The investment philosophy of Peter Lynch, the legendary manager of Fidelity's Magellan Fund, is built on a simple yet strong premise: individual investors can outperform the pros by focusing on what they know and identifying well-run companies trading at reasonable prices. His strategy, often categorized as Growth at a Reasonable Price (GARP), emphasizes sustainable earnings growth, strong financial health, and sensible valuation. It is a disciplined method that avoids speculative manias, instead seeking businesses that can compound value over a decade or more. A recent screen based on Lynch’s main criteria has identified one such candidate for further study: DRDGOLD LTD-SPONSORED ADR (NYSE:DRD).

A Lynchian Profile: Sustainable Growth and Financial Prudence

Peter Lynch’s framework filters for companies with a specific growth profile and a strong balance sheet. DRDGOLD, a South African company specializing in the retreatment of surface gold tailings, appears to fit several of these key principles. The screen’s main filters target companies with a history of consistent, manageable growth, reasonable valuation relative to that growth, and low financial risk.

- Sustainable Earnings Growth: Lynch preferred companies growing earnings per share (EPS) between 15% and 30% annually over a five-year period, seeing this range as sustainable. DRDGOLD’s five-year EPS growth rate of approximately 26.1% sits within this target zone, indicating a solid and steady increase of profitability without the concerns of extreme growth that can be hard to maintain.

- Attractive Valuation via the PEG Ratio: The Price/Earnings to Growth (PEG) ratio is a central part of the Lynch method, as it contextualizes a stock’s price relative to its growth rate. A PEG ratio at or below 1.0 suggests a stock may be reasonably priced or even undervalued given its growth path. DRDGOLD’s PEG ratio, based on its past five-year growth, stands at an attractive 0.49, well below the threshold. This signals the market may not be fully valuing the company’s historical growth performance.

- Exceptional Financial Health: Lynch was cautious of high debt. His screen requires a Debt-to-Equity ratio below 0.6, with a preference for figures even lower. DRDGOLD performs well here, reporting a very small Debt/Equity ratio of approximately 0.0007, meaning an almost debt-free capital structure. This offers significant operational flexibility and lowers risk during economic downturns. Also, the company’s Current Ratio of 3.01 is much higher than the screen’s requirement of 1.0, showing more than enough liquidity to cover short-term obligations.

- High Profitability: A minimum Return on Equity (ROE) of 15% ensures that a company is generating good profits from shareholder investments. DRDGOLD’s ROE of 29.7% not only meets this standard but places it near the top of its industry, reflecting efficient management and a possibly lasting competitive edge in its area of gold recovery.

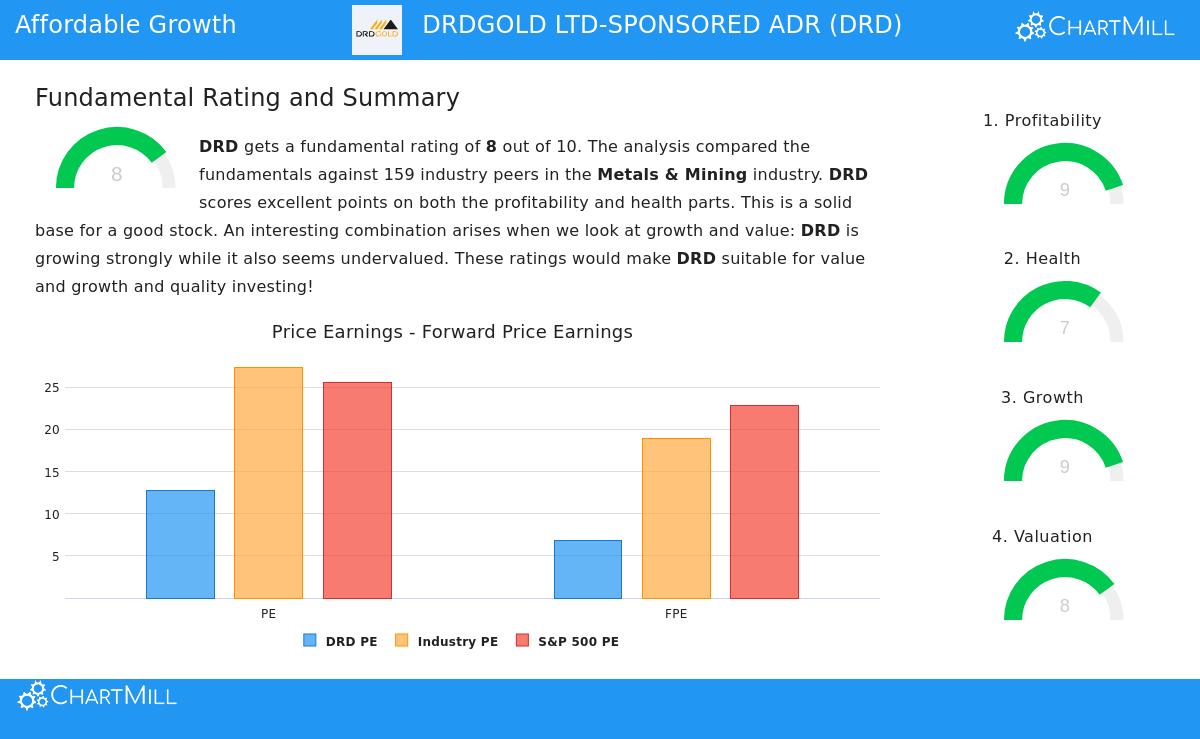

Fundamental Analysis Overview

A detailed fundamental analysis report for DRDGOLD gives the company a high overall score of 8 out of 10, supporting the initial screen results. The report points out several key strengths that long-term investors should consider.

- Profitability is a major strength, with high ratings for margins and returns. The company’s Profit Margin of 35.1% and Return on Invested Capital (ROIC) of 21.6% are some of the best in the Metals & Mining industry.

- Financial health is strong. The company’s solvency and liquidity are rated highly, supported by the very low debt level and solid current ratio already noted. The analysis states the company has no issue meeting its short-term obligations.

- Valuation appears attractive. The report finds DRDGOLD seems undervalued, particularly when looking at forward earnings estimates. Its Price/Earnings and Price/Forward Earnings ratios are low compared to both industry peers and the broader S&P 500.

- Growth is solid and increasing. Both past and expected future growth rates for Revenue and EPS are notable. Specifically, the expected future EPS growth rate of over 45% suggests analysts see progress continuing.

You can review the full fundamental breakdown here: DRDGOLD Fundamental Analysis Report.

Considerations for the Long-Term Investor

While the quantitative filters create an attractive picture, Lynch’s strategy needs qualitative understanding. Investors should study DRDGOLD’s business model completely. The company’s results are linked to the price of gold, introducing a commodity-based volatility that must be understood and accepted. Also, as a South African company, it works within a specific geopolitical and regulatory setting. The fundamental report notes a decreasing dividend history, which may be a point for income-focused investors, though the payout ratio remains manageable. The core of the Lynch method is to find a well-managed company in a workable business, even a "simple" one like tailings retreatment, that is financially stable and bought at a reasonable price, letting the growth build over many years.

Finding More Candidates

DRDGOLD represents one present example that meets a strict set of Lynch-based filters. Investors interested in using this disciplined GARP method to find other possible candidates can examine the screen on their own. You can view and adjust the live Peter Lynch strategy screen here: Peter Lynch Stock Screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investing involves risk, including the potential loss of principal. Always conduct your own thorough research and consider consulting with a qualified financial advisor before making any investment decisions.