The investment philosophy of Peter Lynch, the famous manager of Fidelity's Magellan Fund, focuses on locating well-run, expanding companies available at sensible prices, a strategy often called Growth at a Reasonable Price (GARP). Lynch supported putting money into businesses you comprehend, with lasting expansion, sound financial condition, and appealing prices. His method applies particular quantitative filters to find these opportunities, concentrating on earnings expansion, profit generation, balance sheet soundness, and an important pricing measure that considers that expansion.

Logitech International SA (NASDAQ:LOGI) is a known name to many customers and professionals, making accessories like mice, keyboards, webcams, and headsets. This fits with Lynch's idea of investing in what you know. The company's goods are central to personal computing, gaming, and the hybrid work setting. A recent filter built on Lynch's main standards pointed out Logitech as a stock deserving more examination from long-term GARP investors.

Fitting the Lynch Standards

The filter uses several rules taken from Lynch's strategy. This is how Logitech measures up against these important rules:

- Lasting Earnings Expansion: Lynch looked for companies with steady expansion, but cautioned against very fast growth that could not continue. The filter demands a 5-year earnings per share (EPS) expansion rate between 15% and 30%. Logitech's EPS has expanded at an average yearly rate of 17.67% over this time, easily inside this goal range and pointing to a stable, lasting path.

- Sensible Pricing (PEG Ratio): Maybe the central part of Lynch's pricing method is the Price/Earnings to Growth (PEG) ratio, which compares a stock's P/E ratio to its expansion rate. A PEG ratio of 1 or less shows the stock may be sensibly priced compared to its expansion. Logitech's PEG ratio, based on its last five-year expansion, is 0.93, meeting this important standard and indicating possible value.

- High Profit Generation (Return on Equity): Lynch preferred companies that produce high returns on shareholder equity. The filter requires a Return on Equity (ROE) above 15%. Logitech greatly passes this with an ROE of 30.47%, showing very effective use of investor money.

- Financial Condition (Debt & Liquidity): A careful balance sheet was crucial for Lynch. The strategy selects for a Debt-to-Equity ratio below 0.6 and a Current Ratio above 1. Logitech does very well here, having a Debt-to-Equity ratio of 0.0, meaning it functions with no net debt, and a Current Ratio of 2.21, showing sufficient liquidity to meet short-term needs.

Fundamental Condition Review

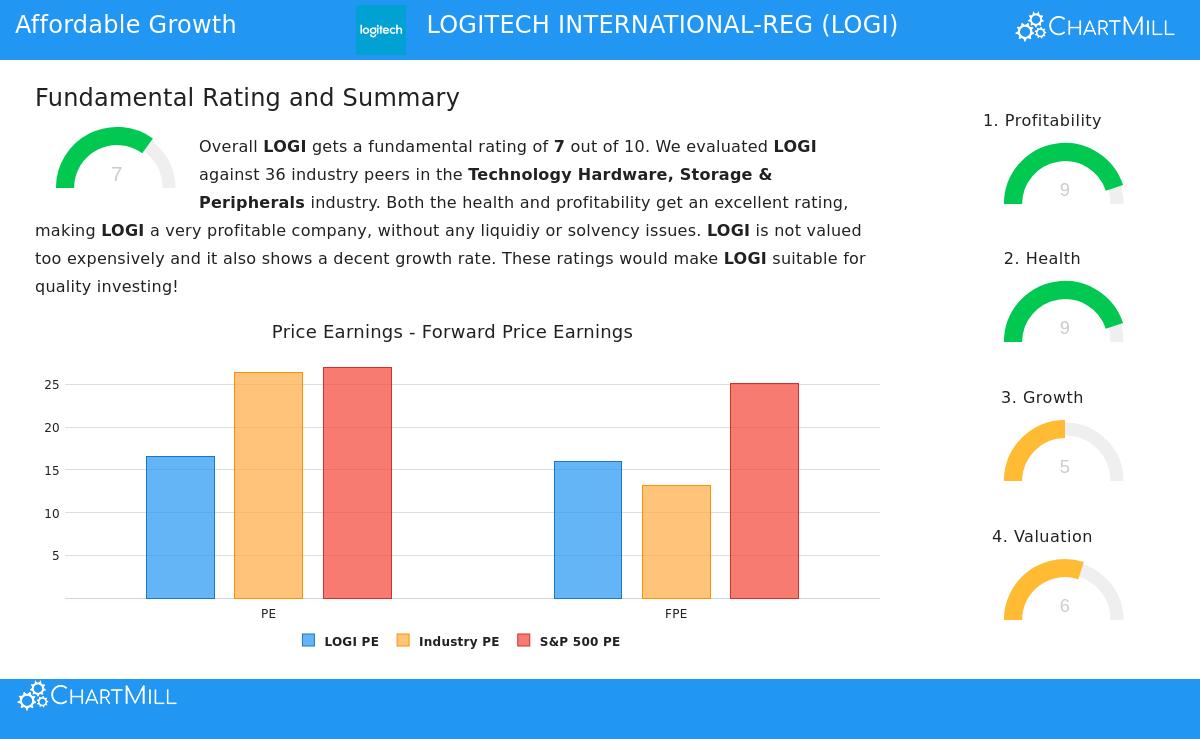

Outside the specific filter settings, a wider fundamental review of Logitech supports its position as a GARP candidate. The company gets a sound overall fundamental score of 7 out of 10. Its most persuasive strong points are in outstanding financial condition and high profit generation. The company's stability is first-rate, backed by its debt-free position and excellent Altman-Z score. Profit generation measures like Return on Assets (17.38%) and Return on Invested Capital (22.38%) also place in the high level of its industry.

Pricing seems reasonable. While the P/E ratio of 16.52 is viewed as "fair," it is less expensive than over 80% of its industry competitors and the wider S&P 500. The primary area of average performance is expansion; while past results have been sound, analysts predict a slowdown in both sales and earnings expansion moving ahead. This is a point for investors to watch, though the predicted expansion rates stay positive.

You can examine the full fundamental details for Logitech here.

Investment Points

For an investor following Peter Lynch's philosophy, Logitech offers a persuasive outline. It functions in a comprehensible business, shows the financial control Lynch respected with no debt and sound cash production, and has a record of profitable expansion at a lasting speed. The current pricing, as shown by the below-1 PEG ratio, suggests the market may not be completely acknowledging this quality and expansion mix.

Still, Lynch would also recommend examining non-quantitative points. Investors should think about the company's competitive place in an active hardware market, its new product development, and how it handles possible cyclical demand. The expected expansion slowdown noted in the fundamental report needs focus to make sure the company's "story" stays unchanged.

Locating Comparable Opportunities

Logitech is one of the companies that passed a filter designed on Peter Lynch's strategy. Investors curious about finding other stocks that fit these standards for lasting expansion, financial soundness, and sensible pricing can run the filter themselves. You can locate the Peter Lynch strategy filter and see all present outcomes here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.