For investors looking for a systematic, long-term way to build wealth, few strategies hold the authority of Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported putting money into what you understand, concentrating on firms with clear operations, durable expansion, and good finances. His system is frequently called a "growth at a reasonable price" (GARP) method, seeking to find firms increasing earnings at a solid rate but not selling at extreme prices. A central instrument for using this thinking is a stock screener that sorts for particular measures linked to earnings, financial strength, and price.

One firm that recently appeared from a Peter Lynch-influenced screen is Newmont Corp (NYSE:NEM), the world’s top gold mining company. For investors who follow Lynch's ideas, Newmont offers an interesting example of a big, well-known business in a basic industry that seems to fit many of his important investment rules.

Fit with Peter Lynch Measures

The heart of Lynch's method includes a group of number-based filters made to distinguish good growth from risky excitement. Newmont's present situation displays a solid fit with a number of these parts:

- Durable Earnings Growth: Lynch looked for firms with a 5-year earnings per share (EPS) increase between 15% and 30%, quick enough to matter but gradual enough to last. Newmont's 5-year EPS increase rate of 21.6% rests well inside this goal area, showing a record of steady, controlled growth.

- Sensible Price Compared to Growth: Maybe the most important Lynch number is the Price/Earnings to Growth (PEG) ratio, which should be at or under 1. This makes sure an investor is not paying too much for the firm's growth path. Newmont's PEG ratio, using its past growth, is 0.91, suggesting its share price could be fairly valued when its historical earnings increase is considered.

- High Profitability: Lynch wanted a high return on equity (ROE) to be certain management was using investor money well. Newmont's ROE of 21.6% is much higher than the 15% lowest limit, putting it with the best in its field and proving very good earnings.

- Cautious Financial Setup: A small debt load was critical for Lynch, who favored a debt-to-equity ratio below 0.6, and preferably under 0.25. Newmont's ratio of 0.17 shows a very careful balance sheet, paid for mainly by equity instead of debt, which gives strength in economic declines.

- Financial Strength: The screen also sorts for a current ratio above 1, making certain a firm can pay its near-term bills. Newmont's current ratio of 2.04 shows good cash availability and financial soundness, a key point for long-term owners.

Basic Health Review

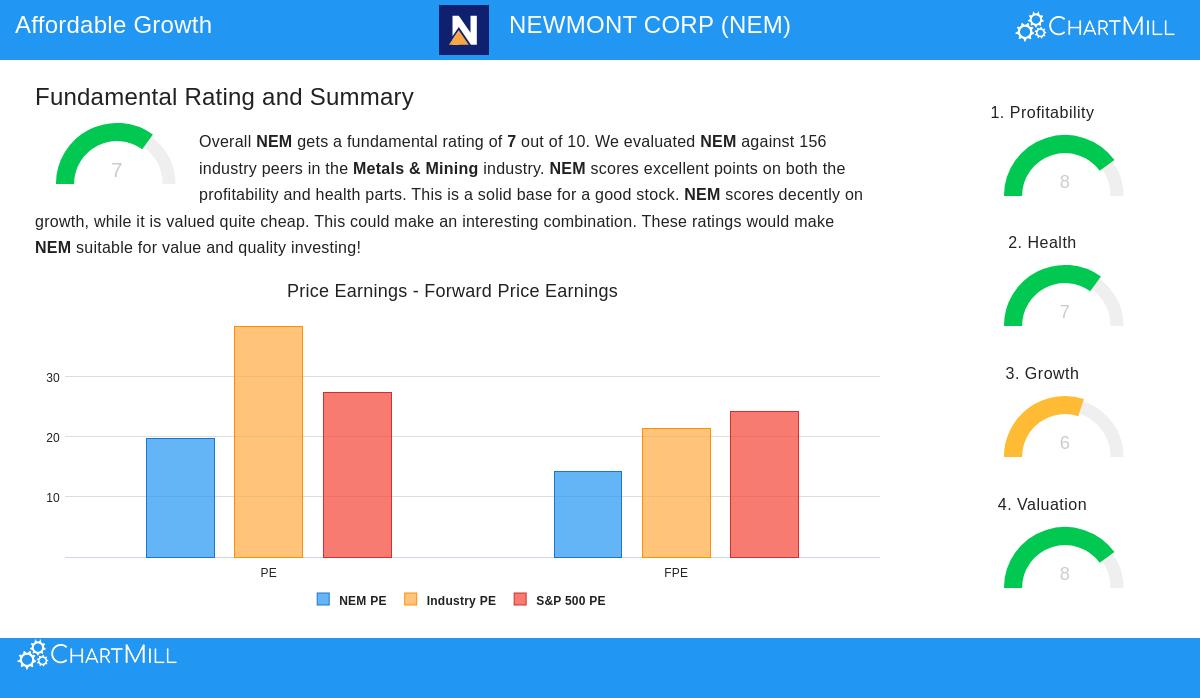

A wider view of Newmont's basic profile supports the image shown by the Lynch screen. Based on a complete basic analysis report, Newmont gets a total score of 7 out of 10, with special good points in earnings and financial strength.

The firm gets a very good profitability score (8/10), led by field-topping margins and returns on capital. Its operating margin over 43% and profit margin above 33% do better than most of its competitors in the metals and mining field. Financially, it scores a firm 7/10, helped by its low debt, good free cash flow, and a sound Altman-Z score pointing to low failure risk.

On price, the report mentions a varied but mostly positive image. While its usual P/E ratio seems high alone, checks against both field competitors and the wider S&P 500 show Newmont is priced more affordably. When growth is considered through the PEG ratio, the price argument becomes firmer. The growth score (6/10) points out very strong past EPS and sales increase, though experts forecast a more measured speed ahead, a change that matches Lynch’s liking for lasting, instead of sudden, growth.

A GARP Possibility in a Standard Field

For the GARP investor, Newmont stands as a interesting option. It works in the frequently ignored and "simple" field of mining, which Lynch might like for its clearness and necessary part in the world economy. The company is not a risky tech newcomer; it is a field frontrunner with physical assets, making large cash flow. The screening outcomes indicate it has produced the kind of profitable, stable-growing results Lynch valued, all while keeping a strong balance sheet.

The mix of solid past growth, high profitability, very little debt, and a sensible PEG ratio makes a profile that matches the "growth at a reasonable price" belief. It is a firm that has grown carefully and seems set to keep doing so, without needing investors to pay extra for unlikely future hopes.

Finding More Investment Options

Newmont Corp is only one instance of a firm that meets a traditional Peter Lynch screen. Investors curious about using this systematic, long-term method to locate other possible choices can view the full screen and its present findings here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a deal to buy or sell any securities. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.