For investors aiming to construct a durable, long-term portfolio, the ideas of quality investing present a useful framework. This method concentrates on finding companies with lasting competitive strengths, sound financial condition, and the capacity to produce high returns on capital reliably over many years. Instead of searching for the lowest prices, quality investors accept paying a reasonable price for outstanding businesses they can hold for a long time. One organized way to find these companies is through a strict screening process, such as the "Caviar Cruise" screen, which selects for solid revenue and profit expansion, high returns on invested capital, good cash flow conversion, and reasonable debt.

A recent search using this process has identified Laureate Education Inc (NASDAQ:LAUR), a supplier of higher education services in Mexico and Peru. The company's financial picture seems to match the central beliefs of quality investing, justifying further examination from investors concentrated on lasting business models.

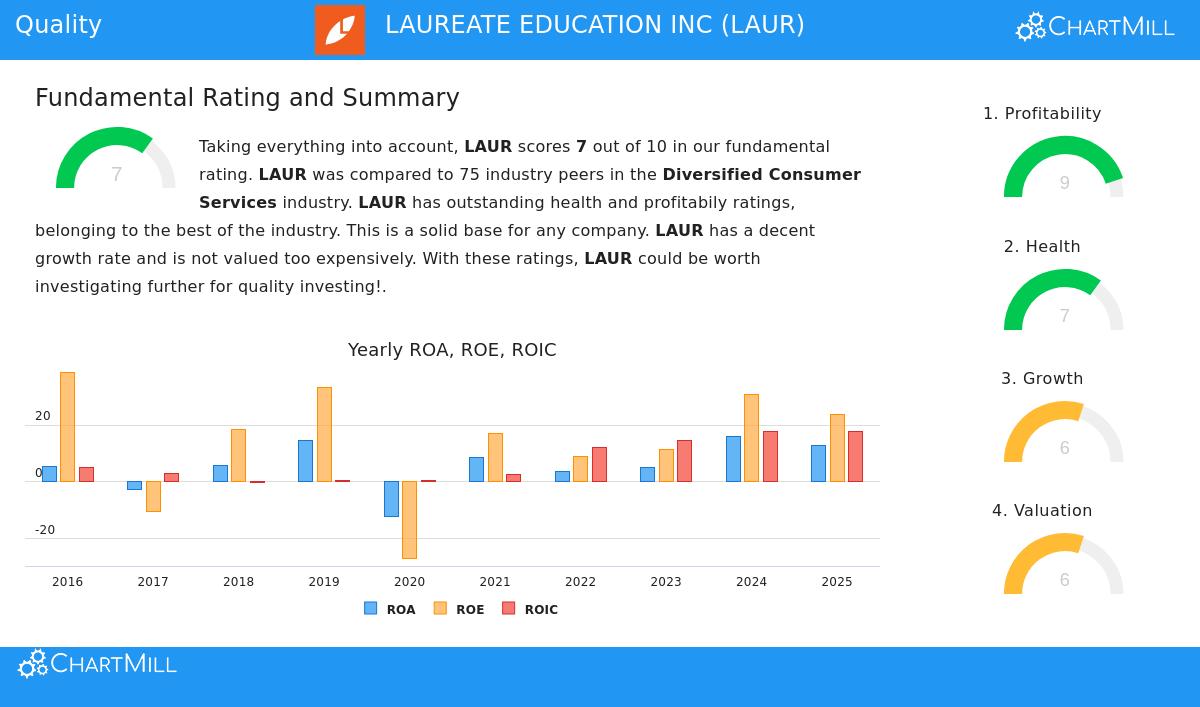

Passing the Main Quality Tests

The Caviar Cruise screen uses several measurable tests to find high-grade candidates. Laureate Education's fundamentals indicate it meets these important checks with clear force.

- High Profitability and Capital Use: A central part of quality investing is a high return on invested capital (ROIC), which shows how well a company uses its money to create profits. Laureate's ROIC excluding cash, goodwill, and intangibles is a notable 39.1%, well above the screen's 15% requirement. This indicates the company's main activities are very good at building shareholder value.

- Strong Cash Flow Production: Good companies convert accounting profits into actual cash. This is calculated by Profit Quality, or the ratio of free cash flow to net income. Laureate's five-year average here is 110.1%, exceeding the 75% filter. This means the company produces more cash than its stated net income, offering important financial room for dividends, share repurchases, debt payment, or new investment.

- A Very Strong Balance Sheet: Careful debt management is important for long-term strength. The screen checks this by comparing total debt to free cash flow. Laureate's ratio of 0.48 is very good, showing it could pay off all its debt in under half a year using its present cash flow. This low debt level offers a wide safety buffer.

- Good Historical Profit Expansion: While 5-year revenue expansion data was not available in the given parameters, the company shows forceful growth in earnings. Its 5-year CAGR for EBIT (Earnings Before Interest and Taxes) is a strong 80.2%. Also, the screen demands that EBIT growth is faster than revenue growth, a signal of getting better operational efficiency and possible pricing strength. The given data shows Laureate has done this, pointing to a path of not only expanding, but also becoming more profitable as it gets larger.

A Broad Fundamental Picture

An examination of Laureate Education's wider fundamental analysis report supports the image shown by the screen. The company gets an overall fundamental score of 7 out of 10, with specific high points in profitability and financial condition.

Its profitability score of 9/10 is fueled by sector-leading margins and returns. The operating margin of 25.3% and ROIC of 17.7% each do better than over 90% of similar companies in the Diversified Consumer Services industry. Financially, the company's stability is sound, with a very low debt-to-equity ratio and an Altman-Z score that shows no bankruptcy danger. The primary area to note is a lower liquidity ratio (current and quick ratios), which the report explains by saying that given the company's very good stability and profitability, this may not signal a basic problem but should be considered within the details of its specific business activities.

On valuation, the stock does not seem too expensive. Its P/E and forward P/E ratios are lower than the wider S&P 500 and a majority of its industry peers. For growth, analysts expect consistent forward revenue and EPS growth in the high single-digits to low teens, indicating the company's growth story is still current.

Is Laureate Education a Quality Stock?

Judging by the measurable filters of the Caviar Cruise screen, Laureate Education makes a solid argument. It displays the signs quality investors look for: high returns on capital, excellent conversion of profits to cash, a very strong balance sheet, and a record of quickly growing earnings. These numbers indicate a business with an efficient operating model and important financial might.

The company's concentration on private higher education in developing Latin American markets like Mexico and Peru fits with the non-numerical points of quality investing, like gaining from a long-term direction (rising need for education) and working in a clear business area. While careful research on competitive forces, regulatory settings, and management performance is still needed, the first measurable picture is persuasive.

For investors wanting to investigate other companies that meet similar strict quality filters, the Caviar Cruise screen can be found here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.