Investors looking to balance the search for growth with a degree of caution often consider strategies like Growth at a Reasonable Price (GARP). This method tries to find companies with solid and lasting earnings increase, but whose shares are not priced too high. It is a middle path between pure, often costly, growth investing and deep-value investments, concentrating on good businesses the market may not yet fully value for future possibility. One way to search for such chances is to use fundamental ratings that assess a stock on a few main areas: growth, valuation, profitability, and financial soundness.

McKesson Corp (NYSE:MCK) is a major company in healthcare supply chain management and medical-surgical distribution, offering necessary services in the U.S. and other countries. The company's fundamental picture, as shown in a detailed analysis report, indicates it may meet the affordable growth requirements, deserving more attention from investors using this method.

Solid Growth Path

The central idea of any growth-oriented strategy is, expectedly, growth. McKesson shows firm performance here, receiving a ChartMill Growth Rating of 7 out of 10. The company is not only posting notable historical results but is also projected to keep a sound speed going forward.

- Earnings Increase: McKesson has shown strong earnings per share (EPS) growth, with a 28.88% rise over the past year and a 17.17% average yearly growth rate over recent years.

- Revenue Progress: Top-line growth is also firm, with revenue rising 15.49% in the last year and increasing at an average yearly rate of 9.22%.

- Future Projection: Analyst forecasts support the extension of this pattern, with predicted average yearly EPS growth of 14.08% and revenue growth of 8.44% in the next years.

This steady and solid growth in both earnings and revenue is exactly what GARP investors look for, as it points to a business that is effectively growing and taking market chances.

Fair Valuation Measures

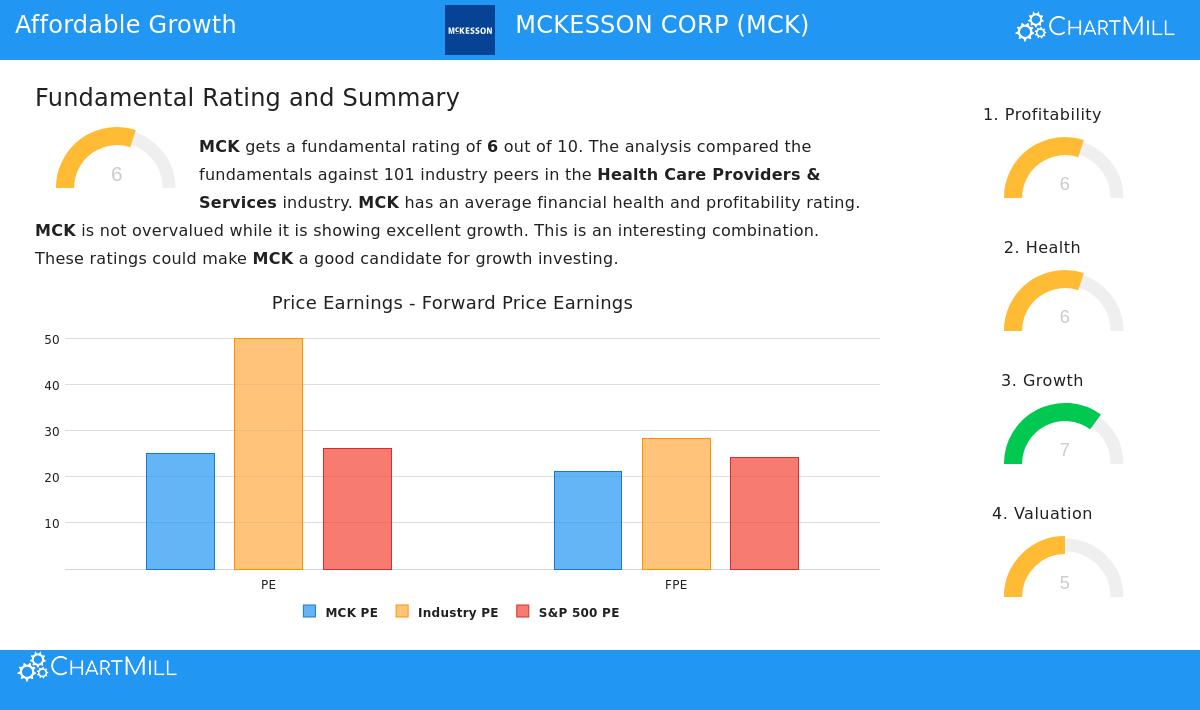

While growth is necessary, paying an unfair price for it can cancel future gains. The affordable growth strategy stresses finding stocks where the price does not completely account for the growth outlook. McKesson’s ChartMill Valuation Rating of 5 implies it is valued similarly to its wider market and industry, giving a fair entry point considering its growth picture.

- P/E Ratios: With a trailing P/E ratio of 25.06, McKesson trades a bit under the current S&P 500 average. Its forward P/E of 21.07 is also similar to the wider market.

- Industry Comparison: More significantly, when measured against its peers in the Health Care Providers & Services industry, which often has higher average multiples, McKesson seems somewhat more fairly priced.

- Growth Consideration: The PEG ratio, which includes earnings growth, shows the stock is priced fairly. This equilibrium is important; the valuation is not so cheap as to point to basic issues, nor so expensive as to require perfect performance for years ahead.

For the affordable growth process, this valuation setting is vital. It implies the market has not yet extended McKesson's solid growth rates into an overly hopeful stock price, leaving possible space for gain as the company carries out its plans.

Supporting Basics: Profitability and Soundness

A growth narrative based on weak finances is a hazardous idea. The affordable growth filter used to find McKesson also needed acceptable scores in profitability and financial soundness, which serve as important checks for durability.

Profitability (Rating: 6): McKesson’s profitability is supported by a very good Return on Invested Capital (ROIC) of 28.37%, doing better than almost all its industry peers. This shows very effective use of capital to produce profits. However, the company works on famously small margins typical in the distribution field, with a gross margin of 3.48% and a profit margin just over 1%. While these margin levels are a feature of its business model, the high ROIC proves that McKesson performs well within that structure.

Financial Soundness (Rating: 6): The company’s health score shows a varied image. On the good side, McKesson has a very solid solvency position. Its Altman-Z score shows no bankruptcy danger, and its debt-to-free-cash-flow ratio of 0.68 is very good, meaning it could in theory pay off all debt in under a year from its cash flow. The company has also been decreasing its share count and lowering its debt-to-assets ratio. A note of attention is liquidity, with current and quick ratios under 1.0, which is not unusual for large distributors with efficient cash conversion cycles but is a measure investors should watch.

These supporting ratings are why the stock met the "acceptable profitability and health" filter. They verify that the growth is not being reached through careless borrowing or by sacrificing returns, giving a steadier base for the investment argument.

Summary and Additional Study

McKesson Corp offers a noteworthy case for investors filtering for affordable growth. The company displays a clear and solid growth path in both revenue and earnings, which is the main driver for possible stock gain. This growth is available at a price that is fair compared to both the wider market and its own industry, sidestepping the extreme high prices often linked to high-growth stocks. While its thin margins and lower liquidity ratios are acknowledged, they are offset by better capital efficiency and a very solid overall solvency position.

For investors curious about examining other companies that meet similar standards of good growth, fair valuation, and acceptable basic finances, more outcomes can be located using the Affordable Growth stock screener.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on supplied data and should not be the only foundation for any investment choice. Investors should do their own complete study and talk with a qualified financial advisor before making any investment decisions.