For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) or "affordable growth" method presents a solid middle path. This tactic tries to find companies that are showing good and lasting growth, but whose stock prices are not too high. By using a multi-part fundamental review that grades stocks on growth, price, earnings, and financial soundness, investors can methodically search for businesses that mix possible increase with fair cost and steady operations. This process helps sidestep the dangers of paying too much for excitement while still taking part in the rise of fundamentally healthy, expanding companies.

One stock that recently appeared through such an affordable growth filter is Houlihan Lokey Inc (NYSE:HLI), a major global investment bank. The filter, which searched for stocks with high growth grades, fair prices, and acceptable scores for earnings and financial soundness, noted HLI as a candidate for more examination.

Growth Path: A Main Feature

The main attraction of an affordable growth stock is, expectedly, its growth picture. Houlihan Lokey is strong in this group, getting a solid Growth Rating of 7 out of 10 from ChartMill’s review. The company’s financial reports show a history of steady and notable increase.

- Earnings Per Share (EPS) Growth: Over the last year, HLI’s EPS rose by a notable 40.97%. The longer-term view is also good, with an average yearly EPS increase of 14.36% over recent years.

- Revenue Growth: The top line is also increasing strongly. Revenue grew 18.05% in the last year and has gone up at an average yearly rate of 15.56% in the past.

- Future View: This speed is projected to keep going. Analyst forecasts point to an average yearly EPS increase of 16.43% and revenue growth of 12.90% in the next few years, showing that the company’s growth narrative is not finished.

This steady history and positive forward view are just what growth-focused investors want, giving a base for possible stock price gains.

Price: Fair During Growth

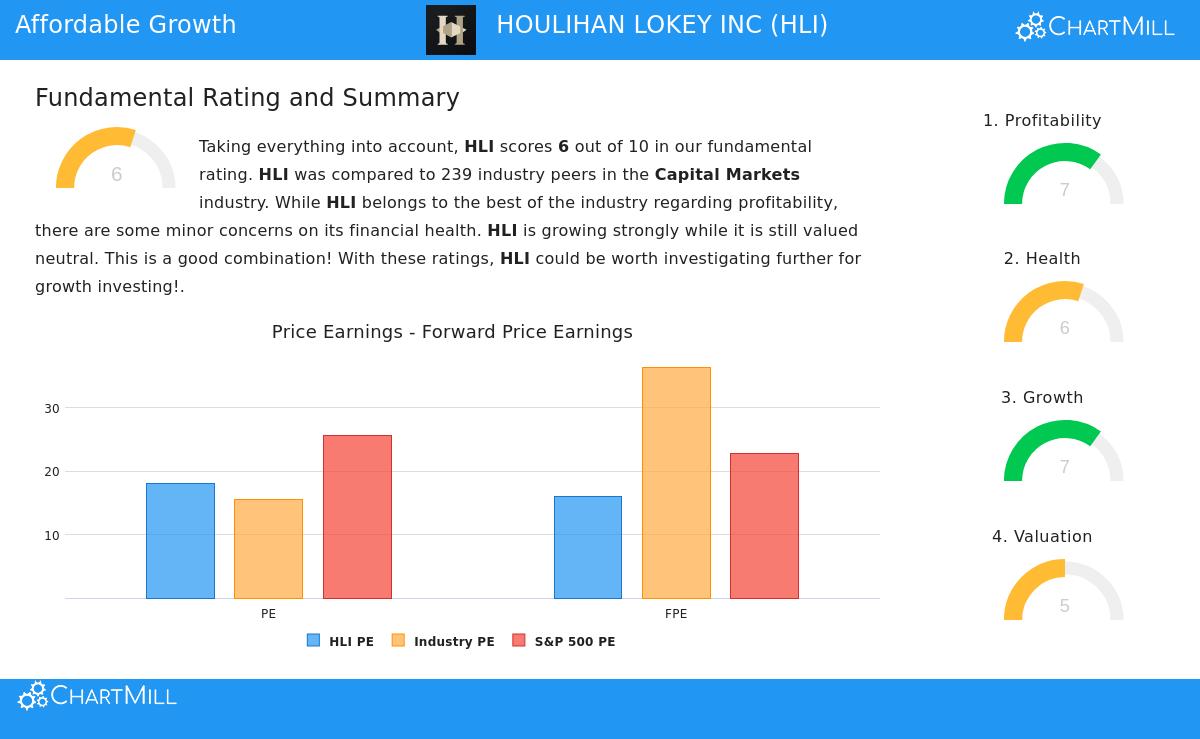

A main idea of the affordable growth tactic is making sure the cost paid for that growth is not too high. This is where price measures become important. HLI gets a Price Rating of 5, which is in a middle area, meaning the stock is not obviously low-cost nor overly costly compared to its fundamentals.

- Price-to-Earnings (P/E): At 18.01, HLI’s P/E ratio is above the industry average, making it costlier than many of its capital markets peers. However, it sells at a clear lower price than the wider S&P 500’s average P/E of 25.61.

- Forward-Looking Measures: The price view gets better when looking forward. The forward P/E ratio of 16.01 matches the industry and is less expensive than the S&P 500. More interesting are measures like Enterprise Value to EBITDA and Price/Free Cash Flow, where HLI is priced more cheaply than a large part of its industry rivals.

- Growth Adjustment: The low PEG ratio, which changes the P/E for projected earnings growth, shows the market may not be completely counting HLI’s future growth possibility, suggesting a fair price for the growth available.

For an affordable growth filter, this price picture is key. It implies investors are not paying extra for past results alone but may be getting future growth at a sensible cost.

Earnings and Financial Soundness: The Supporting Parts

Lasting growth cannot be without basic earnings and a firm financial base. HLI grades well here, with an Earnings Rating of 7 and a Financial Soundness Rating of 6.

Earnings Points: The company is very good at making returns from its assets and equity. Its Return on Invested Capital (ROIC) of 19.40% and Return on Equity (ROE) of 19.52% are some of the top in its industry, doing better than over 80% of peers. This shows management’s ability to use capital well to build value for shareholders—a key feature for a growing company.

Financial Soundness Notes: HLI’s balance sheet is very strong regarding solvency, having no debt and a very good Altman-Z score, which means a very small chance of financial trouble. This gives important steadiness and options. A small point to note is the company’s cash position, with current and quick ratios just under 1.0, which is normal in its industry but shows it depends on steady cash flow to meet immediate bills.

These firm grades in earnings and soundness are essential for the affordable growth tactic. They give trust that the company’s growth is built on a lasting operational model and a stable financial footing, lowering investment risk.

Summary

Houlihan Lokey Inc presents a solid example for the affordable growth investment method. It pairs a clear and projected good growth path—the driver for returns—with a price that seems fair, especially when thinking about its future earnings possibility and profitability. Backed by high returns on capital and a balance sheet with no debt, HLI’s growth looks to be both high-quality and lasting.

This mix of traits is what methodical filters are made to find. For investors curious about reviewing other stocks that fit similar rules of good growth, fair price, and decent fundamentals, you can see the full fundamental analysis report for HLI or find more possible choices by going to the Affordable Growth stock filter.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer or request to buy or sell any securities. The review is based on data and grades from ChartMill, and investors should do their own research and talk with a qualified financial advisor before making any investment choices.