For investors looking for dependable income, a methodical selection process can find companies that provide not only a high dividend yield, but one that can be maintained. A typical plan involves selecting for stocks with a good total dividend profile, supported by acceptable financial condition and earnings. This method tries to sidestep the risk of high yields that frequently signal a troubled stock price and a dividend that may not last. One stock that appears from this type of selection is the utility company Consolidated Edison Inc (NYSE:ED).

A Look at Dividend Longevity

The center of this investment technique is the ChartMill Dividend Rating, a combined score that assesses a company's dividend using its yield, history of increases, and payment longevity. By requiring a high score here, the selection favors quality over yield alone. Yet, a solid dividend is only as reliable as the firm that issues it. This is why additional filters for minimum earnings and condition ratings are important. They confirm the company has the profit to continue its dividend and a financial position stable enough to endure economic shifts, creating a more reliable income source for the patient investor.

Examining Consolidated Edison's Dividend Attraction

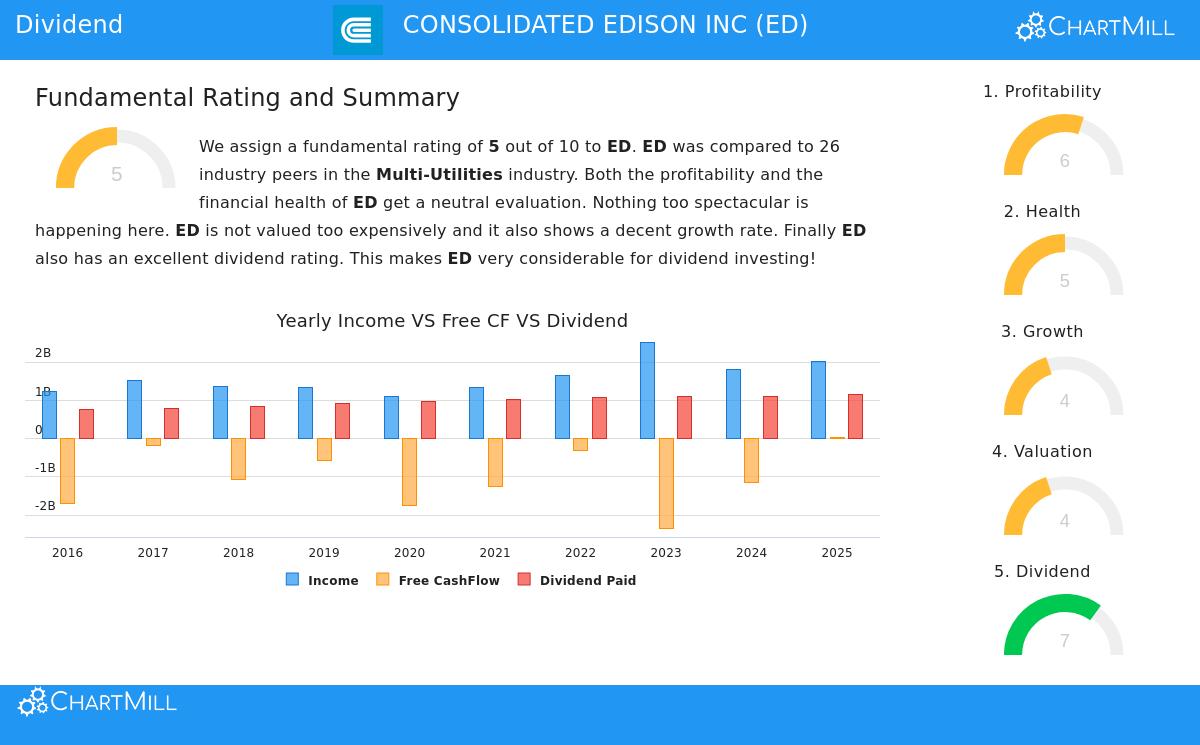

Consolidated Edison receives a Dividend Rating of 7 out of 10, putting it in the high group of dividend-paying stocks by this measure. A detailed review of the fundamental analysis report shows the parts creating this score.

- Yield and History: ED provides a dividend yield of 3.18%, which is notable next to the S&P 500 average near 1.89%. Significantly, the company has a very dependable history, having paid and raised its dividend for at least ten straight years. This record of consistency is a major sign of management's focus on giving capital to shareholders.

- Payment Longevity: The dividend's longevity is judged by the payout ratio, which indicates the share of profits paid as dividends. ED's payout ratio is 57.67%. Although this is elevated, it is usually seen as acceptable, particularly for a steady utility company. The report states that profits are rising quicker than the dividend, which backs the idea that the present payment level can be maintained.

- Small but Consistent Increase: The yearly dividend increase rate is a small 2.66%. For investors centered on income, regularity often outweighs fast increase. This gradual rise assists in protecting income from inflation and mirrors the regulated, steady character of the utility business.

Supporting Basics: Earnings and Condition

A solid dividend cannot stand alone; it needs a base of business strength. ED's supporting ratings give this background.

- Earnings Rating (6/10): The company shows steady earnings with positive profits and cash flow in every one of the last five years. Important margins are varied, with a good Gross Margin beating most industry competitors, while the Operating Margin faces challenges. In total, the company produces enough returns to maintain its operations and its dividend payments.

- Condition Rating (5/10): The financial condition score is middling, offering a detailed view. In one aspect, liquidity measures like the Current and Quick ratios are very good compared to the utility industry. In another, the company holds a large debt load, which is common for utilities that require major investment. The report points out that ED's debt levels are actually more favorable than many competitors, and its ability to cover debt has gotten better from the prior year. This indicates the company is handling its financial setup suitably within its sector's standards.

Price and Increase Background

With a Price Rating of 4 and an Increase Rating of 4, ED is not a bargain-price or fast-increase story. Its Price-to-Earnings ratio is about average for the utility industry. Increase in profits and sales is projected to persist at a slow, single-digit rate. For a dividend investor, this is frequently a suitable exchange: the main aim is safe income, not large price gains. The steady, regulated income of a utility offers a predictable setting for that income.

A Prospect for Income Portfolios

Consolidated Edison Inc makes a strong argument for dividend investors who value reliability and longevity. It results from a strict selection because it joins a reasonable yield with a long record of consistent payments, backed by sufficient earnings and a sector-suitable financial setup. It shows the kind of company that can act as a foundation in a portfolio designed for income.

This review of ED began from an organized selection for good dividend payers. Investors can see the complete list of matching stocks and change the rules to their own preferences by going to the Best Dividend Stocks screen.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on historical data and analyst estimates, which are not guarantees of future performance. Investors should conduct their own research and consider their individual financial circumstances before making any investment decisions.