For investors looking to balance the search for growth with prudence, the "Affordable Growth" or "Growth at a Reasonable Price" (GARP) method offers a practical middle ground. This method tries to find companies that are increasing their revenues and earnings at an attractive rate but are also priced at levels that do not assume flawless execution. By filtering for stocks with good growth scores, sound basic profitability and financial condition, and a price that is not too high, investors can search for chances where the market may not have completely recognized a company's prospects. Doximity Inc-Class A (NYSE:DOCS), a digital platform for medical professionals, recently appeared in such a filter, justifying a more detailed examination of its basic profile.

Growth Path and Momentum

The central idea of any growth method is finding companies with a strong and lasting expansion driver. Doximity’s basic report notes a solid growth profile, receiving a ChartMill Growth Rating of 8 out of 10. The company shows notable momentum across important financial measures.

- Historical Performance: Over the last few years, Doximity has produced outstanding growth. Revenue has increased at an average yearly rate of 37.42%, while Earnings Per Share (EPS) has risen by an average of 79.21% per year.

- Recent Performance: This momentum is not only historical. In the last year, revenue rose by 15.92%, and EPS increased by 28.91%, showing the company's main business continues to grow in a healthy way.

- Future Projections: Looking forward, analysts forecast continued good growth, with estimates indicating yearly revenue growth of 11.82% and EPS growth of 11.76%. While this shows a slowdown from the very high rates of the past, it signals a shift to a still-good, lasting growth stage.

For an affordable growth method, this mix is important: a confirmed history of high growth gives trust in the business model, while a future view that stays positive implies the opportunity remains, even if the pace is a bit slower.

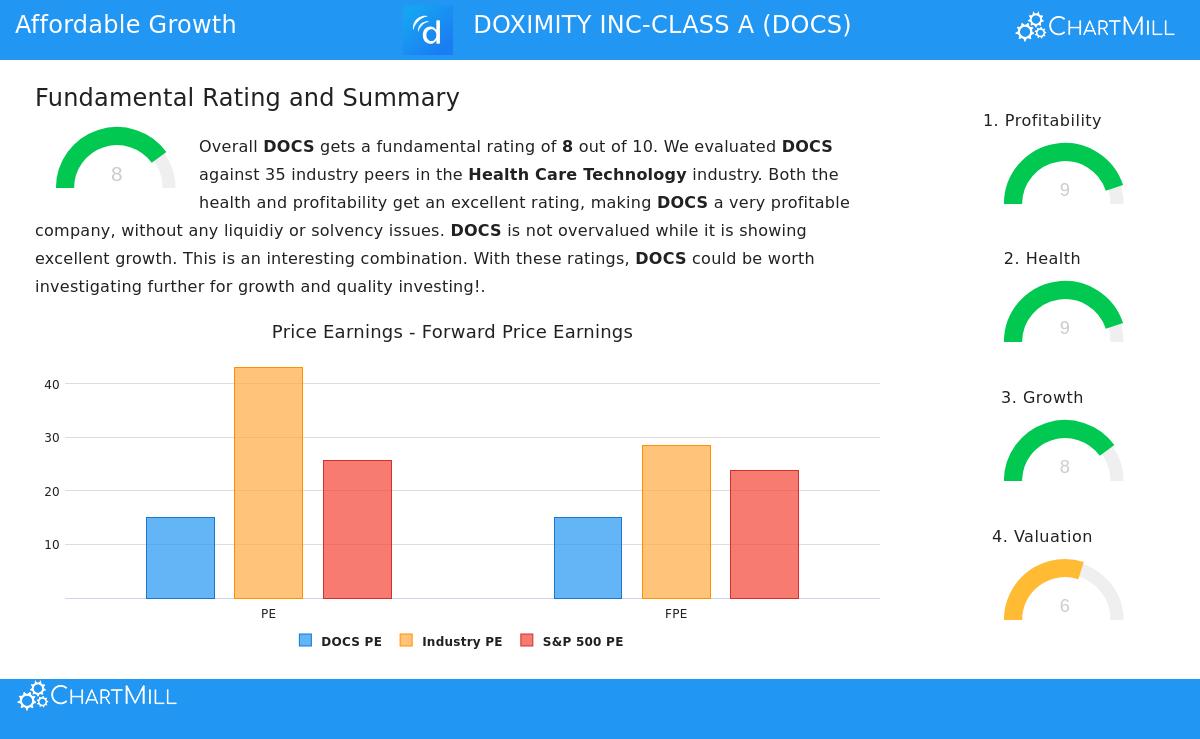

Valuation: Sensible in Context

A stock can show excellent growth but still be a bad investment if its price already accounts for many years of future achievement. The affordable growth filter specifically looks for stocks that are "not overvalued," and Doximity’s Valuation Rating of 6 implies it is in a sensible range, particularly when compared to its industry and its own quality.

- Sensible Multiples: Doximity trades with a Price-to-Earnings (P/E) ratio of 15.03 and a Forward P/E of 14.94. Both numbers are significantly lower than the wider S&P 500 averages (25.73 and 23.72, respectively).

- Industry Comparison: The valuation becomes more interesting within its own sector. Doximity is priced lower than about 83% of similar companies in the Health Care Technology industry based on its P/E ratio, and lower than 80% based on its Forward P/E.

- Quality Reason: It is important to state that low multiples by themselves are not a positive if the basic business is poor. In Doximity’s situation, the sensible valuation is combined with very good profitability, which can support a higher price. The filter’s need for adequate profitability makes sure the valuation is judged next to the quality of earnings, not alone.

This valuation view is key to the GARP argument. It implies the market may be using a general technology discount or not fully recognizing the durability of Doximity's earnings, providing a possible opportunity before the growth narrative is completely understood.

Basic Strength: Profitability and Financial Condition

An affordable growth method must look past the top-line growth and main valuation numbers. The financial base of the company is what lets growth continue and limits the downside. Doximity is strong here, with a Profitability Rating of 9 and a Financial Health Rating of 9.

The company’s profitability measures are very good, often placed at the highest level of its industry.

- It has a Profit Margin of 37.54% and an Operating Margin of 37.44%, doing better than 100% of its industry peers.

- Returns on capital are also very good, with a Return on Invested Capital (ROIC) of 19.48%, showing very efficient use of shareholder capital.

From a condition perspective, Doximity shows a very clear balance sheet.

- The company has no debt, removing solvency risk and interest cost pressures.

- It keeps high liquidity, with a Current Ratio and Quick Ratio of 6.63, giving plenty of buffer to manage any near-term issues or put money into new projects.

These high scores in profitability and condition are not just extra details; they are essential to the affordable growth point. They lower the risk linked to investing in a growth company and provide the financial ability to pay for future expansion from within, making the forecasted growth more believable and lasting.

Conclusion and Next Steps

Doximity Inc. presents an interesting example for the affordable growth investment method. It combines a good, clear growth path—both historical and projected—with a valuation that seems sensible compared to the wider market and its own high-margin, financially sound industry group. The company’s very good profitability and clean, debt-free balance sheet provide a solid base that supports its growth story and reduces investment risk.

This examination is based on Doximity’s full fundamental report, which gives a detailed look at all basic measures. For investors wanting to find other companies that match this careful growth-at-a-reasonable-price profile, the specific filter that found DOCS can be viewed and changed here: View the Affordable Growth Stock Screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented should not be used as the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.