In the search for investment opportunities, many strategies exist, but few have the enduring legacy of value investing. At its center, this philosophy, supported by figures like Benjamin Graham and Warren Buffett, involves finding companies trading for less than their intrinsic worth. The goal is to buy these undervalued assets and hold them until the market corrects its pricing, a process that needs patience and a focus on fundamental business health. A disciplined method for this strategy often involves screening for stocks that are not only inexpensive on common valuation measures, but also show good underlying financial strength, steady profitability, and acceptable growth prospects. This mix helps investors avoid the dreaded "value trap", a stock that is inexpensive for a reason, often because of worsening fundamentals.

One company that recently appeared through such a disciplined screening process is JONES LANG LASALLE INC (NYSE:JLL), a global leader in commercial real estate and investment management services. By using filters that select for a good valuation rating along with acceptable scores in profitability, financial health, and growth, JLL presents an interesting case for more review by value-oriented investors.

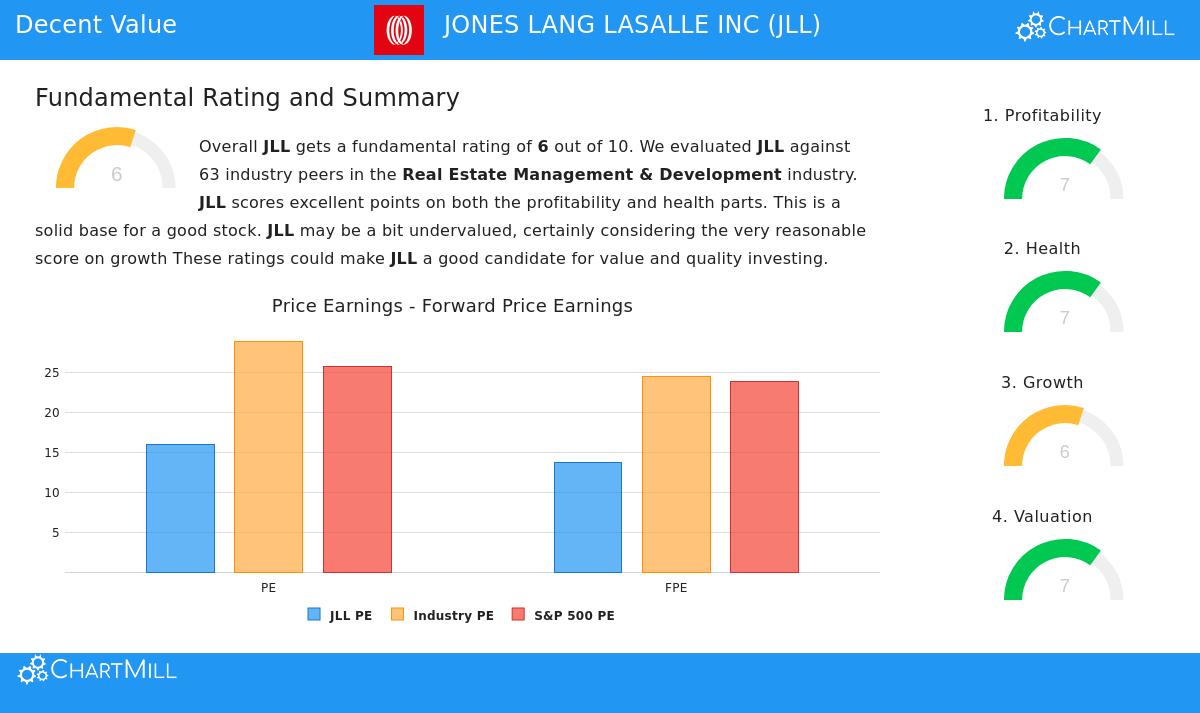

Valuation: The Center of Opportunity

The main attraction for any value investor is an appealing price relative to a company's earnings and assets. JLL’s valuation measures indicate the market may be pricing the company cautiously. According to ChartMill's fundamental analysis report, the stock gets a Valuation Rating of 7 out of 10, showing it is placed well within its industry.

- Price-to-Earnings (P/E) Ratio: At 15.90, JLL’s P/E ratio is much lower than the wider S&P 500 average of 25.71. More significantly, it is lower than about 81% of its peers in the Real Estate Management & Development industry.

- Forward P/E Ratio: The view stays attractive looking forward, with a forward P/E of 13.65. This is also a discount to the S&P 500 and places JLL as less expensive than over 90% of its industry competitors.

- Enterprise Value to EBITDA & Price/Free Cash Flow: Other important valuation multiples back this idea. The company’s Enterprise Value/EBITDA and Price/Free Cash Flow ratios are lower than about 84% and 81% of the industry, in that order.

For a value strategy, these measures are important. They give the initial "margin of safety", the buffer between the price paid and the estimated intrinsic value, that guards investors from mistakes in judgment or unexpected market declines. JLL’s ratings across these standards indicate such a buffer may be present now.

Financial Health: A Base of Stability

An inexpensive stock is only a good investment if the company is financially stable. A strong balance sheet makes sure a business can endure economic cycles, put money into growth, and prevent solvency problems. JLL gets a good Health Rating of 7, showing a sound financial position.

- Solvency Strength: The company shows very good solvency measures. Its Debt-to-Free Cash Flow ratio of 1.69 is notable, showing it could pay off all its debt in under two years using its current cash flow. This ratio is better than 84% of the industry. Also, a good Debt-to-Equity ratio of 0.22 and a positive Altman-Z score of 3.11 point to a low chance of financial trouble.

- Share Count Management: On a positive note, JLL has lowered its number of shares outstanding over the past one and five years, an action that benefits shareholders and can raise earnings per share over time.

This financial strength is essential for a long-term value holding. It matches the idea of investing in businesses, not just stock symbols, and makes sure the company has the staying power needed for the market to see its full value.

Profitability: The Driver of Intrinsic Value

Value investing is not about buying broken companies; it is about buying profitable ones at a discount. A company's ability to produce returns on its capital is a direct source of its intrinsic worth. JLL gets a Profitability Rating of 7, proving it is a fundamentally profitable firm.

- Good Returns on Capital: The company shows effective use of its assets and equity. Its Return on Invested Capital (ROIC) of 8.39% puts it in the top group of its industry, doing better than 95% of peers. In the same way, its Return on Equity (ROE) of 10.56% is higher than 90% of the industry.

- Getting Better Margins: It is worth noting that JLL’s Profit Margin has gotten better lately and, at 3.03%, is above the industry median. Its Operating Margin of 4.49% is also in the better half of the sector.

These measures are important because they confirm the business is operationally sound. A value investor looks for a gap between price and value, and maintained profitability is a key part in figuring that underlying value. JLL’s ratings indicate it has the operational engine to support a higher valuation over time.

Growth: The Reason for Re-rating

While pure value stocks can sometimes be still, the most interesting opportunities often include a growth part that can act as a reason for the market to re-price the stock. JLL’s Growth Rating of 6 shows a sensible and stable growth path.

- Good Historical Performance: Over the past year, the company has given strong growth, with Earnings Per Share (EPS) increasing by 34.62% and Revenue growing by 11.45%. The longer-term averages are also good, with EPS growing at almost 15% each year over recent years.

- Positive Future Expectations: Analysts think this momentum will keep going, predicting yearly EPS growth of over 14% in the coming years. While revenue growth is expected to slow, it stays positive.

For the value strategy, this growth part is significant as it can speed up the coming together of market price with intrinsic value. It gives a fundamental reason for the stock’s multiple to increase, offering the chance for a "double benefit", earnings growth combined with a higher valuation multiple.

Conclusion and Further Research

JONES LANG LASALLE INC shows a profile that matches several key ideas of value investing: it seems fairly priced relative to its industry and the market, it works from a position of financial strength, it creates good profits on its capital, and it is joined with a respectable growth view. This mix tries to meet the value investor's search for a margin of safety while avoiding the problems of a still or weakening business.

It is important to note that any screen is a beginning point for more careful examination. Investors should think about the cyclical character of the commercial real estate sector, macroeconomic interest rate risks, and the company’s competitive environment.

For investors interested in looking at similar opportunities found by this "Decent Value" method, you can see the full screening rules and view other possible choices by going to the pre-configured stock screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data and ratings provided by ChartMill. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.