For investors aiming to construct a portfolio using value investing principles, the central task is finding companies that trade below their intrinsic value. This established method, created by Benjamin Graham and used by Warren Buffett, requires a systematic hunt for stocks where the market price seems separate from the basic business facts. A useful method for this hunt is to filter for companies that display good financial condition and earnings, indicate a chance for expansion, and, most importantly, are valued much lower than similar companies and the overall market. This mix points to a margin of safety, a protection against error that is fundamental to the value approach.

PACIRA BIOSCIENCES INC (NASDAQ:PCRX) is a pharmaceutical company centered on non-opioid pain control and regenerative health answers. Its marketable products consist of EXPAREL, a long-lasting local pain reliever for postsurgical pain, ZILRETTA for osteoarthritis knee pain, and the iovera® cryotherapy device.

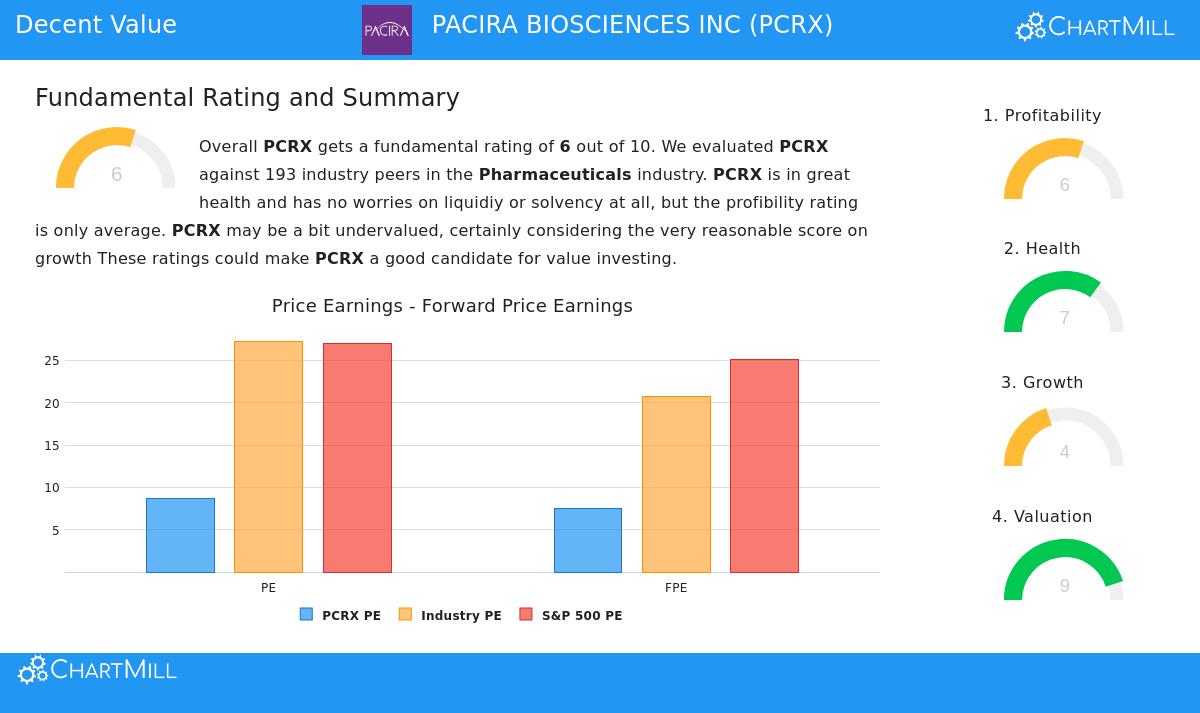

A Notable Valuation Picture

The strongest point for PCRX as a possible value chance is found in its valuation numbers. According to ChartMill's fundamental analysis report, the stock gets a high Valuation Rating of 9 out of 10. This grade comes from a detailed examination of important price multiples, which together show a stock priced at a large discount.

- Price-to-Earnings (P/E): PCRX has a P/E ratio of 8.69. This is much lower than the S&P 500 average of 27.03 and also less than about 93% of similar companies in the pharmaceuticals industry.

- Forward P/E: For the future, the valuation seems even more appealing with a forward P/E ratio of 7.45, again placing it as less expensive than over 93% of industry rivals.

- Cash Flow and EBITDA: The value case goes past earnings. The company's Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios are also in the least expensive quarter of its industry, meaning the market is using a low multiple on its cash production and operational earnings.

For a value investor, these numbers are the beginning. A low P/E ratio can sometimes point to basic issues, but when combined with acceptable grades in other important areas, as seen here, it can instead mark a possible market pricing error ready to be fixed.

Evaluating Financial Condition and Earnings

An inexpensive stock is only a sound investment if the company is financially stable and able to produce earnings. This is where the "margin of safety" idea is vital; good basic facts supply the protection that guards the investment case. PCRX's report indicates a firm base.

Financial Condition (Rating: 7/10): The company shows good liquidity, a main sign of its capacity to handle immediate responsibilities and endure economic slumps.

- Its Current Ratio of 4.54 and Quick Ratio of 3.28 are sound, indicating sufficient resources to cover debts.

- The Debt-to-Free Cash Flow ratio of 2.72 is positive, implying it would need less than three years of present cash flow to settle all debt, a better result than 92% of its industry peers.

Earnings (Rating: 6/10): While there are some notes about decreasing margins compared to last year, PCRX's earnings picture stays fair relative to its sector.

- The company keeps positive earnings and operating cash flow.

- Important efficiency ratios like Return on Assets (0.56%), Return on Equity (1.01%), and Return on Invested Capital (2.67%) all place in the top 20-21% of the pharmaceuticals industry.

- A very high Gross Margin of 79.39% beats 85% of peers, showing strong pricing ability or cost management at the core production stage.

This mix is significant for the value plan. It suggests the business is steady and operationally efficient, lowering the chance that the low valuation is just a "value trap", an inexpensive stock that stays inexpensive because of worsening basic facts.

Expansion Factors and the Full View

Strict value stocks frequently have limited expansion, but the best choice presents a sensible expansion route to help drive a re-valuation. PCRX's Growth Rating of 4/10 shows a varied picture. The last year had decreases in both Revenue and Earnings Per Share (EPS), which probably adds to the stock's low valuation. However, the longer-term and future-looking views give setting.

- Over the last few years, the company has reached an average yearly Revenue expansion of over 11%.

- Analysts predict a move back to expansion, with EPS forecast to rise by an average of over 10% each year in the next few years.

For the value investor, this path is important. The recent softness may be temporary or changing, forming the purchase chance. If the company can get back to its past expansion patterns as predicted, the present low valuation multiples may show to be a short-term irregularity.

Conclusion

PACIRA BIOSCIENCES INC presents a situation that matches several value investing standards. It is valued at a steep discount to both the market and its industry based on normal earnings and cash flow measures. This low valuation is joined with a sound financial state, marked by healthy liquidity and workable debt, and an earnings picture that, while showing some recent strain, stays in the race. The expected return to earnings expansion supplies a possible trigger for the market to re-evaluate its price.

As with any investment, careful examination is necessary. Investors should think about the particular tests the company faces, including recent revenue patterns and margin pressure. However, for those filtering for fair value chances, stocks with good valuation, condition, earnings, and expansion traits, PCRX justifies a more detailed examination.

This examination used a "Decent Value" filtering plan. You can locate more stocks that match similar standards by using the predefined ChartMill stock screener.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to purchase or sell any securities. The examination is based on data and grades given by ChartMill, and investors should do their own separate research and talk with a qualified financial advisor before making any investment choices.