In the world of investing, the search for undervalued companies is a cornerstone of the value investing philosophy. This strategy, popularized by Benjamin Graham and Warren Buffett, involves identifying stocks trading below their intrinsic value, offering a potential "margin of safety" for investors. A disciplined approach often looks for companies that are not just cheap on paper, but also possess solid underlying fundamentals. This means screening for stocks with attractive valuations while ensuring they maintain decent profitability, financial health, and growth prospects, thereby avoiding potential "value traps" where a low price signals deeper problems rather than opportunity.

GENPACT LTD (NYSE:G), a global professional services firm focused on digital transformation and business process management, emerges as a candidate from such a screening methodology. The company was identified using a "Decent Value" screen that prioritizes a strong fundamental valuation rating while requiring decent scores in profitability, financial health, and growth. A review of Genpact's detailed fundamental analysis report reveals why it fits this profile and may warrant a closer look from investors employing a value-oriented strategy.

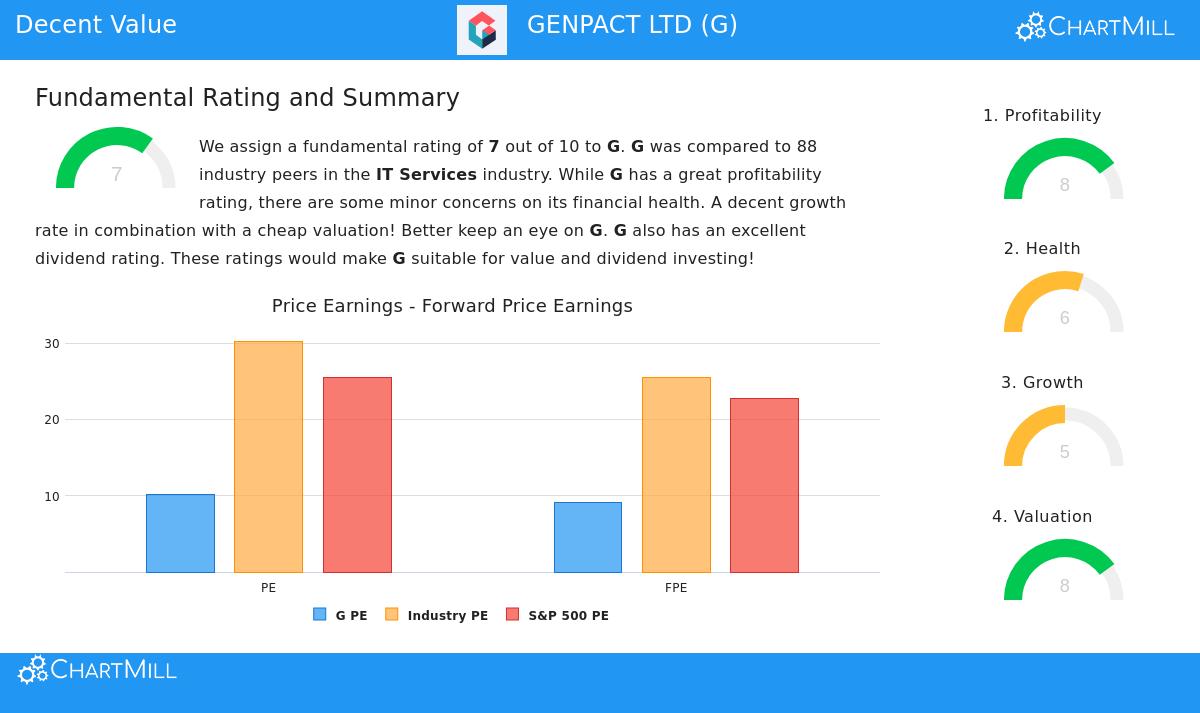

Valuation: The Core of the Opportunity

For a value investor, an attractive valuation is the primary entry point. It represents the potential discount to intrinsic value. Genpact's fundamentals perform well in this area, earning a high valuation rating of 8 out of 10. The metrics suggest the stock is priced conservatively relative to both its earnings and its industry.

- Price-to-Earnings (P/E) Ratio: At 10.17, Genpact's P/E ratio is considered reasonable and is significantly cheaper than 84% of its peers in the IT Services industry. It also stands well below the current S&P 500 average of approximately 25.5.

- Forward P/E Ratio: An even more notable figure is the forward P/E of 9.09, which is cheaper than nearly 83% of industry competitors. This indicates the market is valuing its near-term earnings power at a steep discount.

- Cash Flow and EBITDA: The value case is further supported by a low Price/Free Cash Flow ratio, where Genpact is cheaper than almost 89% of the industry, and an attractive Enterprise Value to EBITDA multiple.

This group of valuation metrics is important because it provides the statistical foundation for a margin of safety. A low P/E ratio in isolation is not enough, it must be considered alongside the company's ability to generate those earnings consistently, which leads to an examination of profitability.

Profitability: Quality at a Discount

A cheap stock is only a good investment if the underlying business is sound and profitable. This is where many pure value plays falter, but Genpact demonstrates notable strength, scoring an 8 for profitability. The company not only earns money but does so with efficiency that ranks highly within its sector.

- Return Metrics: Genpact's Return on Invested Capital (ROIC) of 13.59% outperforms over 86% of its industry peers and is above its own three-year average, indicating improving capital allocation. Its Return on Equity of 21.67% is also in the top tier of the industry.

- Healthy Margins: The company maintains a strong Operating Margin of nearly 15%, better than 80% of competitors, and this margin has been increasing in recent years. A solid Profit Margin of 10.88% further confirms the company's ability to convert revenue into earnings.

For a value investor, this high profitability is essential. It suggests the business has a durable competitive advantage and efficient operations, reducing the risk that the low valuation is a symptom of permanent decline. Strong profitability also supports the company's financial health and its ability to return capital to shareholders.

Financial Health and Dividend

A company's financial resilience ensures it can weather economic downturns and continue investing for the future. Genpact's financial health rating of 6 reflects a generally solid, if not exceptional, position. Key solvency metrics are reassuring.

- Debt Management: With a Debt-to-Equity ratio of 0.46, the company is not overly reliant on debt financing. More impressively, its Debt to Free Cash Flow ratio of 2.16 is good, indicating it could pay off all its debt with just over two years of cash flow, a metric better than 72% of its peers.

- Dividend Profile: Complementing its value proposition, Genpact carries a dividend rating of 7. It offers a yield of 2.00%, which is above the industry average, and has a reliable track record of increasing its payout for at least five consecutive years, with an average annual growth rate near 12%. The payout ratio is a sustainable 21% of income, leaving ample room for reinvestment and further growth.

This combination of manageable debt, strong cash flow coverage, and a growing dividend is attractive for value investing. It provides an income stream while you wait for the valuation gap to close and indicates a shareholder-friendly management team confident in the company's future cash flows.

Growth: The Engine for Revaluation

Finally, for a value stock to realize its potential, there needs to be a catalyst for the market to re-evaluate its price. Steady growth provides that catalyst. Genpact's growth rating of 5 points to a business that is expanding at a measured, stable pace.

- Historical Growth: Over the past year, Earnings Per Share (EPS) grew by a healthy 14.02%, with an average annual EPS growth of 11.54% over recent years. Revenue growth has been more modest but consistent, averaging around 6.5%.

- Future Expectations: Analysts project this momentum to continue, with EPS expected to grow at an average rate of 12.09% annually in the coming years, supported by revenue growth forecasts of approximately 7.7%.

This steady growth is the final piece of the puzzle. It suggests the company is not stagnant, which is vital for the intrinsic value to increase over time. For value investors, sustainable growth at a reasonable price (often highlighted by a low PEG ratio) can signal a high-probability opportunity for capital appreciation as earnings expand and the market potentially awards the stock a higher multiple.

Conclusion

Genpact Ltd presents a case study in applied value investing principles. It is not a deep-value, distressed turnaround story, but rather a financially healthy, profitable, and growing business that the market appears to be pricing at a significant discount to its peer group and the broader market. The company's high valuation rating, coupled with solid scores in profitability, financial health, and growth, aligns with a strategy seeking quality at a reasonable price. This profile aims to balance the potential reward of a low valuation with the reduced risk offered by strong fundamentals.

Investors interested in similar opportunities can explore the predefined "Decent Value Stocks" screen or customize their own search using the fundamental ratings on ChartMill's stock screener to find other companies that may meet their specific criteria.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and ratings provided by ChartMill, and investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.