For investors looking for chances where a company's market price may not completely show its basic business condition, a systematic value method can be a helpful beginning. One frequent tactic involves filtering for companies that seem basically priced low by the market while still showing firm operational condition and earnings. The reasoning is simple: find businesses selling for less than their calculated worth, but steer clear of possible "value traps" by confirming they have the financial strength and profit ability to last and expand. This technique mixes the bargain-seeking part of value investing with a needed emphasis on quality, searching for stocks that are not only low-priced, but low-priced without a clear cause.

Harmony Biosciences Holdings (NASDAQ:HRMY) offers an interesting example for this kind of assessment. The commercial-stage pharmaceutical company, centered on treatments for rare neurological disorders, receives a 7 out of 10 in ChartMill’s total basic rating. A closer examination of its detailed basic report shows a profile noted by outstanding valuation measures combined with firm profitability and financial condition, hinting the stock may be missed by the wider market.

Valuation: A Clear Leader

The most notable part of Harmony Biosciences' basic view is its valuation. The company gets a top-level Valuation Rating of 9 out of 10, showing it is priced very appealingly compared to both its own profit ability and its industry group. This is the base of the value investment argument.

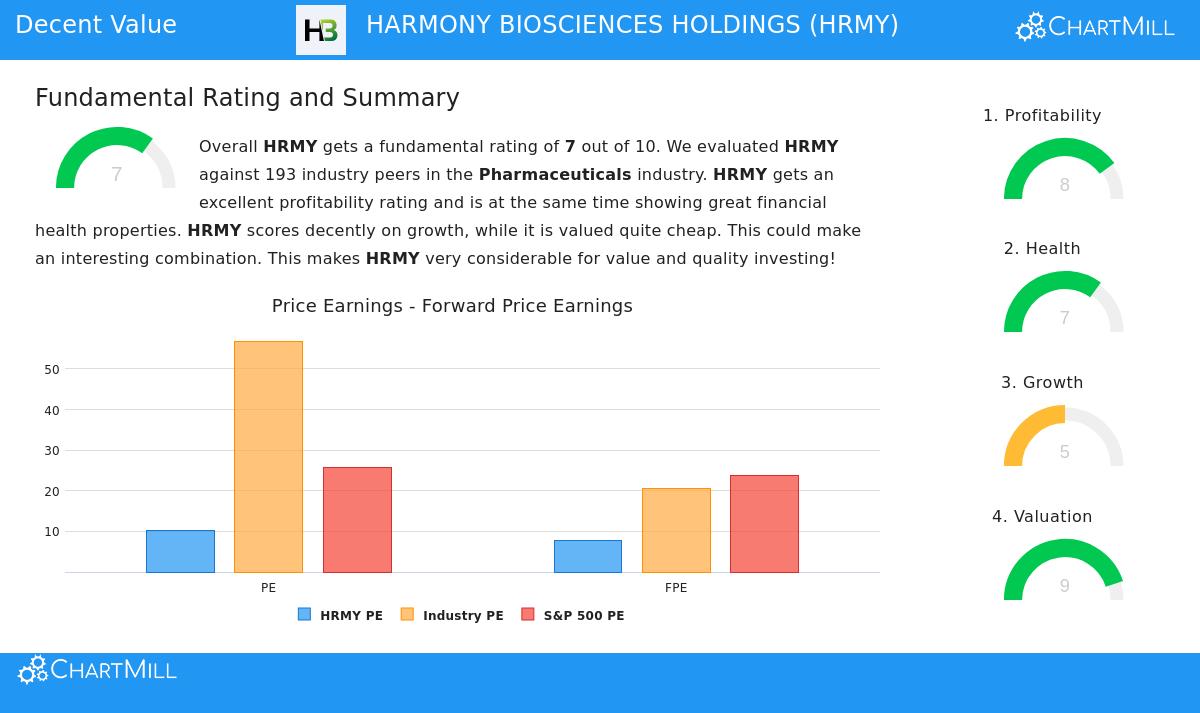

- Price-to-Earnings (P/E): HRMY trades at a P/E ratio of 10.25, which is not only much less expensive than the current S&P 500 average of 25.71 but also puts it in the least expensive 10% of companies within the competitive pharmaceuticals industry.

- Forward P/E: The view stays appealing looking forward, with a forward P/E ratio of 7.67. This is less expensive than over 91% of industry group and under a third of the S&P 500's forward P/E average.

- Cash Flow & EBITDA Multiples: The value argument goes beyond profits. Based on its Enterprise Value to EBITDA and Price/Free Cash Flow ratios, HRMY is valued as less expensive than about 96% and 95% of its industry competitors, in turn.

For a value investor, these measures point to a significant margin of safety. The market is using a large discount to Harmony's profits and cash flows, which could offer protection against mistake and chance for gain if the market re-evaluates the company's value.

Profitability and Financial Condition: The Base of Quality

A low price alone is insufficient; it must be backed by a good business to escape the dangers of a value trap. Harmony Biosciences rates highly here, with a Profitability Rating of 8 and a Condition Rating of 7. This pairing shows the company is not only continuing but doing well financially, which is vital for the long-term strength needed in a value investment.

Profitability Positives:

- The company shows strong margins, with an Operating Margin of 24.00% and a Profit Margin of 18.27%, each doing better than over 91% of the industry.

- Its effectiveness in using capital is very good, shown by a Return on Invested Capital (ROIC) of 15.30%, which exceeds 94% of peers. A steadily high ROIC over recent years shows lasting competitive strengths.

- Harmony has been profitable and produced positive operating cash flow in each of the past five years, showing a history of financial steadiness.

Financial Condition Positives:

- The balance sheet is firm. With a low Debt/Equity ratio of 0.17 and a Debt-to-Free-Cash-Flow ratio of only 0.50, the company has very little debt and can settle its debts quickly with its cash flow.

- Liquidity is strong, with Current and Quick Ratios above 3.5, showing sufficient resources to meet near-term needs.

- An Altman-Z score of 4.42 indicates a very low short-term chance of financial trouble.

This firm condition and profitability profile is exactly what value investors search for to confirm a low-priced stock. It verifies that the low price is probably not a sign of a failed business model or coming financial risk, but possibly a market pricing error.

Growth: A Cautious View

The company's Growth Rating is a more average 5, which gives important setting. Past growth has been notable, with Revenue increasing at an average rate of over 40% in recent years, including 21.5% in the last year. However, analyst forecasts for the future are more guarded, with yearly Revenue growth estimated near 5.4% and EPS growth near 6.4%.

For a value plan, this cautious growth view is not always a bad point. It may partly clarify the market's quiet valuation. The main point is that growth, while easing from its fast past rate, is still forecast to be positive. When joined with the exceptionally low price and high profitability, it hints investors are paying very little for this future growth, which can be an appealing situation.

Conclusion

Harmony Biosciences Holdings shows the traits wanted by a "quality at a discount" filtering method. The stock trades at a large discount to the market and its industry based on almost all normal valuation measures. Importantly, this low valuation is placed next to high scores for profitability and financial condition, showing the basic business is fundamentally healthy and very profitable. While future growth forecasts are moderate, they are positive, and the company's strong cash production and clear balance sheet give stability.

This pairing, being priced like a company in difficulty while performing like one in good condition, is what makes HRMY a interesting option for investors using a systematic value plan centered on finding low-priced quality.

Interested in finding other stocks that match a similar profile of good valuation joined with acceptable basics? You can examine more possible chances using the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis presented is based on data and ratings provided by ChartMill and should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results. Investing in stocks involves risk, including the potential loss of principal.