For investors aiming to assemble a portfolio of lasting, high-grade businesses, the quality investing philosophy offers a strong framework. This method concentrates on finding companies with durable competitive strengths, skilled leadership, reliable earnings, and sound financial condition, firms an investor would be at ease holding for decades. The "Caviar Cruise" stock screener is built to methodically filter for these characteristics, using measurable standards like solid revenue and profit expansion, high returns on invested capital, good free cash flow production, and reasonable debt. A company that meets this strict filter justifies more attention from investors focused on quality.

One company that presently appears from this quality-oriented filter is Huron Consulting Group Inc (NASDAQ:HURN), a supplier of technology, data, and analytics solutions to the healthcare, education, and commercial industries. The company’s financial statement matches several main supports of the quality investing plan.

Match with Quality Investing Standards

The Caviar Cruise system stresses not only expansion, but profitable and efficient expansion. It looks for companies where profit growth exceeds sales growth, signaling better operational efficiency and pricing ability. Also, a high return on invested capital (ROIC) is critical, as it reveals management’s ability to use capital to create earnings.

Huron Consulting shows good results in these central areas:

- Profit Growth Exceeding Sales: While the given 5-year sales CAGR data is not present, the company's 5-year EBIT (Earnings Before Interest and Taxes) compound annual growth rate is a notable 31.6%. This concentration on EBIT growth, a gauge of core operational earnings, is key to the quality filter as it removes financial and tax setups, permitting a clearer evaluation of business results.

- Notable Return on Capital: A prominent measure for HURN is its Return on Invested Capital (leaving out cash, goodwill, and intangibles), which is at a striking 56.5%. This is much higher than the filter’s limit of 15% and shows that Huron produces significant profit from the capital it has put into its business. For a quality investor, a high and maintainable ROIC is a clear sign of a lasting competitive edge and good capital use.

- Good Cash Flow and Reasonable Debt: Quality companies convert accounting earnings into actual cash. HURN’s 5-year average Profit Quality—which calculates free cash flow as a portion of net income—is 108.7%, passing the filter’s 75% goal. This means the company reliably produces more cash than its stated net income, offering financial room. This cash production backs a sound balance sheet, shown by a Debt-to-Free Cash Flow ratio of 3.14, comfortably inside the filter’s acceptable limit of below 5. This ratio implies Huron could in theory settle all its debt with slightly more than three years of current free cash flow, indicating limited financial danger.

Fundamental Condition and Expansion Outline

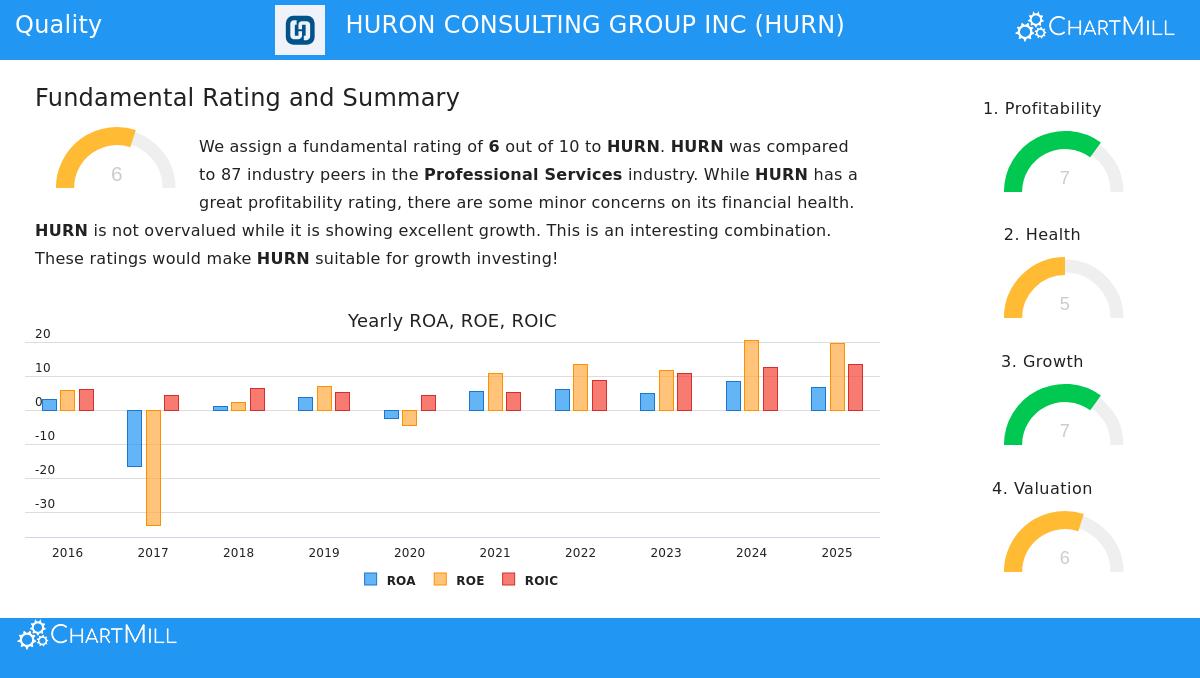

An examination of Huron’s wider fundamental analysis report supports its quality features. The report gives HURN a total score of 6 out of 10, stating it is "suitable for growth investing." The examination points out a solid profitability outline (score of 7) fueled by good returns on assets, equity, and invested capital that beat most of its Professional Services industry competitors. Margins are sound and have displayed progress.

The expansion story is strong, with a growth score of 7. The company has shown good historical expansion in both earnings per share (29.4% yearly growth over 5 years) and sales, and experts forecast ongoing double-digit expansion in the coming years. While the financial condition score (5) mentions some small points about liquidity ratios versus competitors, the company’s ability to meet obligations remains firm, supported by an acceptable Altman-Z score and the reasonable debt load noted before.

From a price standpoint, the report indicates HURN is priced neutrally to somewhat lower than both its industry and the wider market, exchanging at a P/E ratio of 16.2. For a quality investor, paying a fair—not greatly reduced—price for a better business is frequently an agreeable exchange.

Investment Points

While the numerical filter shows an appealing image, quality investing also requires evaluating non-numerical aspects. Huron’s focus on essential consulting in areas like healthcare and education, which encounter ongoing regulatory and technological change, implies a stable demand source. The company’s approach, using deep knowledge and data analytics, can build competitive barriers. Still, investors should think about the natural variability of consulting services and the company’s dependence on important staff to produce its project-based sales.

For investors wanting to examine other companies that meet the Caviar Cruise quality filter, you can see the complete list of findings here.

In conclusion, Huron Consulting Group makes a strong argument for quality investors grounded in its numerical profile. Its notable returns on capital, effective cash conversion, careful debt handling, and history of profitable expansion fit well with the standards made to find lasting, well-managed businesses. As with all investments, this filter-based finding should act as the beginning for more detailed investigation. A full review of Huron’s complete fundamental analysis, competitive situation, and long-term industry directions is necessary before any investment choice.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.