For investors looking to balance the search for growth with some caution, the Growth at a Reasonable Price (GARP) method presents a strong middle path. This method looks for companies with good and lasting earnings increases, but whose stock prices are not at the high levels often seen for aggressive growth stocks. The "Affordable Growth" screen puts this method to work by finding stocks with good growth basics, firm financial and profit strength, and a price that seems fair. This process tries to find chances where the market might not completely recognize a company's future, possibly giving a good balance of risk and reward.

Neurocrine Biosciences Inc (NASDAQ:NBIX) comes up as a pick from this screen, showing a picture that matches the affordable growth idea. The company, a biopharmaceutical business centered on neuroscience, has established a marketable group of treatments for neurological and endocrine conditions, primarily with its main product INGREZZA for tardive dyskinesia.

Notable Growth Path

The foundation of any GARP investment is, expectedly, growth. Neurocrine Biosciences does very well here, receiving a high ChartMill Growth Rating of 9 out of 10. The company’s financial results show a business in a strong period of increase.

- Past Results: Over the last year, the company's Earnings Per Share (EPS) rose by a notable 41.64%, while Revenue increased by 21.45%. The longer-term pattern is also strong, with an average yearly EPS increase of 29.09% and Revenue increase of 22.29% over recent years.

- Future Projections: This pace is forecast to keep going. Analysts predict average yearly EPS increase of 26.83% and Revenue increase of 10.12% in the next few years. This mix of solid past results and a good forward view is key for the method, as it looks for growth that is shown, not just possible.

A Price Assessment

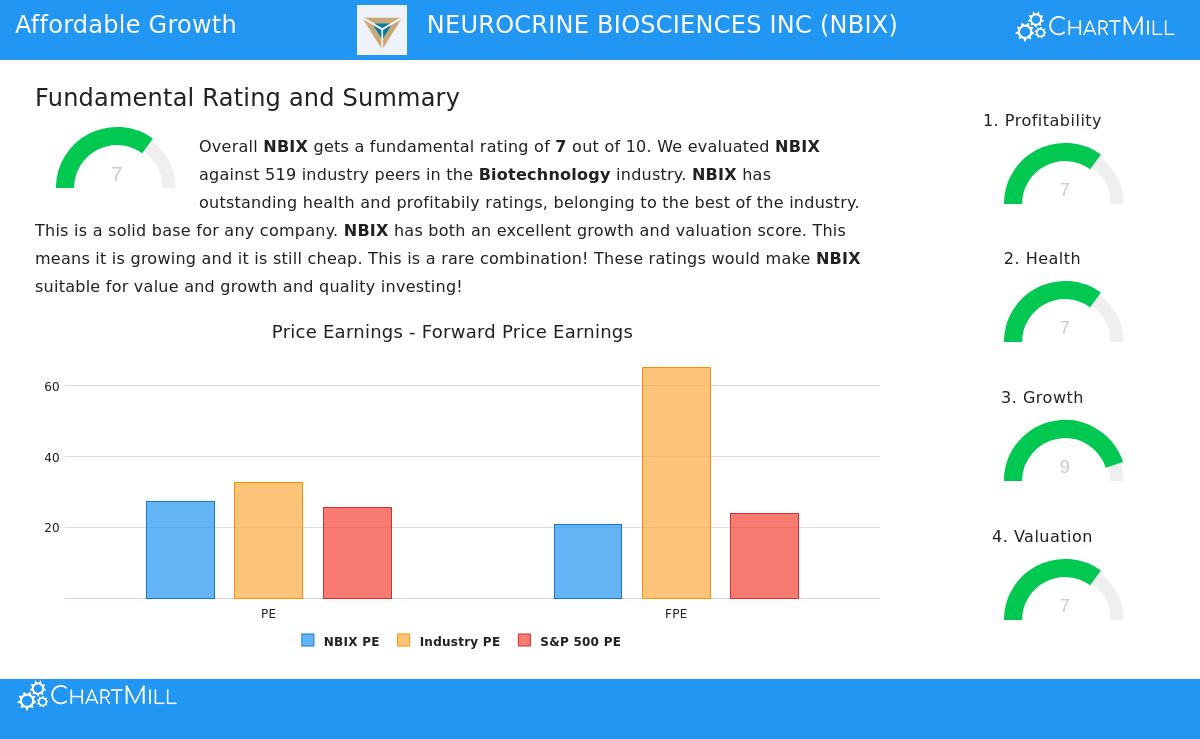

While growth is needed, paying a fair price for it is what defines the GARP method. Neurocrine gets a good Valuation Rating of 7. A closer examination shows a detailed picture where the stock seems high on some standard measures but very appealing compared to others in its field.

- Direct vs. Field Comparison: The stock's Price/Earnings (P/E) ratio of 27.42 and Forward P/E of 20.91 are similar to or a bit higher than the wider S&P 500 average. Directly, this points to a full price.

- Field Price Advantage: The strong price story comes from field comparison. Within the high-growth but often unprofitable biotechnology sector, Neurocrine is notable. Its P/E ratio is lower than 92.5% of others in its field, and its Forward P/E is lower than 94%. More significantly, its Enterprise Value to EBITDA and Price/Free Cash Flow ratios are lower than about 94% and 96% of the field, in order.

- Growth Adjustment: The low PEG ratio, which modifies the P/E for projected earnings growth, further shows the market may not be fully accounting for the company's good growth outlook. For an affordable growth investor, this relative price within a high-value field is a main draw.

Supporting Basics: Profit and Financial Soundness

Lasting growth must be supported by a steady base. The GARP method specifically looks for acceptable profit and financial soundness to steer clear of "growth pitfalls" – companies increasing sales but losing money. Neurocrine scores a 7 in both Profit and Soundness ratings, giving this important support.

- Profit Strength: The company has very good margins, with a Gross Margin over 98%, an Operating Margin of 22.25%, and a Profit Margin of 16.73%, each placed in the top group of its field. Its Return on Equity (14.71%) and Return on Invested Capital (11.30%) are also with the field's best. This shows skill in turning revenue into earnings effectively.

- Firm Financial Soundness: Neurocrine holds a very strong balance sheet with no debt, an unusual and important positive in cost-heavy biotech. This gives great room to fund research, business moves, or handle economic drops. Its high Altman-Z score (7.25) and good liquidity ratios (Current Ratio of 3.39) further highlight its financial steadiness.

Summary

Neurocrine Biosciences presents an example of the affordable growth concept. It joins fast, well-proven growth in earnings and revenue—the main force for stock price gains—with a price that, while not low on its own, is a marked difference within its own high-value field. This relative price is supported by very good profit measures and a clean, debt-free balance sheet, meeting the quality and risk-control parts built into the GARP method.

For investors, this picture indicates a company whose growth is both confirmed and likely to persist, yet is not valued at a maximum compared to similar companies. It represents the hunt for quality growth found at a fair price.

Interested in reviewing other stocks that match this Affordable Growth picture? You can use the same screen or adjust your own settings with the ChartMill stock screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The review uses data and ratings from ChartMill. Investors should do their own separate research and think about their personal money situation and risk comfort before any investment choices. Past results do not show future outcomes.