For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a sensible middle path. This method tries to find companies that are increasing their earnings and revenue at a good rate but are also priced at levels that do not require flawless future results. By filtering for stocks with good growth scores, firm profitability, sound finances, and fair prices, investors can search for chances where the market may not completely recognize a company's prospects. One company that recently appeared from such a filter is the investment bank Houlihan Lokey Inc (NYSE:HLI).

A Closer Look at Growth Metrics

The central idea of an affordable growth strategy is, expectedly, growth. Houlihan Lokey’s fundamental report shows a solid growth picture, receiving a ChartMill Growth Rating of 7 out of 10. This score indicates good momentum in both the recent history and the expected future.

- Past Performance: The company has shown notable expansion, with Earnings Per Share (EPS) rising 40.97% over the last year and increasing at a yearly rate of 14.36% over several years. Revenue growth has been similarly good, up 18.05% last year with a multi-year yearly growth rate of 15.56%.

- Future Expectations: Analysts predict this momentum will persist, with EPS expected to grow at a typical yearly rate of 16.34% and revenue predicted to rise by 13.02% yearly in the next few years. This alignment between past results and future predictions is a main part in judging lasting growth, an important element for the GARP method.

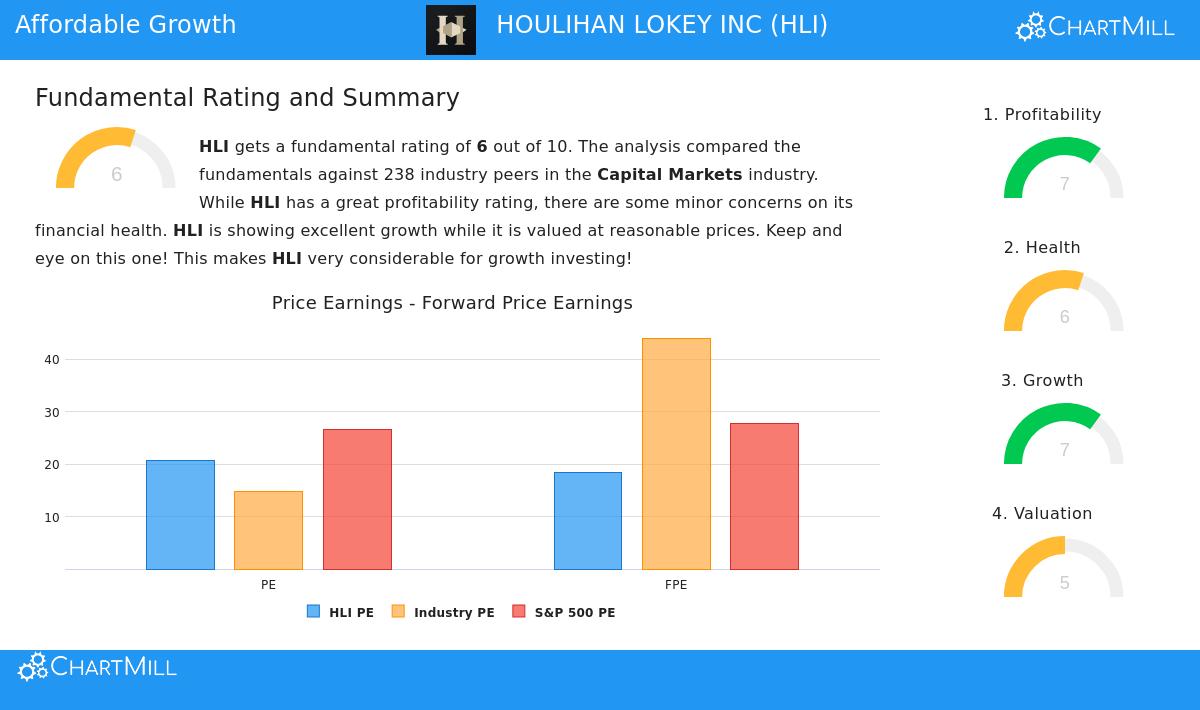

Valuation: Judging the "Affordable" Part

A stock can show excellent growth but still be a bad investment if its cost is too steep. The price assessment is what divides a speculative growth purchase from an "affordable" one. Houlihan Lokey gets a ChartMill Valuation Rating of 5, pointing to a varied but generally fair view when its growth is taken into account.

- Traditional Multiples: On a standard Price-to-Earnings (P/E) basis, HLI trades at 20.70, which seems high next to its industry average. Still, this must be seen with context. The company’s P/E is lower than the wider S&P 500 average of 26.64, and its forward P/E of 18.42 is also less expensive than the market.

- Growth-Adjusted Value: More revealing for a growth stock is the Price/Earnings-to-Growth (PEG) ratio, which includes expected earnings growth. Houlihan Lokey’s low PEG ratio implies the market may not be completely accounting for its predicted growth rate, indicating a possibly lower price. Also, measures like Enterprise Value to EBITDA and Price to Free Cash Flow show the company is priced more cheaply than a large number of its competitors in the capital markets industry.

Supporting Fundamentals: Profitability and Financial Health

For growth to be lasting and for a fair price to be valid, a company must be profitable and financially stable. These are the supporting structures of the affordable growth filter. Houlihan Lokey scores a 7 for Profitability and a 6 for Financial Health.

The high profitability rating is supported by very good returns on capital. The company’s Return on Invested Capital (ROIC) of 19.40% puts it in the best group of its industry, doing better than over 95% of peers. Its Return on Assets and Return on Equity are also much higher than industry averages, showing highly effective use of its resources to produce profits.

The financial health score shows a detailed picture. On the good side, the company has no debt and has a very strong Altman-Z score, almost removing bankruptcy risk. The main issue is with liquidity, with current and quick ratios below 1.0, hinting at possible difficulties in meeting immediate obligations without new cash flow, a significant point for investors to watch, though it is not unusual in some financial services business models.

Why This Fits the Strategy

Houlihan Lokey’s profile matches the affordable growth idea well. The strategy looks for companies where growth is not a wish but a shown and predicted fact, which HLI displays through its steady double-digit EPS and revenue increase. It then needs this growth to be obtainable at a cost that does not presume perfect performance far ahead. Here, HLI’s price, especially on growth-adjusted measures and cash flow bases, seems fair compared to both its own potential and the market. The firm profitability confirms the growth is of high caliber, produced from effective operations, while the acceptable health rating (with noted points) indicates a stable enough base to keep performing its plan.

For investors wanting to examine other companies that match this mix of growth, price, and fundamental soundness, more results from this Affordable Growth filter can be found here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and ratings provided by ChartMill, and investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.