Harmonic Inc (NASDAQ:HLIT) has been identified by a screening process built on Peter Lynch's investment methodology, which highlights finding companies with lasting growth paths trading at fair prices. This method, explained in Lynch's book One Up on Wall Street, centers on fundamental analysis to create a long-term portfolio of companies that show good profitability, sound finances, and yearly earnings growth between 15% and 30% to prevent unstable expansion. The method favors stocks with low price-to-earnings growth (PEG) ratios and acceptable debt levels, matching the "growth at a reasonable price" (GARP) idea that mixes growth possibility with price awareness.

Meeting Peter Lynch Criteria

Harmonic Inc fits a number of important filters from the Peter Lynch screen, which are made to find companies set for long-term achievement without paying too much for growth. The standards make sure that chosen firms are not just expanding but are also financially stable and fairly priced.

- Earnings Growth: Harmonic's EPS has increased at an average yearly rate of 23.05% over the last five years, placing it within Lynch's chosen span of 15–30%. This points to continued, controlled growth instead of sharp but possibly unsteady rises.

- Valuation Compensation: The company's PEG ratio of 0.49 is much lower than the limit of 1, indicating the stock is priced low compared to its earnings growth. Lynch stressed that a low PEG helps prevent paying too much for future growth.

- Financial Health: With a debt-to-equity ratio of 0.27, Harmonic employs less debt than equity for financing, matching Lynch's liking for companies with D/E ratios under 0.6. Also, its current ratio of 1.99 shows good short-term cash availability, going beyond the least needed level of 1.

- Profitability: Harmonic's return on equity (ROE) of 15.38% is above the 15% mark, showing effective use of investor money to create earnings, a key part of Lynch's method for spotting well-run firms.

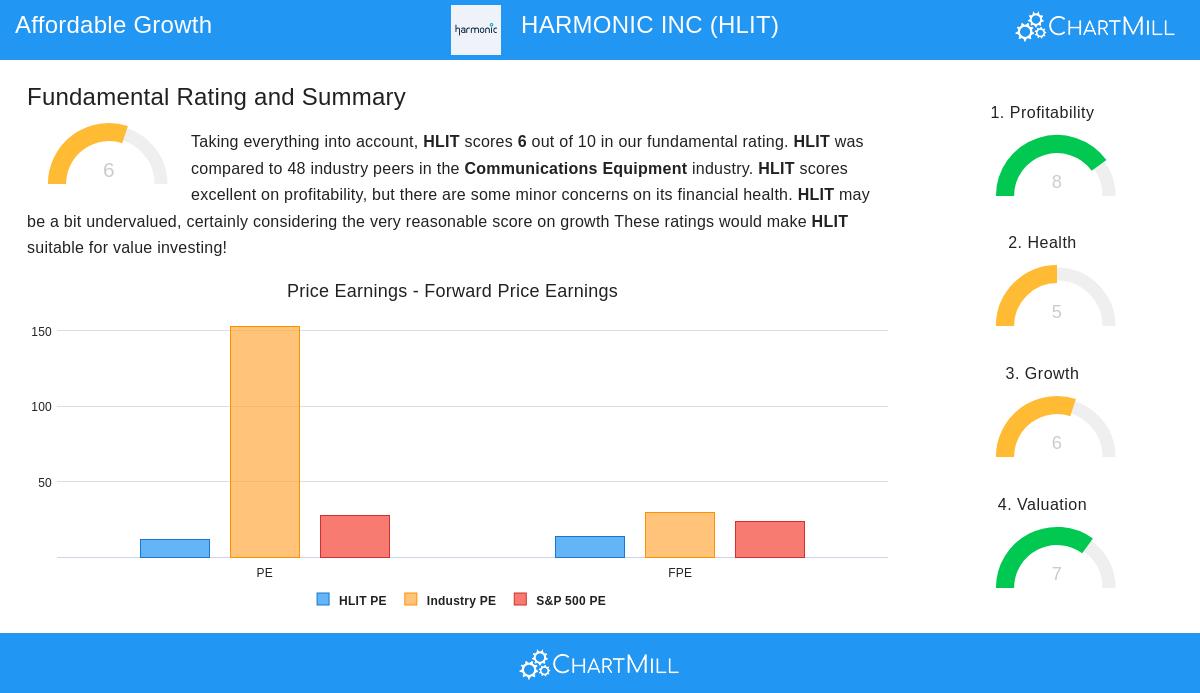

Fundamental Analysis Overview

Harmonic's fundamental rating of 6 out of 10 shows a varied but hopeful profile. The company does very well in profitability, with high marks for return on assets, equity, and invested capital, together with better profit and operating margins. Its valuation numbers are especially noteworthy, with a P/E ratio of 11.35 much lower than industry and S&P 500 averages, signaling possible low pricing. Still, worries exist about financial health, including an Altman-Z score in the trouble area, although this is somewhat balanced by good free cash flow coverage of debt and a firm current ratio. Growth stays strong, with past EPS and revenue gains exceeding many competitors, although future estimates point to a slowing in growth rates.

For a complete breakdown, see the full fundamental analysis report.

Alignment with GARP Investing

For investors looking for growth at a fair price, Harmonic presents a noteworthy case. Its following of Lynch's ideas, through regulated earnings growth, low PEG, and good ROE, places it as a company that can provide returns without the high cost usually linked to fast-growing stocks. The concentration on video delivery and broadband solutions, while not in a trending industry, fits with Lynch's support for investing in comprehensible businesses with consistent need. While the fundamental report notes some dangers, like share dilution and solvency worries, the general numbers back a story of a profitable, expanding company available at a good price.

Investors curious about reviewing other companies that fit similar standards can access the Peter Lynch screen here for more options.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.