For investors looking to balance the search for growth with fiscal care, the "Growth at a Reasonable Price" or "Affordable Growth" strategy offers a practical middle path. This method looks for companies that are increasing their earnings and revenue faster than average but are also priced at levels that do not require flawless future performance. By selecting stocks with good fundamental growth marks, along with reliable profitability, sound finances, and a fair valuation score, investors may reduce the risks common to high-priced growth stocks while keeping exposure to their possible gains.

Hamilton Lane Inc - Class A (NASDAQ:HLNE) appears as a candidate from this type of selection process, showing a profile that fits this measured investment view.

A Base of Strong Profitability and Financial Soundness

Before examining growth and value, a company must have a steady operational and financial foundation. Hamilton Lane performs well here, receiving a high profitability mark of 8 out of 10. The company shows outstanding returns on capital, a sign of efficient management and a lasting competitive edge.

- Return on Equity (ROE): At 26.61%, HLNE's ROE is better than over 90% of similar companies in the Capital Markets industry.

- Return on Invested Capital (ROIC): A three-year average ROIC of 22.58% is much higher than the industry average, though a recent figure of 16.05% calls for attention to the reason for the drop.

- Good Margins: The company keeps up good profit (30.59%) and operating margins (42.80%), putting it in the top group of its industry.

Financially, Hamilton Lane is in good condition with a rating of 7. Its solvency measures are especially strong, pointing to low bankruptcy risk and a comfortable debt level. The Altman-Z score is solid, and a very low debt-to-free-cash-flow ratio of 0.79 shows the company could clear all its debts in under a year from its operational cash flow. While current and quick liquidity ratios are only satisfactory, they are considered alongside the firm's very good profitability and solvency, which usually balance near-term liquidity considerations.

Showing Steady and Projected Growth

The center of the affordable growth idea is, expectedly, growth. Hamilton Lane gets a growth rating of 7, backed by a good past record and positive future estimates. For an investor using this strategy, maintained historical growth that is forecast to continue is a key pairing.

- Past Performance: Over recent years, HLNE has displayed very good revenue growth, averaging 21.08% each year. Earnings per share (EPS) growth has been even stronger over a multi-year period, averaging above 20%.

- Future Projections: Analysts predict this trend will continue. EPS is estimated to grow at close to 17% each year in the near future, with revenue growth expected near 17.36%. This steadiness in the growth path—where future estimates match past results—lowers the unpredictability often built into a stock's price.

This steady growth picture is important for the strategy because it gives a concrete foundation for valuation. A company with uneven or slowing growth is much more difficult to value fairly, while consistent expansion allows for more assured modeling and evaluation of whether the present stock price offers a good opportunity.

Valuation Considering Quality and Growth

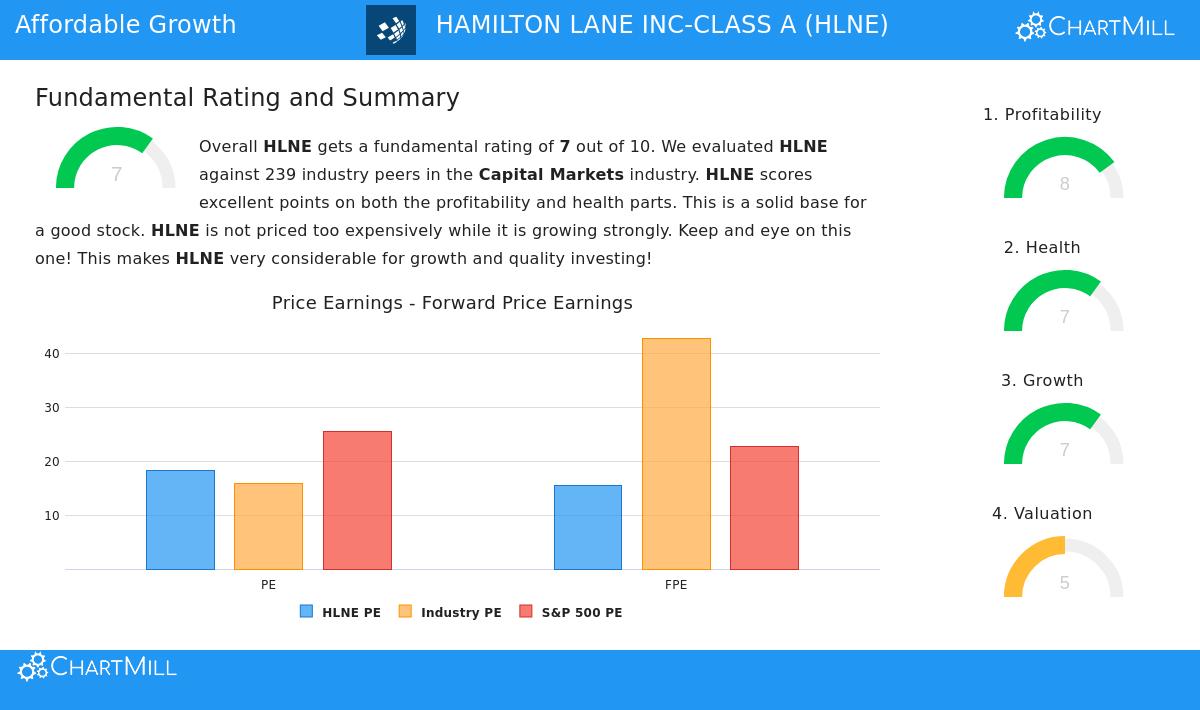

The last, and possibly most important, part is valuation. A stock can show excellent growth and profitability, but if it is valued assuming perfect long-term performance, the potential reward relative to risk weakens. Hamilton Lane's valuation rating of 5 indicates it is not overly expensive, particularly when weighing its quality and growth outlook.

- Price-to-Earnings: With a trailing P/E ratio of 18.18, HLNE trades at a small premium to its industry but at a noticeable discount to the wider S&P 500 average. Its forward P/E of 15.46 is more appealing, sitting below both the industry and S&P 500 averages.

- Cash Flow and EBITDA Multiples: The stock looks more appealing on cash-based measures. Judging by its Enterprise Value to EBITDA and Price to Free Cash Flow ratios, most of its industry peers are priced higher.

- Growth Adjustment: The PEG ratio, which modifies the P/E for estimated growth, shows a fair valuation. The market is not assigning an extreme premium for HLNE's projected ~17% earnings growth, especially when that growth is supported by high profitability.

This fair valuation is the key element of the affordable growth strategy. It means investors are not paying too much for the company's quality and growth path, possibly offering a buffer and space for price improvement if the company keeps performing well.

Summary

Hamilton Lane displays a unified investment profile that matches the ideas of seeking affordable growth. It joins a record of good, profitable expansion with a balance sheet that can fund future plans, all while being valued at a price that does not seem to assume an improbable future. The company's high profitability and financial soundness support the durability of its growth, making the fair price especially significant.

For investors wanting to review other companies that fit similar standards of acceptable growth, decent fundamentals, and fair valuation, more outcomes from the "Affordable Growth" screen are available here.

A full fundamental analysis report for Hamilton Lane (HLNE) is ready for additional study here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making any investment decisions.