In the world of investing, the search for undervalued opportunities is a constant pursuit. One systematic approach involves screening for companies that appear fundamentally inexpensive relative to their intrinsic worth, yet still demonstrate the underlying financial strength and operational quality to justify a higher price. This method, often used by value investors, looks beyond a simple low price tag. It seeks stocks with an attractive valuation, trading at a discount to their peers and the broader market, while also showing solid profitability, a healthy balance sheet, and promising growth prospects. The goal is to find potential bargains where the market may be missing quality, offering a margin of safety for the long-term investor.

A recent scan using this "decent value" method has identified GOLD FIELDS LTD-SPONS ADR (NYSE:GFI) as a candidate for closer review. The South African-based gold miner, with a global portfolio of assets, shows a profile that fits the central ideas of value investing: it seems inexpensive on key measures while rating highly on fundamental condition and results.

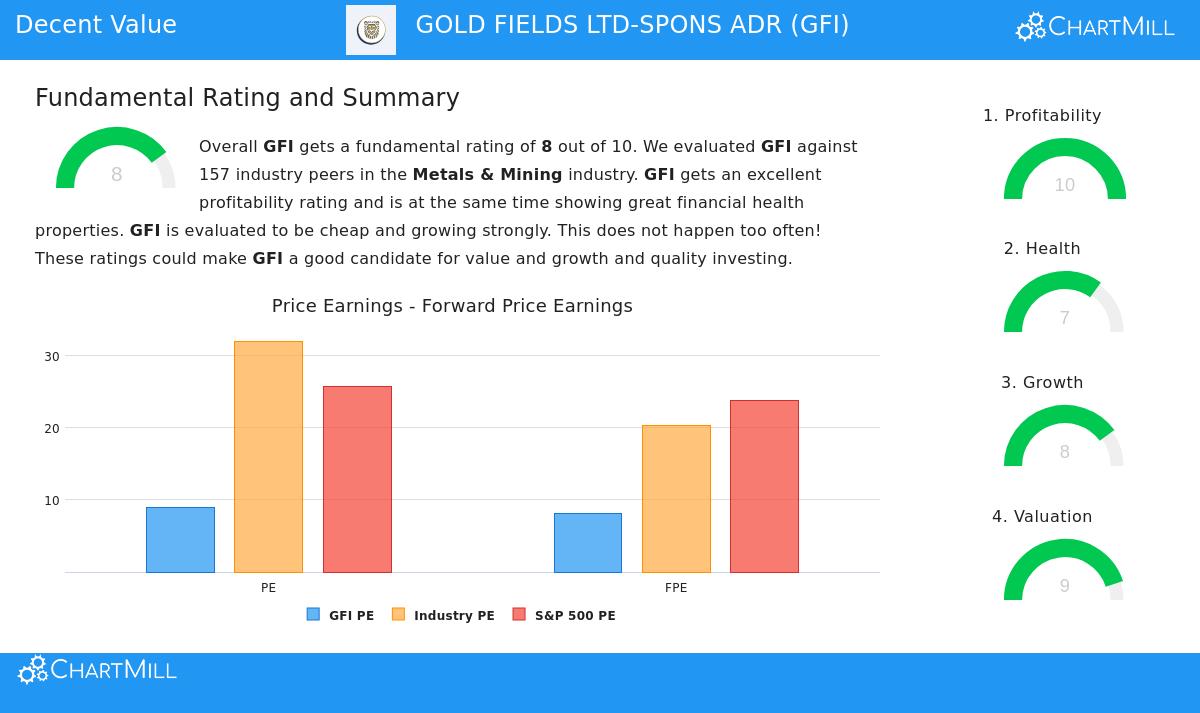

Valuation: A Clear Discount

The foundation of any value case is an attractive price. According to the ChartMill Fundamental Analysis Report for GFI, the stock receives a top Valuation Rating of 9 out of 10. This score shows the company is trading at a notable discount relative to both its industry and the broader market. For value investors, a low valuation gives the necessary starting point, indicating the market may be incorrectly pricing the company's future cash flows.

- Price-to-Earnings (P/E): GFI's P/E ratio is 8.89, which is seen as reasonable on an absolute basis. More significantly, it is less expensive than over 99% of its peers in the Metals & Mining industry, where the average P/E is above 32.

- Forward P/E: Looking ahead, the valuation stays attractive with a forward P/E of 8.08, less expensive than nearly 85% of industry competitors.

- Enterprise Value to EBITDA: This measure, which includes debt, also shows undervaluation, with GFI valued as less expensive than about 93% of its industry group.

This wide discount across several valuation views is exactly what value screens aim to find. It indicates that even if the company's growth slows from recent high levels, the current price may already account for a negative outlook.

Profitability & Financial Health: A Strong Foundation

An inexpensive stock is only a good investment if the basic business is stable. This is where GFI's profile becomes especially notable. The company has a perfect Profitability Rating of 10/10 and a good Health Rating of 7/10. For a value investor, these scores are vital; they show that the "bargain" is not due to a poor business, but possibly a market mistake regarding a capable operator.

Profitability Points:

- High Returns: The company produces excellent returns on its assets (ROA of 30.17%) and invested capital (ROIC of 34.48%), doing better than most of its industry.

- Strong and Improving Margins: GFI operates with notable profit (37.57%) and operating margins (57.01%), which have been rising steadily in recent years. This operational effectiveness is a main source of cash flow.

Financial Health Review:

- Solvency Strength: GFI has an Altman-Z score of 7.06, showing a very low near-term risk of financial trouble. Its debt-to-free-cash-flow ratio is a sound 1.37, meaning it could pay off all debt with less than a year and a half of its cash flow.

- Controlled Leverage: While its debt-to-equity ratio is higher than some peers, the report states this is balanced by strong free cash flow production. The overall view is of a company with a firm balance sheet able to fund operations and handle industry cycles.

This pairing of high profitability and good financial condition lowers the risk often linked with deep-value stocks. It offers the stability value investors want while waiting for the market to see the company's intrinsic worth.

Growth: The Possible Catalyst

While pure value investments sometimes involve flat businesses, GFI includes an active element with a strong Growth Rating of 8/10. This growth part can serve as a reason for a new assessment of the stock's valuation. The company is not just inexpensive on current earnings; it is increasing those earnings at a solid rate.

- High Past Results: Over the past year, GFI has provided very high growth, with Earnings Per Share (EPS) up 267.75% and Revenue rising by 135.10%. This was caused by both operational results and higher gold prices.

- Continued Forward Progress: Looking forward, analysts expect solid ongoing growth, with EPS predicted to grow over 21% each year and Revenue expected to rise by more than 13% per year.

For the value investor, this growth story is significant. It suggests the discount to intrinsic value could shrink not only through multiple improvement (the P/E ratio increasing) but also through the steady growth of the earnings base itself. The company’s 3.11% dividend yield, which is above both the industry and S&P 500 averages and has a record of growth, adds to the total return potential.

Conclusion: An Attractive Value Case

GOLD FIELDS LTD presents a detailed case for investors using a careful value plan. The stock appears as deeply undervalued, trading at a portion of the multiples held by its industry. Importantly, this low valuation is combined with high profitability measures and a financially sound balance sheet, reducing the risk of a standard "value trap." The inclusion of a strong recent and expected growth path provides a possible source for share price gains beyond a simple multiple change. In summary, GFI seems to provide the uncommon mix of a value price on a quality, advancing asset.

Find More Undervalued Opportunities The review of GFI came from a systematic screening process. If you are interested in finding other companies that fit similar standards of sound valuation, health, profitability, and growth, you can review the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on data and reports provided by third parties. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions. Past performance is not indicative of future results.