Investors looking for long-term growth chances at fair prices frequently use established methods that mix basic strength with lasting development. The Peter Lynch investment style, explained in his book One Up on Wall Street, gives an organized system for spotting these firms. This process focuses on locating businesses with good but controlled profit increases, sound money condition, and appealing prices compared to their growth potential. Instead of following risky fads, Lynch supported putting money into clear companies with steady performance numbers.

Fitting the Lynch Standards

Newmont Corp (NYSE:NEM) shows various traits that match Peter Lynch's investment thinking. The gold mining firm's money measurements meet a number of important filtering points that Lynch saw as needed for lasting long-term growth.

- Lasting Profit Increase: The firm has reached a five-year EPS growth figure of 21.58%, fitting nicely inside Lynch's chosen span of 15-30%. This shows steady widening without the instability that frequently comes with overly fast growth.

- Appealing Price: With a PEG figure of 0.67, Newmont sells under Lynch's limit of 1.0, hinting the share might be priced low compared to its past growth path.

- Careful Money Setup: The firm keeps a debt-to-equity figure of 0.17, much under Lynch's highest limit of 0.6 and even below his chosen mark of 0.25, showing little need for outside loans.

- Good Cash Position: A current ratio of 2.04 shows sound near-term money health, passing the lowest need of 1.0 and giving extra safety against market changes.

- Money-Making Work: Newmont's return on equity of 21.63% greatly beats the 15% lowest Lynch wanted, showing good use of owner money.

Basic Review

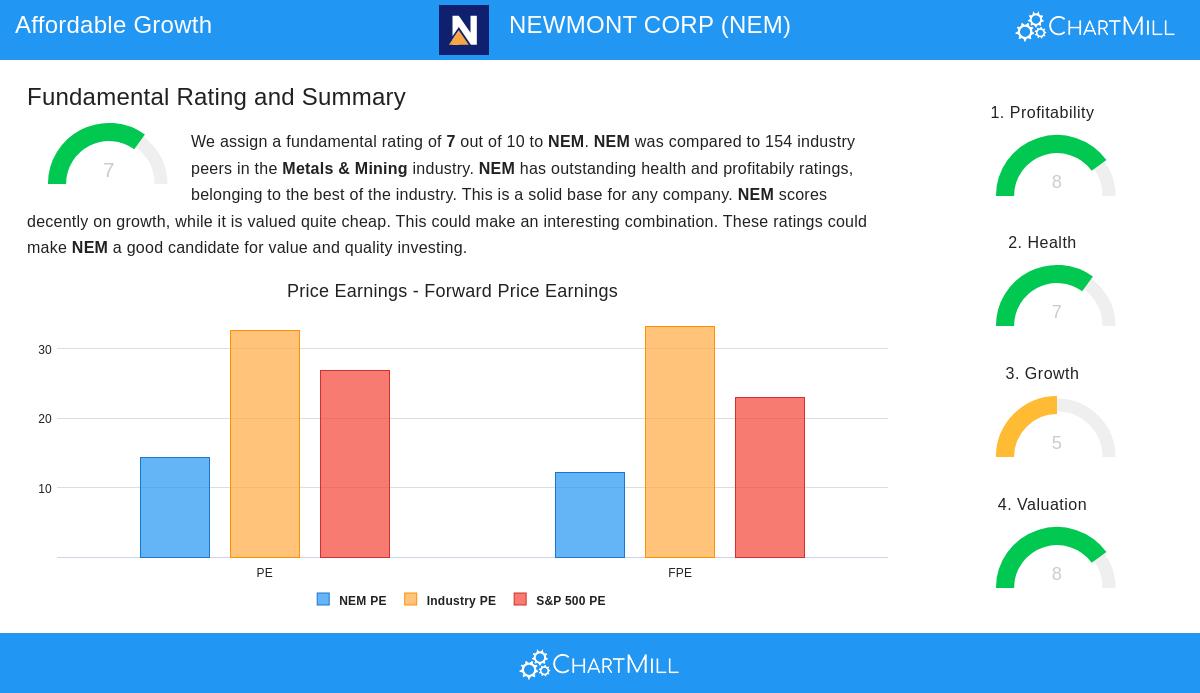

The full fundamental analysis report gives Newmont a good score of 7 out of 10, pointing out several pluses that back the Lynch system's attention to money health and profit gain. The firm grades especially high on profit measurements, with outstanding returns on assets, equity, and put-in money that do better than most others in the field. Profit differences across gross, operating, and net counts sit in the high group of the metals and mining area, though some thinning has happened lately.

From a price view, Newmont shows a notable case. While the normal P/E ratio seems fairly priced at 14.40, the firm sells at a lower cost than both field averages and the wider S&P 500 when looking at expected earnings and business value multiples. The balance sheet displays health with good cash ratios and workable debt amounts, though the payment record shows some recent drop even with a lasting payout ratio.

Growth Path Points

The firm's past growth shapes display strong speed, with EPS growing 124.42% over the last year and income rising at a 13.91% yearly rate over several years. Still, experts guess more average forward growth, with EPS likely to rise 4.43% each year and income maybe falling a bit. This split between past results and future guesses might clarify the appealing price multiples and stands as a main thought for investors using the Lynch plan.

Portfolio Match

For investors using Peter Lynch's ideas, Newmont stands for the kind of set, money-wise firm that can build the base of a long-term portfolio. The firm's worldwide mining work across many areas gives spread within the materials field, while its focus on valued metals gives contact to goods that often act unlike regular stocks. Lynch stressed knowing the businesses you put money into, and Newmont's clear mining design fits this need nicely.

Investors curious about finding more firms that meet the Peter Lynch investment rules can look at the full filtering outcomes for other possible chances.

Disclaimer: This review is based on basic facts and investment process ideas for learning uses only. It does not make up investment guidance, and investors should do their own study and talk with money helpers before making investment picks. Past results do not promise future ends, and all investments hold risk including possible loss of original money.