For investors looking for a disciplined, long-term method to assemble a portfolio, few strategies are as respected as Peter Lynch’s method. As the famous manager of the Fidelity Magellan Fund, Lynch supported a philosophy of putting money into familiar companies and concentrating on businesses with durable growth, sound financial condition, and fair prices. His method, often called Growth at a Reasonable Price (GARP), steers clear of speculative stocks in favor of firms that are profitable, easy to grasp, and priced in a way that does not overestimate their future potential. A filter using his main ideas recently found Fluor Corp (NYSE:FLR) as a possible option for more examination.

A Filter for Durable Growth

The Peter Lynch filter looks for companies that show a particular profile: steady but not extreme earnings increase, high earnings ability, a solid financial position, and a good price when growth is considered. The aim is to locate soundly managed businesses the market might not fully recognize, offering a chance for long-term gain. For a stock such as Fluor Corp, a worldwide engineering, procurement, and construction company, the filter points out several important measures that fit this thinking.

How Fluor Corp Fits the Lynch Standards

The filter uses particular number-based rules, and Fluor’s present situation shows a strong fit on multiple points:

- Earnings Growth (5-Year Average): 27.7%

- Why it matters: Lynch wanted companies with a confirmed history of earnings increase, usually between 15% and 30%. Growth beyond 30% was seen as possibly not lasting. Fluor’s five-year average EPS growth of 27.7% fits right in this desired range, showing a good past record.

- PEG Ratio (Past 5 Years): 0.64

- Why it matters: This is a central part of the Lynch method. The Price/Earnings to Growth (PEG) ratio helps decide if a stock’s price is fair compared to its past growth rate. A PEG under 1.0 is seen as good, hinting the market may not completely account for the company’s growth. Fluor’s PEG of 0.64 indicates it might be trading at a fair price considering its past growth.

- Return on Equity (ROE): 65.3%

- Why it matters: Lynch liked companies that produce high returns on shareholder equity, a signal of effective management and earnings ability. An ROE above 15% was a least requirement. Fluor’s very high ROE of 65.3% is much greater than this mark, showing high earnings ability within its industry.

- Debt-to-Equity Ratio: 0.21

- Why it matters: Financial condition is critical. Lynch chose companies with little debt, often wanting a D/E ratio below 0.25 to make sure of stability during economic slowdowns. Fluor’s ratio of 0.21 shows a careful financial setup supported more by equity than debt.

- Current Ratio: 1.45

- Why it matters: This checks a company’s capacity to pay its short-term bills. A ratio above 1.0 is necessary, and Fluor’s 1.45 suggests a sufficient cash position to manage upcoming debts.

Basic Condition and Price Setting

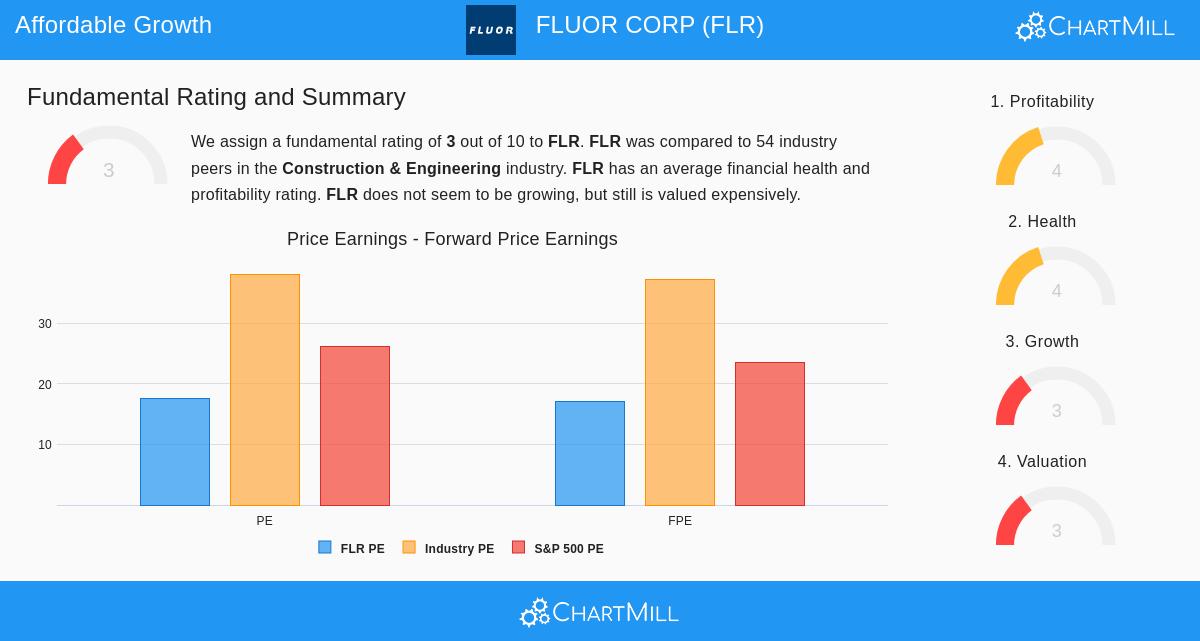

While the Lynch filter gives a good beginning, a closer review of Fluor’s total basic situation, as described in its detailed examination report, adds needed detail. The report gives Fluor a middle overall score, noting a varied result across different groups.

The company’s clear advantage is its earnings ability, where measures like Return on Assets and Profit Margin are some of the top in the Construction & Engineering field. Its financial condition is also seen as middle to positive, with the small debt amount and good cash ratios being definite pluses, although its Altman-Z score implies it is in a steady, if not outstanding, place regarding failure risk.

The more difficult parts are growth and price setting. While past EPS growth has been good, recent patterns show a small drop, and future growth forecasts are low. On price, Fluor’s P/E ratio of 17.6 is seen as high on a plain level, though it is lower than many of its industry competitors and the wider S&P 500. This contrast is important for GARP investors: the stock seems fairly priced compared to its competitors and its own past growth (as shown by the low PEG ratio), but not clearly a low-price find.

Is Fluor a Lynch-Type "Simple" Company?

A frequently missed part of Lynch’s method is his liking for companies in "simple" fields. Fluor’s work—large engineering and construction for energy, city systems, and government plans—is complicated but basically clear. It supplies needed services that are always required, even if they are not seen as exciting. For a long-term investor, this can be a benefit, as it might keep the stock away from short-term traders and let its basic story develop over time.

Looking for More Investment Options

Fluor Corp stands for one possible option found through a structured use of Peter Lynch’s ideas. Investors curious about finding other companies that pass this same group of rules for durable growth, financial soundness, and fair price can review the complete results using the Peter Lynch Strategy stock filter.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. The Peter Lynch filter is a model based on past standards and does not promise future results. Investors must do their own complete study and think about their personal money situation and risk comfort before making any investment choices.