Investors aiming to assemble a collection of lasting, high-quality companies at fair prices frequently consider the ideas of famed fund manager Peter Lynch. His approach, outlined in One Up on Wall Street, centers on finding firms with good, maintainable growth, sound financial condition, and appealing prices, a philosophy often called Growth at a Reasonable Price (GARP). The central thought is to locate companies that are increasing reliably but are not excessively promoted or priced, permitting the long-term accumulation of returns. A filter using Lynch's main measures recently pointed to Kinross Gold Corp (NYSE:KGC) as a possible option deserving more study.

Using the Lynch Method

Peter Lynch’s approach steers clear of speculative, high-priced growth stocks for companies with a history of controlled increase. He stressed basic condition tests to confirm a business could endure economic shifts. The filter used a number of his standard checks, and Kinross Gold seems to satisfy these numerical standards.

- Maintainable Earnings Growth: Lynch wanted companies with a 5-year earnings per share (EPS) increase between 15% and 30%, quick enough to be interesting but gradual enough to be maintained. Kinross Gold states a 5-year EPS increase rate of 19.2%, putting it directly within this preferred band.

- Fair Pricing (PEG Ratio): To prevent paying too much for growth, Lynch employed the Price/Earnings to Growth (PEG) ratio, choosing a value of 1 or lower. Kinross Gold’s PEG ratio, calculated from its last 5-year increase, is 0.92, hinting the market may not be completely valuing its past earnings growth.

- Sound Financial Condition: A careful balance sheet was essential for Lynch. The filter demanded a Debt/Equity ratio under 0.6 and a Current Ratio over 1. Kinross does very well here, with a Debt/Equity ratio of 0.16, much lower than Lynch’s own more cautious limit of 0.25, and a solid Current Ratio of 2.84, indicating sufficient cash to meet near-term needs.

- High Profit Generation (Return on Equity): Lynch searched for companies that effectively produce profits from shareholder equity, establishing a high standard with an ROE above 15%. Kinross Gold’s ROE of 31.6% greatly passes this mark, implying management is very good at using capital.

Examining the Basics More Closely

A wider basic examination of Kinross Gold supports the image shown by the Lynch filter. The company gets a good total score, with specific high points in profit generation and financial condition.

The profit generation picture is very good, with sector-best margins and returns. The company’s Return on Invested Capital (ROIC) of 21.75% is much higher than its cost of capital, meaning it is producing real economic value with each dollar used. This matches Lynch’s interest in companies that are not only increasing, but increasing profitably and effectively.

From a financial condition view, the balance sheet is a key trait. The extremely low debt amount, paired with good free cash flow, provides the company notable financial room and stability. Importantly, Kinross has been lowering its share count over time, a trait Lynch liked as it can improve per-share value for continuing shareholders.

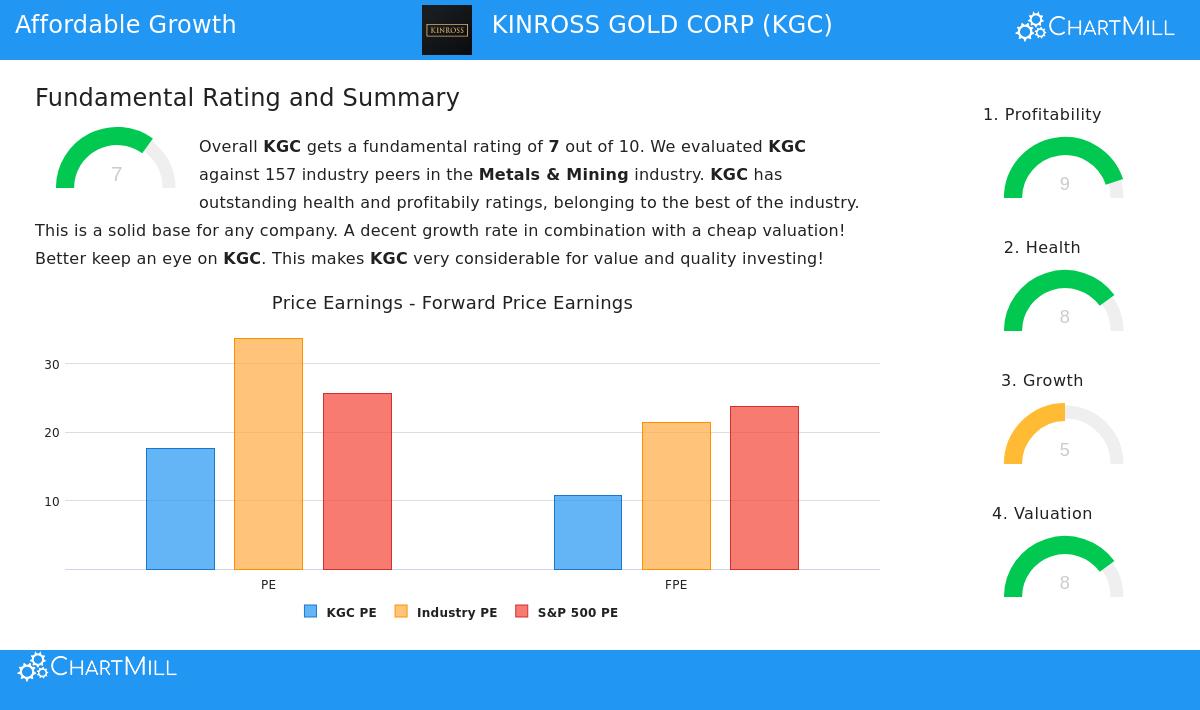

On pricing, the image is varied but tends positive. While the standard P/E ratio seems high alone, it turns appealing when measured against sector competitors and when growth is included through the PEG ratio. Measures like Price/Free Cash Flow and Enterprise Value/EBITDA also propose the stock is valued low compared to the wider mining sector.

The primary point of care exists in future increase forecasts. Analysts predict a short-term decrease in revenue and earnings increase, a typical factor for cyclical commodity companies. This highlights the Lynch idea that filtering is only the initial stage; investors must then study the business cycle, commodity forecast, and company-specific plans to decide if present operational health can continue. You can see the full basic examination report here.

Is Kinross Gold a Lynch-Method Investment?

For investors following the GARP philosophy, Kinross Gold offers an interesting example. It meets the first Lynch filter by showing a record of reliable earnings increase, trading at a fair price when that growth is considered, and working from a very strong balance sheet with high profit generation. These are exactly the features Lynch thought could result in good long-term investments, as they lower risk while keeping contact with accumulating returns.

However, the Lynch way needs looking past the figures. The next, vital stage is non-numerical study: knowing the gold mining sector’s patterns, judging the duration and expenses of Kinross’s main mining plans, and reviewing management’s capital use choices. The company’s attention on operational effectiveness and its set of development plans, like the Great Bear asset in Canada, would be key to this examination.

For investors wanting to review other companies that presently meet this strict investment filter, you can locate the complete, current list of outcomes using the Peter Lynch Strategy stock screener.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any security. The examination uses publicly accessible information and a particular investment strategy filter. Investors should do their own complete study and think about their personal financial situation and risk comfort before making any investment choices. Past results do not guarantee future outcomes.