The investment philosophy of famous fund manager Peter Lynch focuses on finding well-run, expanding companies trading at sensible prices, a strategy often called Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on lasting earnings expansion, high profitability, and firm financial health, while staying away from high debt. His process, explained in his book One Up on Wall Street, offers a structured system for finding companies that are not just expanding quickly, but doing so in a financially responsible way that can be maintained over many years. This method removes speculative stocks in favor of businesses with clear models and lasting competitive strengths.

One company that currently appears from a filter built on Lynch's main standards is Hamilton Lane Inc. - Class A (NASDAQ:HLNE). The firm is a top provider of private markets investment services, offering solutions across private equity, credit, real assets, and venture capital. For investors looking for long-term GARP possibilities, Hamilton Lane offers an interesting profile that matches closely with the Lynch investment list.

Match with Peter Lynch Standards

A Peter Lynch filter usually looks for companies showing good but maintainable expansion, sensible valuation compared to that growth, high profitability, and a careful balance sheet. Hamilton Lane's present fundamentals hit these specific marks:

- Maintainable Earnings Expansion: Lynch preferred companies with a steady earnings expansion history, but was cautious of unsustainably high rates. Hamilton Lane's earnings per share (EPS) has expanded at an average yearly rate of 20.2% over the last five years. This fits directly within the Lynch-favored range of being above 15% but below 30%, pointing to a solid yet possibly keepable expansion path.

- Sensible Valuation (PEG Ratio): A central part of Lynch's strategy is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks where the price is fair given the expansion rate. A PEG ratio at or under 1.0 is seen as good. Hamilton Lane's PEG ratio, based on its past five-year expansion, is 0.86. This shows the market may be pricing the company at a small discount to its historical expansion performance, a main sign for value-aware growth investors.

- High Profitability (Return on Equity): Lynch searched for companies that effectively create profits from shareholder equity. A high Return on Equity (ROE) is a sign of a good business. Hamilton Lane's ROE of 26.6% is outstanding, greatly beating most of its peers in the capital markets industry and showing better management skill in using capital.

- Financial Health (Debt & Liquidity): A careful balance sheet is key for surviving economic cycles. Lynch stressed low debt. Hamilton Lane's Debt-to-Equity ratio of 0.32 is much below the filter's limit of 0.6, and even under Lynch's stricter personal choice of 0.25, showing a capital structure funded mainly by equity. Also, its Current Ratio of 1.20 shows it keeps enough short-term assets to meet its near-term debts, passing another of Lynch's basic financial health tests.

Fundamental Health and Expansion View

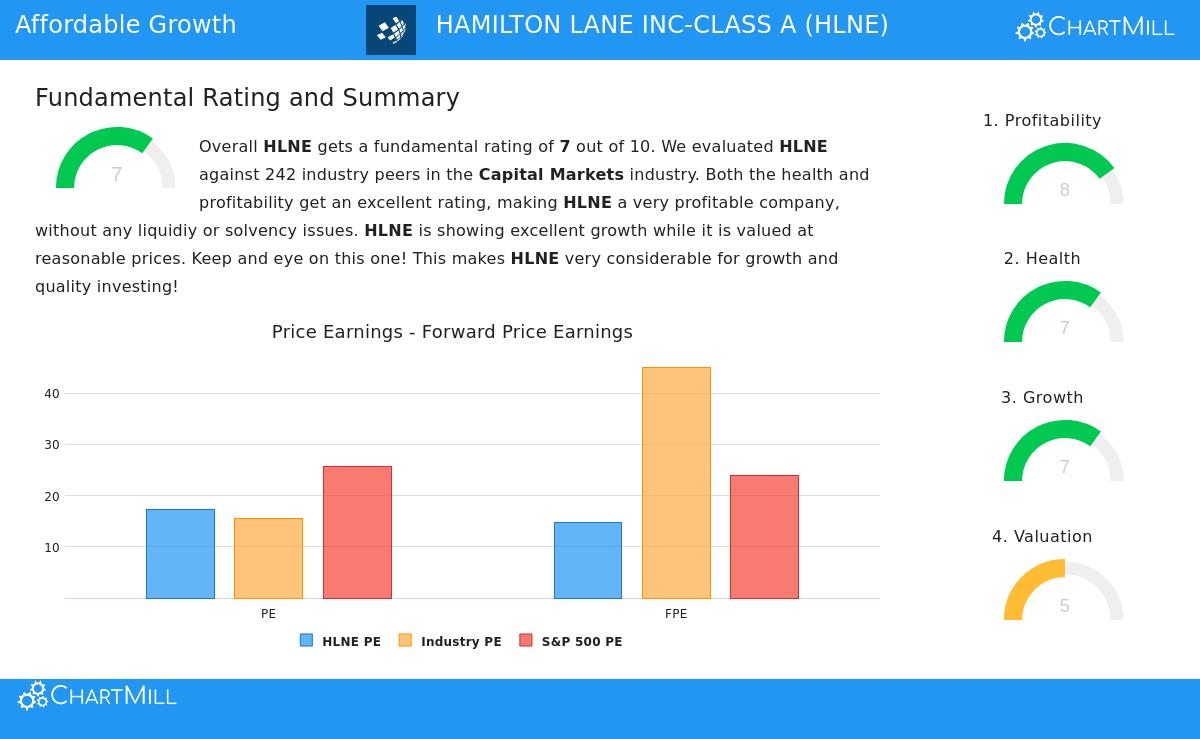

Beyond the specific filter points, a wider look at Hamilton Lane's fundamental report supports its position as a GARP candidate. The company gets a high overall fundamental score of 7 out of 10. Its profitability numbers are especially solid, with top scores for Return on Assets and Return on Invested Capital. The firm's financial stability is also a positive, shown by a good Altman-Z score and a very low Debt-to-Free-Cash-Flow ratio, suggesting little bankruptcy danger and a high ability to repay debt.

While the stock's basic Price-to-Earnings ratio might look fair or somewhat high alone, this is balanced by the company's high expansion and profitability scores. Looking forward, analysts predict continued expansion, with expected EPS growth averaging close to 17% yearly. This future view, paired with its historical performance, backs the idea of maintainable growth. For a complete look at these numbers, you can see the full fundamental analysis report for HLNE.

A Long-Term View

It is key to see this analysis through the view Peter Lynch himself advised. The aim is not short-term trading but finding companies to own for years as their core business increases in value. Hamilton Lane works in the specialized and increasing area of private markets access, a "simple" but necessary sector by Lynch's meaning. Its method of providing advisory services, personalized accounts, and specialized funds creates high-margin, repeating revenue, which is seen in its notable profit margins.

The company's mix of strong past expansion, a sensible valuation when growth is considered, first-class profitability, and a very firm balance sheet makes a profile that is naturally defensive but set for expansion. This two-part nature is central to the GARP strategy, looking for good growth without paying too much for it.

Finding Like Possibilities

Hamilton Lane acts as a real example of how structured filtering can find possible long-term investments. For investors wanting to look at other companies that pass similar strict growth and value filters, the Peter Lynch Strategy screen gives a changing list of candidates that deserve more study.

Disclaimer: This article is for information only and does not make up financial advice, a support, or a suggestion to buy, sell, or own any security. The analysis is based on public data and a particular investment strategy system. All investing has risk, including the possible loss of original money. Investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment choices.