For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a practical middle path. This method tries to find companies that are showing solid and consistent growth, but whose stock prices are not at high levels. It avoids the speculative excitement often seen with fast-rising growth stocks while also steering clear of value traps, companies that are inexpensive for a cause. One useful way to apply this method is through systematic filtering, searching for stocks with good fundamental growth ratings combined with acceptable valuation, profitability, and financial strength measures. This process helps identify businesses that are growing effectively and are structured to last, without needing investors to pay a high price that might reduce future gains.

A recent filter using these "affordable growth" ideas has identified HEALTHEQUITY INC (NASDAQ:HQY) for closer review. The company, a major provider of technology-supported services for health savings accounts (HSAs) and other consumer-directed benefits, seems to match the central ideas of the GARP approach. A detailed fundamental analysis report on HealthEquity shows a profile characterized by solid expansion, firm core business results, and a valuation that does not seem high compared to its potential.

Strong Growth Path

The base of any GARP candidate is a clear and positive growth direction. HealthEquity’s report displays a positive growth story, receiving a ChartMill Growth Rating of 7 out of 10. The company is not only growing but doing so at a faster rate in important areas.

- Earnings Momentum: The company's Earnings Per Share (EPS) increased by a notable 22.15% over the previous year, with a firm average yearly growth rate of 12.72% over a longer time. Importantly, analysts believe this momentum will persist, forecasting average yearly EPS growth of 19.43% in the next few years.

- Revenue Growth: Top-line growth is equally good. Revenue rose by 12.20% in the last year and has been increasing at an average yearly rate of 17.66% over recent years. While future revenue growth is predicted to slow to an estimated 8.51% yearly, it remains at a sound level that backs the overall growth idea.

This mix of solid past performance and optimistic future estimates is key for the affordable growth method, as it looks for companies where growth is a present fact, not only a future hope.

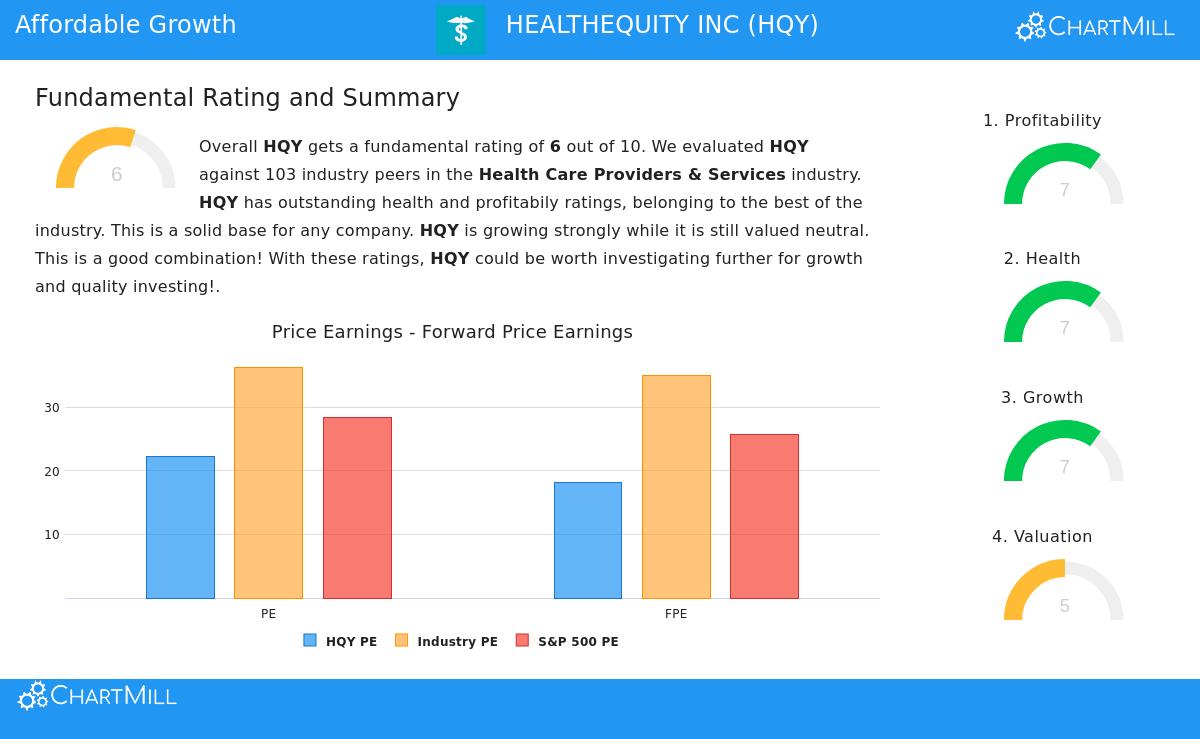

A Valuation That Is Not High

An acceptable valuation is the important balance in the GARP method, making sure investors are not paying too much for that growth. HealthEquity’s Valuation Rating of 5 indicates it is not highly priced, particularly when viewed next to its growth rate and industry competitors.

- Relative Value: With a Price-to-Earnings (P/E) ratio of 22.29, HealthEquity trades at a valuation that is somewhat lower than almost 68% of its peers in the Health Care Providers & Services industry, where the average P/E is above 36.

- Growth-Adjusted Measure: Maybe more revealing is the Price/Earnings-to-Growth (PEG) ratio. The report mentions a "low PEG Ratio," which shows the stock's P/E multiple is acceptable when balanced against its expected earnings growth rate. This is a key measure for GARP investing.

- Market Comparison: The stock’s P/E and its Forward P/E of 18.10 are also valued lower than the current averages for the S&P 500, offering a buffer compared to the wider market.

This valuation view supports the "affordable" part of the filter. The growth is not being overlooked by the market, but it also is not being valued as if it were perfect, leaving possible space for gain as the company follows its plans.

Supporting Fundamentals: Profitability and Strength

For growth to be lasting and the valuation to be reasonable, a company must be profitable and financially stable. HealthEquity scores a 7 on both its Profitability and Financial Strength ratings, providing a solid base.

Profitability Positives:

- The company has very good margins, with a Profit Margin of 14.86% and an Operating Margin of 23.20%, each performing better than over 98% of industry rivals.

- Returns on capital, including Return on Assets (5.65%) and Return on Invested Capital (7.20%), are in the better half of the industry, showing efficient use of shareholder money.

Financial Strength Positives:

- Liquidity is very sound, with a Current Ratio and Quick Ratio of 4.13, indicating no trouble in meeting near-term needs and performing better than over 90% of the industry.

- The balance sheet seems workable, with a Debt-to-Equity ratio of 0.46, which is seen as sound and better than many peers.

These elements are important for the affordable growth method. High profitability suggests the growth is of good quality and can be put back into the business well, while sound financial strength lowers the chance of trouble from economic or operational problems, making the growth story more lasting.

Conclusion

HealthEquity presents a profile that matches closely with the goals of an affordable growth investor. The company shows a clear and quickening earnings growth direction, trades at a valuation that is acceptable both on its own and relative to its growth rate (PEG), and is backed by high-level profitability and a firm financial condition. This mix of features, growth, value, profitability, and strength, is exactly what filters like this try to find: companies that are performing well now and are priced in a manner that allows for future benefit.

Investors curious about examining other companies that match this "Growth at a Reasonable Price" profile can find more possible choices by looking at the results of the Affordable Growth stock filter.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making any investment decisions.