For investors looking for dependable income, a methodical screening process can aid in finding companies that provide more than a high stated yield. A frequent method uses filters for stocks that join a good dividend history with firm basic business strength and earnings. This method emphasizes longevity, searching for companies that not only give dividends now but are also in a fiscal state to keep and possibly raise those payments in the future. By concentrating on basic scores for dividend caliber, earnings, and fiscal strength, investors can sort through the market to locate businesses constructed to endure economic shifts and benefit shareholders steadily.

EnerSys (NYSE:ENS), a worldwide top provider in stored energy solutions for industrial uses, appears as a notable candidate from this kind of screening method. The company’s basic report shows a history that matches well with the standards of dividend longevity backed by firm operating and fiscal bases.

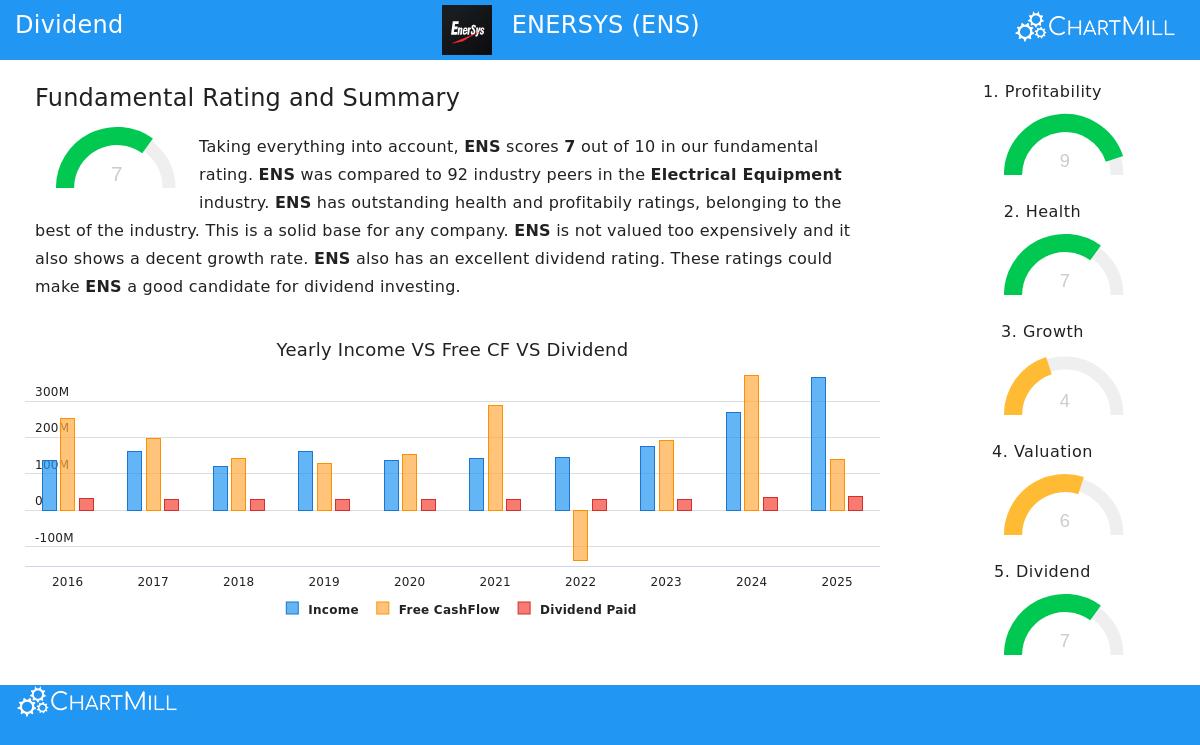

A Look at Dividend Longevity

For dividend investors, the caliber and steadiness of the payment are frequently more important than the simple amount of the yield. EnerSys’s dividend history, which receives a firm ChartMill Dividend Rating of 7 out of 10, is formed on a past of steadiness and careful management.

- Steady History: The company has paid and, notably, has not reduced its dividend for at least ten years. This lasting dedication offers a degree of predictability that income-seeking investors appreciate.

- Lasting Payout Ratio: A central measure for dividend strength is the payout ratio, which calculates the part of earnings given as dividends. EnerSys pays out only 12.14% of its earnings, a very cautious level that leaves plenty of room to put money back into the business and soften against possible earnings changes. This low ratio is a firm sign that the present dividend is not in danger.

- Increase-Focused: Beyond simple keeping, EnerSys has raised its dividend at an average yearly rate of 6.15% over recent years. Also, its earnings are rising at a quicker rate than its dividend, indicating this increase path is lasting and not pressuring the company’s finances.

While its present dividend yield of 0.58% is moderate next to the wider S&P 500, it is meaningful within the setting of its field. EnerSys’s yield is much higher than the average for the Electrical Equipment sector, putting it in the leading group of dividend payers next to its peers. This points out a company giving back a competitive part of its earnings to shareholders within a competitive field.

The Base: Earnings and Fiscal Strength

A lasting dividend must be backed by a profitable and fiscally stable business. This is why screening for adequate earnings and strength scores is a key part of the method; a high yield is unimportant if the company behind it is facing difficulties. EnerSys does very well in these basic areas, getting a top-level Earnings Rating of 9 and a firm Strength Rating of 7.

The company’s earnings measures are especially firm:

- It shows very good returns on its capital, with a Return on Invested Capital (ROIC) of 13.13% that does better than over 92% of its field competitors.

- Its profit margin of 8.37% and operating margin of 12.66% are also with the best in the sector and have shown upward movements in recent years.

From a fiscal strength view, EnerSys shows a stable image:

- The company has a firm current ratio of 2.75, showing more than enough short-term assets to meet its near-term debts.

- Its debt amounts, shown in a Debt-to-Equity ratio of 0.61, are workable and match field standards. More importantly, its Debt to Free Cash Flow ratio of 2.67 is very good, suggesting it could pay off all its debt in under three years using its cash flow, which offers a major safety buffer.

Worth and Increase Setting

EnerSys seems fairly valued relative to both its own earnings potential and its field. With a Price-to-Earnings (P/E) ratio of 16.69 and a forward P/E of 14.63, the stock is valued lower than about 90% of its field peers and is under the present average for the S&P 500. This worth, when joined with its high earnings, indicates the market may not be completely valuing the company’s quality and stability.

Increase is moderate, with earnings per share expected to rise about 8.75% yearly in the coming years. For a dividend-focused method, this level of increase is often enough, as it backs the possibility for continued dividend raises without needing the forceful, and often riskier, expansion looked for in pure increase investing.

A Candidate for More Study

EnerSys stands for the kind of company a methodical dividend screening process tries to find: one with a steady and rising dividend based on outstanding earnings and stable fiscal strength. Its moderate yield is balanced by a very lasting payout and a firm competitive place within its field. Investors can look at the complete study in the full EnerSys basic report for a more detailed look into all the measures talked about.

For those wanting to look into other companies that meet similar standards of high dividend caliber, firm earnings, and good fiscal strength, the Best Dividend Stocks screen offers a changing beginning point for more study.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a deal to buy or sell any securities. The study is based on data and scores given by ChartMill, which can change. Investors should do their own complete study and think about their personal fiscal situations and risk comfort before making any investment choices.