For investors looking for a dependable source of passive income, a methodical screening process is important. One useful method is to look for companies that provide a good dividend now and also have the fundamental financial soundness to maintain and possibly increase those payments in the future. This method frequently centers on stocks with high dividend scores, which assess elements such as yield, history of growth, and payment sustainability, while also needing a minimum level of acceptable profitability and financial soundness. This confirms the dividend is not temporary but is supported by a sound, well-run company.

Medtronic PLC (NYSE:MDT) is a worldwide figure in medical technology, creating and producing device-based treatments for many fields like cardiac rhythm management, spinal orthopedics, surgical instruments, and diabetes care. The company's wide array of products and fixed position in hospitals around the world are the base of its operations.

Dividend Profile: A Dependable Payer with Potential for Increase

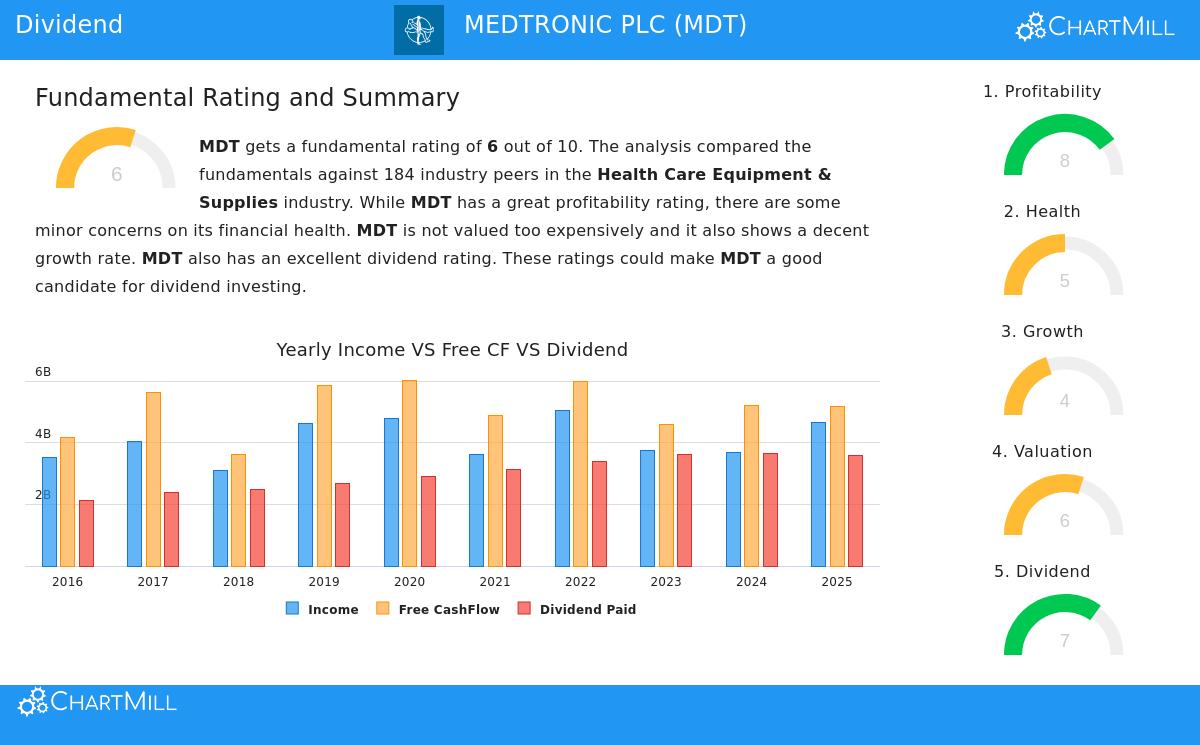

The central attraction of Medtronic for investors concentrating on income is its set dividend program. Based on ChartMill's fundamental review, the stock receives a Dividend Score of 7 out of 10, putting it in the high group of dividend-paying stocks filtered. This score rests on a few main supports:

- Good and Competitive Yield: MDT now provides a dividend yield of 3.25%. This yield is notable when measured against the wider S&P 500 average of about 1.91%. Also, it is higher than the average yield in its own Health Care Equipment & Supplies field.

- Established History of Regularity: The company has a dependable record, having paid and, importantly, kept its dividend the same or higher for at least ten straight years. This lasting practice gives investors assurance in management's focus on giving capital to shareholders.

- Maintainable Increase Path: MDT has raised its dividend at a yearly rate of around 5.1% over the last five years. This increase is seen as maintainable by experts because the company's profits are expected to rise more quickly. This link between dividend increase and profit increase is a key test for making sure future raises are not paid for by too much debt or weakening the financial position.

A note of care in the review is the present payout ratio, which is close to 79% of net income. This is higher than the level usually seen as cautious, but the situation of the company's good profitability and positive future profit forecasts indicates the dividend is still workable.

Fundamental Soundness: Profitability and Financial Condition

A high dividend is only as solid as the company behind it. This is why the filtering rules call for acceptable scores in profitability and financial condition, to steer clear of situations where a high yield indicates trouble instead of chance. Medtronic does acceptably on these basic measures.

Profitability Score: 8/10 The company gets a strong Profitability Score of 8. Its margins are a specific positive:

- An operating margin of almost 19% puts it in the top group of its field.

- A profit margin of 13% and a good gross margin over 65% also show efficient operations and pricing ability. While some profit ratios have faced difficulty in recent years, the central business is still very profitable, creating ample cash to meet its duties and pay for its dividend.

Financial Condition Score: 5/10 The Condition Score of 5 shows an acceptable, but not outstanding, financial state. The review presents a varied image:

- Liquidity is acceptable: With a current ratio of 2.54 and a quick ratio of 1.87, Medtronic has enough short-term assets to cover its short-term debts, showing no immediate liquidity worries.

- Solvency measures indicate some use of debt: The company has a moderate amount of debt, with a Debt/Equity ratio of 0.57. This is workable but shows some use of debt for funding. The good point is that its Debt-to-Free-Cash-Flow ratio is more favorable than many field competitors, meaning its operational cash creation is enough to handle its debt over time.

Valuation and Increase Setting

From a valuation view, Medtronic seems fairly valued. Its Price-to-Earnings ratio of 15.6 and Forward P/E of 14.2 are seen as reasonable and are lower than both the wider S&P 500 and the average for its own field. This suggests the market is not valuing its profits or dividend stream too highly.

Increase is expected to be stable, not fast. Sales and profits are forecast to rise in the mid-single-digit percentage range each year. For a dividend investor, this modest, predictable increase pattern can be better, as it often comes from a steady, established business less likely to the changes that can risk dividend payments.

Is Medtronic Suitable for a Dividend Portfolio?

Medtronic PLC makes a notable case for investors using a quality dividend method. It joins a better-than-average and increasing yield with the signs of a lasting business: good profitability, a long record of dependable payments, and acceptable financial condition. The company works in the stable healthcare field, which can give steadiness during economic declines. While the higher payout ratio and moderate debt level need watching, they are weighed against the firm's very good cash creation ability and field-leading margins.

For investors who value regular income from companies with strong positions and global size, MDT deserves more study. Its profile matches the aim of making a portfolio of dividend payers that can provide income through different market periods.

Want to see other stocks that meet similar quality dividend filters? You can look at the complete list of options by going to the Best Dividend Stocks screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. All investments have risk, including the possible loss of the amount invested. Investors should do their own study and talk with a registered financial advisor before making any investment choices. The review is based on given data and shows conditions at the time of writing, which can change.