For investors looking for chances where a company's market price may not completely match its basic financial condition, a systematic filtering method can be a good first step. One way is to find stocks that seem basically priced low while also showing good operational soundness and earnings, along with acceptable expansion potential. This method tries to locate companies selling for less than their true worth, not because of weak basics, but possibly because of market shortsightedness or temporary worries. A "Decent Value" filter, which selects for stocks with high valuation grades together with good grades in earnings, financial condition, and expansion, puts this search into practice.

Exelixis Inc (NASDAQ:EXEL) comes up as a result from this kind of filtering. The cancer-centered biopharmaceutical company, recognized for its main cancer treatment cabozantinib, shows a financial picture that deserves more examination from the investor focused on value.

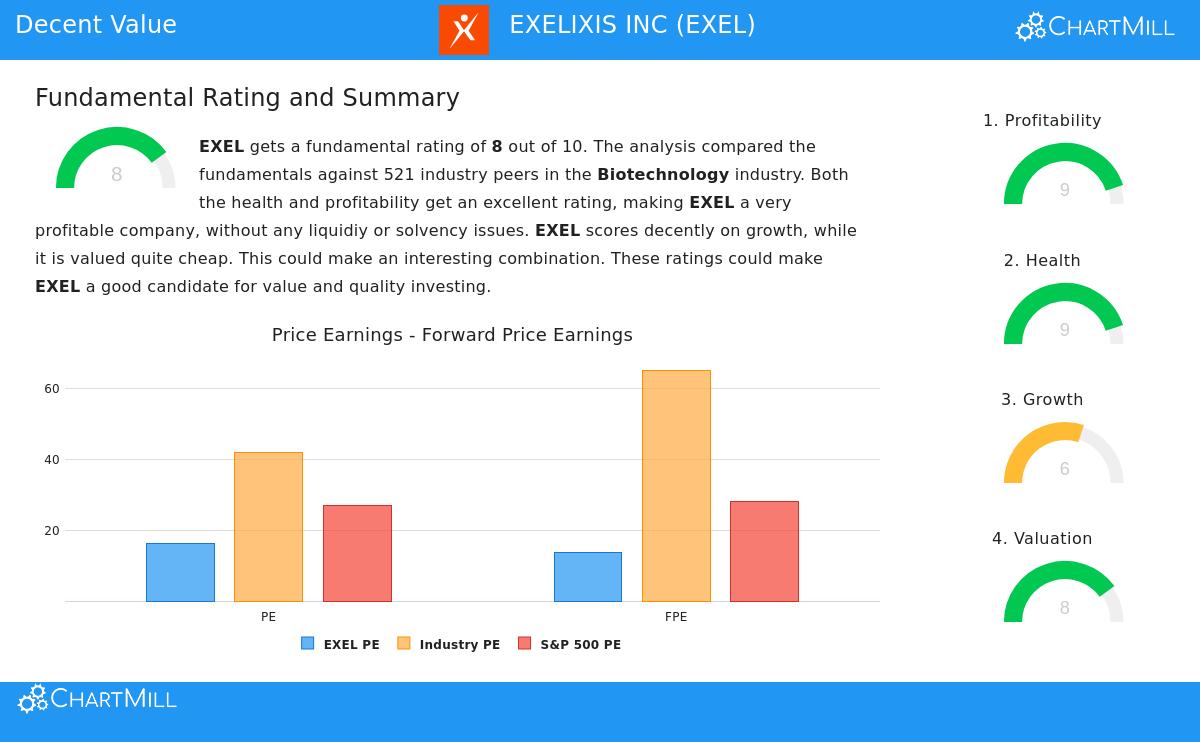

Valuation: An Appealing Starting Price

The central idea of value investing is buying a dollar of assets for fifty cents. Exelixis's valuation numbers indicate the market might be giving such a lower price, particularly in its high-profit industry. Based on ChartMill's basic analysis, the stock gets a good Valuation grade of 8 out of 10.

- Price/Earnings Ratio: At 16.16, EXEL's P/E ratio is much lower than 95.78% of its biotechnology industry counterparts, whose average P/E is above 41. It also sells for a marked discount compared to the wider S&P 500's present average P/E of about 27.

- Forward-Looking Numbers: The valuation view stays appealing on a forward basis. The Price/Forward Earnings ratio of 13.77 is lower than 96.74% of industry rivals and much under the S&P 500 average.

- Cash Flow & EBITDA: The company's attraction goes past earnings. Judging by its Price/Free Cash Flow and Enterprise Value to EBITDA ratios, EXEL is priced more affordably than over 96% of its industry group.

This combined information forms a view of a company whose present stock price does not appear to completely account for its earnings and cash production ability compared to both its direct competitors and the overall market.

Financial Condition: A Strong Balance Sheet

A low price is only a value trap if the company's base is weak. For value investors, a safety net is often located in sound financial condition, and Exelixis does very well here with an almost perfect Condition grade of 9.

- Operation Without Debt: The company has no debt, leading to a Debt/Equity ratio of zero. This removes interest cost risk and gives great strategic and financial room to maneuver, an uncommon and strong benefit in expensive biotech.

- Good Solvency: An Altman-Z score of 12.79 shows almost no short-term bankruptcy danger and does better than 84% of the industry.

- Plenty of Liquidity: With a Current Ratio of 3.56 and a Quick Ratio of 3.50, the company has more than enough liquid assets to meet its near-term responsibilities many times.

This clean balance sheet works as an important protection, shielding the company during industry declines or research difficulties and supplying the means to take advantage of new chances without weakening shareholders or using expensive debt.

Earnings: High-Performance Operation

Value is not only about a low price, it is about the caliber of the earnings and assets you are purchasing. Exelixis shows outstanding operational effectiveness, receiving an Earnings grade of 9.

- Better Returns: The company produces a Return on Invested Capital (ROIC) of 29.21%, doing better than 99% of its industry counterparts. Importantly, this ROIC is much higher than its cost of capital, proving the company is building real shareholder value.

- Growing Margins: Its Profit Margin of 33.73% and Operating Margin of 38.48% are higher than about 97% of the industry. Notably, these margins have gotten better in recent years, pointing to capable management and pricing ability for its sold products.

- Steady Cash Production: The analysis mentions positive earnings and operating cash flow not just in the last year but steadily over the past five years, showing the lasting nature of its earnings.

For a value investor, this degree of earnings confirms the business model and implies that present earnings are not a temporary event but the outcome of a lasting competitive edge, in this instance, its effective cancer treatments.

Expansion: A Maintainable Path

While pure value stocks occasionally miss expansion, the best candidate mixes value with a forward direction. Exelixis has a good Expansion grade of 6, showing an acceptable, if not dramatic, expansion picture that backs its valuation.

- Good Past EPS Expansion: Earnings Per Share has expanded at a notable average yearly rate of 51.25% over recent years, with a 49.73% jump in the past year alone.

- Future Predictions: Analysts think this expansion will persist, though at a more controlled, maintainable speed. EPS is forecast to expand by about 15.92% yearly in the next few years.

- Sales Base: While future sales expansion is predicted to be more limited (around 7.52%), it adds to a past average expansion rate of over 18%.

This expansion picture is key because it suggests the company's true worth is probably rising over time. A value investor is not just buying a fixed asset at a discount but a growing business whose reduced price may become even more appealing as its earnings increase.

Conclusion

Exelixis shows a situation where a systematic filtering approach has found a possible mismatch. The company sells at valuation levels much lower than its industry, yet it functions with a balance sheet free of debt, notable earnings numbers, and a record of strong expansion that is anticipated to continue. This mix, a low price joined with high-caliber basics, is exactly what methods like the "Decent Value" filter aim to discover. It matches the value investing rule of looking for a "margin of safety," where the company's financial condition and earnings ability give a buffer against the unknowns present in any stock investment.

For investors wanting to see the complete basic analysis that backs this assessment, you can locate the full report here: Fundamental Analysis of EXELIXIS INC.

If the picture of Exelixis fits your investment approach, you can use similar standards to look for other possible chances. Our stock filter can help you find more companies that match these "Decent Value" conditions. Click here to view the filter and see more results.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a bid or request to buy or sell any securities. The analysis uses given information and shows the author's view. Investing in stocks includes risk, including the possible loss of the original amount. You should do your own complete research and talk with a qualified financial consultant before making any investment choices. Past results do not show future outcomes.