Investors looking for expansion chances at fair prices frequently use methods that find firms with good development potential that are not yet too expensive according to the market. The Affordable Growth method focuses on stocks showing good expansion paths while keeping solid basic financial health and profit measures, all at prices that do not demand high costs. This system mixes the search for development with careful money management, looking for firms that join several positive traits instead of being strong in only a single part.

Growth Path

EMCOR GROUP INC (NYSE:EME) shows the kind of expansion pattern that affordable growth investors usually look for. The firm's recent results display notable development in important financial numbers, with especially good outcomes in profit growth. The basic financial review shows a number of good expansion signs:

- Earnings Per Share has increased by 26.31% over the last year

- Past EPS growth averages 30.23% each year over recent years

- Revenue went up by 14.11% in the last year with a 9.69% average yearly growth rate

- Future EPS growth is estimated at 12.63% each year

- Revenue growth is anticipated to keep going at 9.09% each year

These expansion numbers point to a firm that has shown good past development while keeping positive future growth forecasts. The steadiness between past results and future estimates gives assurance that the expansion narrative is still valid, which is important for investors looking for lasting development rather than short-term jumps.

Price Assessment

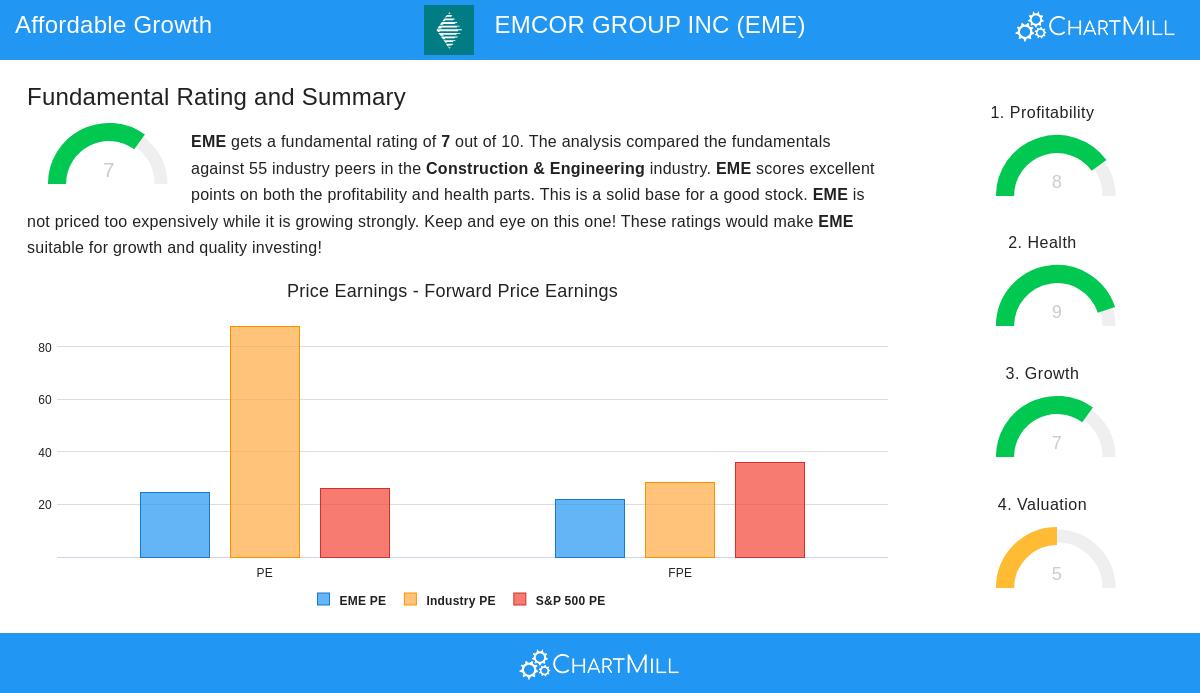

The price situation for EMCOR shows a noteworthy case where standard measures could at first imply high costs, but the full picture shows a more detailed story. While the firm's Price/Earnings number of 24.56 might seem high on its own, several elements support this multiple within the affordable growth structure:

- The P/E number is less expensive than 74.55% of similar industry firms

- Forward P/E of 21.77 looks good next to the S&P500 average of 36.12

- Enterprise Value to EBITDA shows a cheaper price than 69.09% of industry rivals

- Price/Free Cash Flow number is more appealing than 72.73% of industry peers

- The PEG number, which includes growth, implies a suitable price

For affordable growth investors, these price measures show that while EMCOR is not very cheap, it stays fairly priced considering its growth outlook and industry standing. The firm's price becomes more interesting when viewed next to its growth speed and profit-making ability.

Profit-Making and Money Strength

Beyond expansion and price, EMCOR is strong in the basic areas that affordable growth investors focus on for risk control. The firm's profit measures are particularly good, with Return on Equity at 33.89% and Return on Invested Capital at 27.41%, both placed in the high group of industry peers. Profit margins have shown steady gain, with operating margin getting to 9.41% and profit margin at 6.96%.

The money strength score of 9/10 highlights the firm's steadiness, with several notable positive points:

- Altman-Z score of 6.58 shows very low failure risk

- Very small debt with Debt/Equity number of 0.00

- Debt to Free Cash Flow number of 0.01 shows good ability to pay debts

- Steady positive profits and cash flow over five years

- Share number decrease through repurchases

These health and profit-making measures supply the safety buffer that affordable growth investors need, making sure the firm's growth is not reached through too much borrowing or financial tricks.

Investment Points

For investors using the affordable growth plan, EMCOR stands for an interesting case where several basic elements line up. The firm's good expansion profile is backed by excellent profit-making and very good money strength, making a base for lasting development. The price, while not very low, seems acceptable considering the quality of the business and its growth outlook.

The firm's place in electrical and mechanical construction services gives contact to infrastructure and industrial markets, areas that keep seeing continuous spending. With work covering business, technology, factory, and health clients through about 100 smaller companies, EMCOR gains from varied income sources while keeping operational attention.

View more affordable growth stock options using our preset filter

This article gives basic financial study for information only and is not investment guidance, a suggestion, or support for any security. Investors should do their own study and talk with money advisors before making investment choices. Past results do not ensure future outcomes, and all investments have risk including possible loss of the original amount.