For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish solid dividend payers from hazardous yield traps. One useful method focuses on companies that provide a good dividend while also having the fundamental financial soundness to maintain and possibly raise those payments. This method frequently uses combined scores that assess a stock's dividend quality, earnings power, and balance sheet condition together. By applying minimum standards for these scores, investors can efficiently find companies where the dividend is backed by a firm operational base, lowering the chance of future reductions and improving the possibility for lasting, cumulative gains.

POOL CORP (NASDAQ:POOL), the top wholesale distributor of swimming pool supplies and similar outdoor living products, appears as a result from this kind of screening method. The company's basic profile indicates it could deserve additional examination from investors focused on income.

Dividend Dependability and Increase

The primary attraction for dividend investors is found in POOL CORP's history and present yield. The company’s dividend traits show a dedication to giving capital back to shareholders.

- Reasonable and Rising Income: The stock has a dividend yield of 2.30%, which is fair by itself but gains more weight when measured against wider indexes. This yield exceeds the present S&P 500 average and places in the higher range of its industry group. Significantly, the dividend has a good record of increase, having risen at a notable yearly rate of about 17.5% over the last five years.

- Longstanding History: Steadiness is vital in dividend investing. POOL CORP has built a dependable history, having distributed dividends for a minimum of ten years without a decrease. This past record offers some assurance of management's dedication to the shareholder payment.

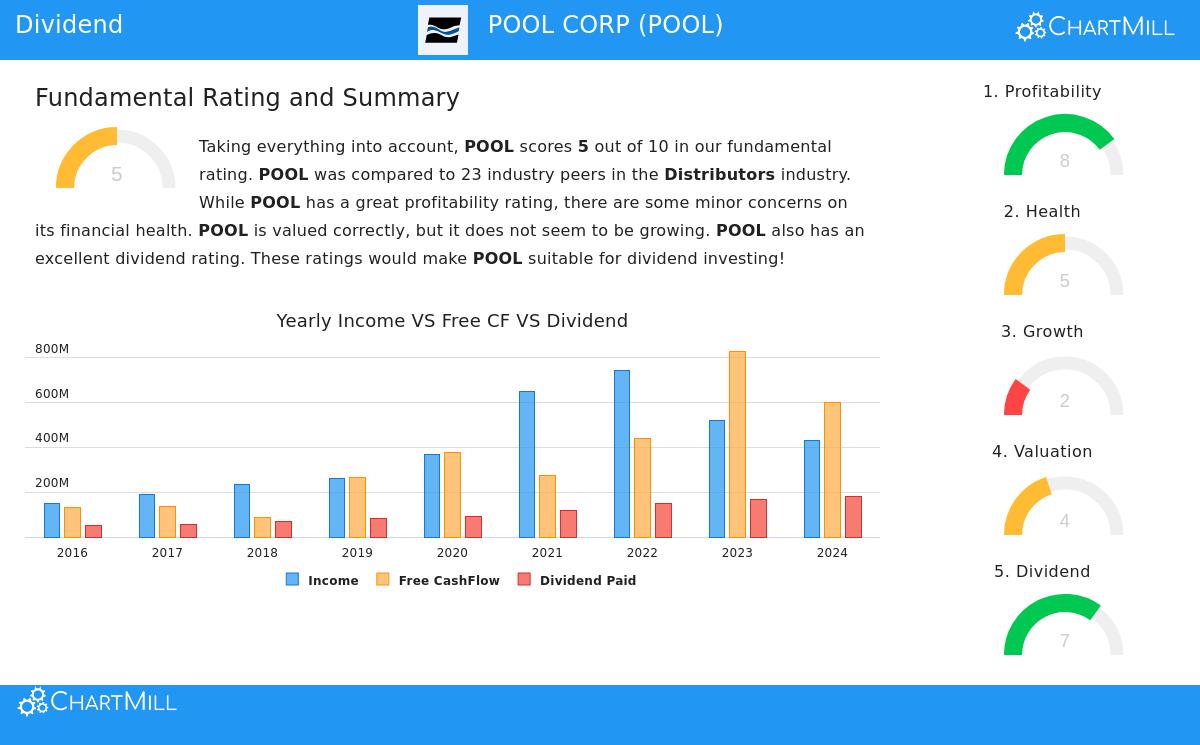

- A Point on Maintainability: While the payout ratio, the share of profits paid as dividends, is at a workable 44.9%, the basic report notes an area for attention. The recent increase rate of the dividend has been faster than the increase rate of profits. This difference implies the remarkable historical dividend increase speed might slow to match profit growth more closely going forward, a typical factor for established dividend payers.

Supporting Basics: Earnings Power and Condition

A high dividend is only as secure as the company’s capacity to keep it. This is where the screening standards for good earnings power and balance sheet condition show their value, and POOL CORP performs well on these supporting aspects.

Earnings Power: The company receives a high ChartMill Profitability Rating of 8, indicating effective operations. Important measures are notable:

- Strong Returns: The company produces a solid Return on Equity (ROE) of 29.72% and a good Return on Invested Capital (ROIC) of 16.15%, both numbers placing it near the top in its field. High returns on capital are a sign of a good business with a lasting market position.

- Good Margins: POOL CORP keeps firm operating and profit margins that exceed most of its rivals, showing cost control and operational effectiveness.

Satisfactory Balance Sheet Condition: With a ChartMill Health Rating of 5, the company’s financial state is viewed as acceptable, though with certain details. The balance sheet displays both positive features and points to note:

- Stability: The company has a sound Altman-Z score, showing little short-term default risk. Its debt amounts compared to free cash flow are workable, indicating it could settle debts in a practical period.

- Cash Flow Note: The current ratio is firm, but the quick ratio, which leaves out inventory, is under 1.0. This is not unusual for a distribution company that carries large inventory, but it is an element investors should note within the framework of the company’s total cash generation.

Price and Expansion Background

For a dividend investor with a lengthy time frame, price and expansion possibilities give background for the overall return potential.

- Price: POOL CORP’s valuation seems acceptable within its market setting. Its Price-to-Earnings (P/E) ratio is more favorable than both the wider S&P 500 and the norm for its industry. This implies the market is not valuing its profits and dividend stream too highly.

- Expansion View: The company’s recent profit expansion has been slight, but analyst forecasts indicate a return of mid-single-digit expansion in both sales and earnings per share in the next few years. This expected expansion is important as it offers the possible base for future dividend raises.

Summary

POOL CORP offers an example of using a multi-part screen for dividend investing. The stock satisfies the first standards by providing a fair and rising yield supported by a ten-year reliable payment history. Importantly, this dividend is upheld by the company’s central advantages: excellent earnings power measures that indicate a superior business operation and a balance sheet condition that, while not flawless, shows adequate steadiness. The acceptable price and constructive expansion view further complete the profile for a possible lasting investment.

For investors wanting to investigate other companies that meet similar filters for dividend quality, earnings power, and balance sheet condition, the pre-set "Best Dividend Stocks" screen can act as a beginning for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. The analysis is based on data provided and current market conditions, which are subject to change.