For investors looking for chances where the market price may not completely show a company's true condition, a systematic screening method can be a useful instrument. One method is to look for companies that join an attractive price with good basic condition, earnings, and expansion. This method tries to find possible "value with a moat", stocks that are priced well compared to their competitors or real worth, but are not low-priced for poor reasons. They are supported by good finances and positive business speed, lowering the chance of a basic value mistake. The present market setting, marked by a downward long-term direction for the S&P 500, can frequently make these price gaps, offering chances for steady investors.

Neurocrine Biosciences Inc (NASDAQ:NBIX) appears as a candidate from this kind of screening method. The biopharmaceutical company, centered on neurological and endocrine diseases, shows a picture that deserves more examination from those using a price-focused, yet quality-aware, investment plan.

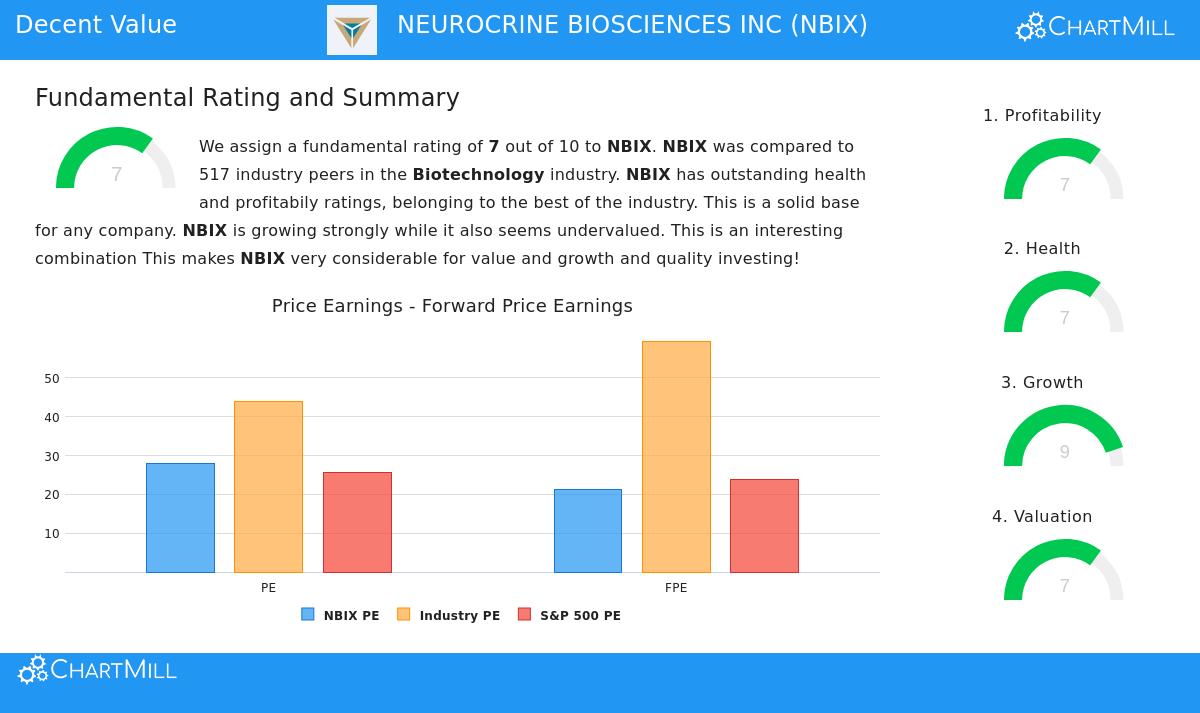

Valuation: A Relative Discount in a High-Priced Field

The central idea of value investing is buying an asset for less than its calculated real worth. For NBIX, the price measures point to a large markdown relative to its field, even if its straight P/E ratio may seem high initially.

- Field Comparison: The company's price score of 7/10 is pushed by its position compared to biotech competitors. NBIX costs less than about 93% of its field based on its Enterprise Value to EBITDA and a notable 96% based on its Price to Free Cash Flow.

- Growth-Considered Price: A central measure for expansion-focused value investors is the PEG ratio, which changes the P/E for expected earnings expansion. NBIX's low PEG ratio shows the market may not be completely counting its strong expansion path, making the present price seem "rather low".

- Setting Matters: While NBIX's P/E of 27.83 is nearly equal to the wider S&P 500 average, it differs greatly from the biotechnology field's average P/E of 43.8. This difference points out the stock's relative low price within its own high-expansion, high-multiple field.

Financial Condition: A Strong Balance Sheet

A low-priced stock is only a sound investment if the company is financially stable. A good balance sheet gives a safety buffer, making sure the business can handle economic drops and put money into future expansion without high risk. NBIX's condition score of 7/10 is held by outstanding ability to pay.

- No Debt: The company has zero owed debt. This gives a Debt/Equity ratio of 0, putting it with the top in its field and removing interest cost risk.

- Good Cash Position: With a Current Ratio of 3.39 and a Quick Ratio of 3.30, NBIX keeps enough cash to meet its short-term needs easily, giving working freedom.

- Low Failure Risk: An Altman-Z score of 7.33 shows very low short-term risk of money trouble, doing better than over 78% of field competitors.

Earnings: High Earnings and Effective Money Use

Value is not only about a low cost, it is about the grade of profits you are buying. A company with high returns on money is more likely to keep and increase its real worth over time. NBIX gets a 7/10 for earnings, showing top working skill.

- Excellent Earnings: The company has a Gross Margin of 98.18%, an Operating Margin of 22.25%, and a Profit Margin of 16.73%. Each of these measures puts NBIX in the top group of its field, doing better than over 92% of competitors.

- Better Returns: The company makes good returns on its assets and used money. Its Return on Invested Capital (ROIC) of 11.30% and Return on Equity (ROE) of 14.71% both do better than about 94% of the biotechnology field, showing very effective use of owner money.

Expansion: A Strong Force for Value Achievement

For a value idea to work, there often needs to be a reason for the market to re-price the stock. Continued expansion can be that reason, closing the space between price and seen value. NBIX's expansion score is a high 9/10.

- Notable Past Expansion: Over the last year, NBIX increased its Earnings Per Share (EPS) by 41.64% and Revenue by 21.45%. The 5-year average expansion rates are equally good at 29.09% for EPS and 22.29% for Revenue.

- Good Future Predictions: Experts think this speed will keep going, with forward EPS expansion planned at 26.83% each year and Revenue expansion at 10.12%. This steady, high-level expansion backs the view that the company's present price may not show its future profits ability.

Conclusion: An Attractive Mix of Qualities

Neurocrine Biosciences shows an attractive case for investors screening for price with quality. It is not a deep-discount, recovery story, but instead a profitable, expanding company with a clean balance sheet that is trading at a noticeable markdown to its field competitors. The mix of a low relative price, strong financial condition, top-grade earnings, and a strong expansion force fits with a method looking for low-priced companies with basic strength. This picture tries to lower the chance of a value mistake while placing for possible gain as the market sees the gap between NBIX's price and its basic business grade.

For investors wanting to look at other companies that meet similar rules of good price joined with acceptable basics, you can see the full "Decent Value" screen here.

Disclaimer: This article is for information only and does not make financial guidance, a suggestion, or an offer to buy or sell any securities. The examination is based on data and scores given by ChartMill, and investors should do their own study and talk with a qualified financial advisor before making any investment choices. Past results are not a guide for future results.