valuation Rating of 7 out of 10. This rating comes from several important ratios that imply the market may be valuing the company cautiously.

- Price-to-Earnings (P/E) Ratio: At 7.39, PPC's P/E ratio is much lower than both the S&P 500 average (28.39) and its industry group in the Food Products sector. The analysis shows PPC is less expensive than 93% of the companies in its industry based on this measure.

- Forward P/E Ratio: Looking forward, the Price/Forward Earnings ratio of 10.02 also presents a view of a fairly valued stock, less expensive than 92% of its industry rivals.

- Enterprise Value to EBITDA: This measure, which includes debt, gives more support to the valuation argument, showing PPC is valued lower compared to 86% of its industry.

For a value investor, these numbers are the beginning. A low valuation compared to earnings and cash flow can signal a possible gap between the stock's price and the company's capacity to produce profit, forming the "margin of safety" that is key to the method.

Evaluating Financial Strength and Earnings

An inexpensive stock is only a sound investment if the company is financially stable. This is where the "value trap" danger appears, a stock that seems cheap but is linked to a weakening business. PPC's basic report gives a varied but mostly satisfactory view of its financial position, with a Health Rating of 5.

On the good side, the company's Altman-Z score of 3.86 points to a low short-term danger of bankruptcy and is stronger than 79% of its peers. Its Debt to Free Cash Flow ratio of 3.73 is also seen positively, suggesting it could in theory pay off all debt in less than four years using its present cash flow. Still, investors should be aware of some points for attention, including a Debt-to-Equity ratio of 0.87, which shows a moderate use of debt financing, and a Quick Ratio of 0.78, which may indicate some limits in meeting immediate liabilities without selling inventory.

Where PPC truly does well is in earnings. It has a high Profitability Rating of 8. Main strong points include:

- High Returns: A Return on Equity of 34.73% and a Return on Invested Capital of 19.90% are some of the best in its industry, doing better than over 96% of peers.

- Good and Getting Better Margins: The company's Profit Margin of 6.70% and Operating Margin of 9.53% are above the industry middle point and have gotten better in recent years.

For the value investor, strong earnings are vital. It confirms the business model, implies efficient management, and supplies the profit generation that, if maintained, should in time be seen in a higher stock price.

Expansion Path and Dividend Factor

Expansion is the last part of the analysis, as it helps judge a company's future intrinsic value. PPC's Growth Rating is a neutral 5, showing a story of strong past results meeting near-term challenges.

The company has achieved notable historical expansion, with Earnings Per Share (EPS) growing over 27% on average each year in recent years. Revenue has also grown at a good rate of over 9% per year. However, analyst projections point to a possible reduction in pace, with EPS expected to fall a little in the next few years. This expected slowdown probably adds to the stock's lower valuation now. The value investing idea often involves seeing past temporary cyclical drops or negative projections if the central business stays profitable and financially sound.

A noticeable feature for income-focused value investors is PPC's large dividend yield, presently close to 20%. While the report mentions the dividend history is not long, the size of the yield adds another part of possible return while an investor waits for a potential valuation improvement.

Is PPC a Fit for a Value Portfolio?

Filtering for stocks with sound valuation, acceptable health, and strong earnings is a useful way to find possible value chances. Pilgrim's Pride Corp presents a situation that matches several of these points. It seems basically inexpensive on several valuation measures, runs a very profitable central business, and keeps an acceptable, though not perfect, financial health picture. The expected slowdown in earnings expansion presents a clear risk and is probably the main reason for its low valuation, representing the typical value investor's test of telling a short-term problem from a lasting drop.

The mix of a low P/E ratio, high earnings returns, and a large dividend yield makes PPC a stock deserving of more detailed study for investors using a value-based method.

Interested in locating more stocks that match this "acceptable value" description? You can perform a similar filter using the ChartMill Stock Screener to look at other possible chances.

Disclaimer: This article is for information only and does not form financial advice, a suggestion, or an offer or request to buy or sell any securities. The analysis is based on data and ratings from ChartMill, and investors should do their own complete research and think about their personal financial situation before making any investment choices. Past results are not a guide for future outcomes.