For investors aiming to assemble a portfolio of lasting, superior businesses, the ideas of quality investing offer a useful structure. This method centers on finding companies with lasting competitive strengths, sound financial condition, reliable earnings, and capable leadership, characteristics that let them increase value over many years. An organized method to start this hunt is with a stock screener based on measurable quality measures. One example is the "Caviar Cruise" screen, which selects for firms displaying better past results in sales and earnings increase, high returns on capital put to work, sound cash flow generation, and an acceptable level of debt.

The Walt Disney Co. (NYSE:DIS) appears as a candidate from this screening method, deserving more examination by investors focused on quality. The company's wide holdings across television networks, subscription video services, amusement parks, and merchandise forms a distinct assembly of famous brands and creative assets.

Performance and Earnings Increase

A central idea of quality investing is the search for companies that have shown they can increase not only sales, but, more critically, their basic earnings. The Caviar Cruise screen demands at least 5% yearly increase in both sales and EBIT (Earnings Before Interest and Taxes) over five years. EBIT is an important measure here, as it concentrates on central operational earnings, removing the influence of financing and tax rates to permit a clearer evaluation.

Disney's past numbers show a detailed account:

- Sales Increase (5Y CAGR): 3.78% – This is a little under the screen's 5% limit, showing the company's very large size and the business interruptions encountered by its parks and movie divisions in recent periods.

- EBIT Increase (5Y CAGR): 29.53% – Importantly, Disney's EBIT increase is much greater than its sales increase. This points to strong operating leverage and better earnings, a signal that the company can turn additional sales into even larger profits, a trait of quality often fueled by pricing ability or scale benefits.

Return on Capital and Financial Effectiveness

Maybe the most important filter in a quality screen is the Return on Invested Capital (ROIC). A high ROIC shows that leadership is skilled at directing capital to produce profitable increase. The Caviar Cruise screen uses a strict version (ROIC leaving out cash, goodwill, and intangibles) and sets a high mark at 15%.

- ROIC (Excluding Cash, Goodwill & Intangibles): 24.11% Disney's result here is very good, easily passing the requirement. This implies that the capital put into the central business, from park upgrades to content creation for streaming, is producing sound returns. For a quality investor, a maintainably high ROIC is a main sign of a lasting competitive strength.

Cash Flow Soundness and Debt Condition

Quality companies produce sufficient free cash flow (FCF), which gives financial room for dividends, stock buybacks, new investment, or lowering debt. The screen assesses both the soundness of earnings and the balance sheet.

- Earnings Soundness (5Y Avg.): 119.01% – This measure, which compares free cash flow to net income, is excellent. A number over 100% indicates Disney has turned more than 100% of its accounting profits into actual cash over the past five years, pointing to very high earnings quality and effective management of working capital.

- Debt-to-Free Cash Flow: 4.17 – This ratio shows it would take about 4.2 years of current FCF to pay off all existing debt. It rests acceptably below the screen's limit of 5, indicating a tolerable debt amount compared to the company's sound cash-producing capacity.

Fundamental Analysis Summary

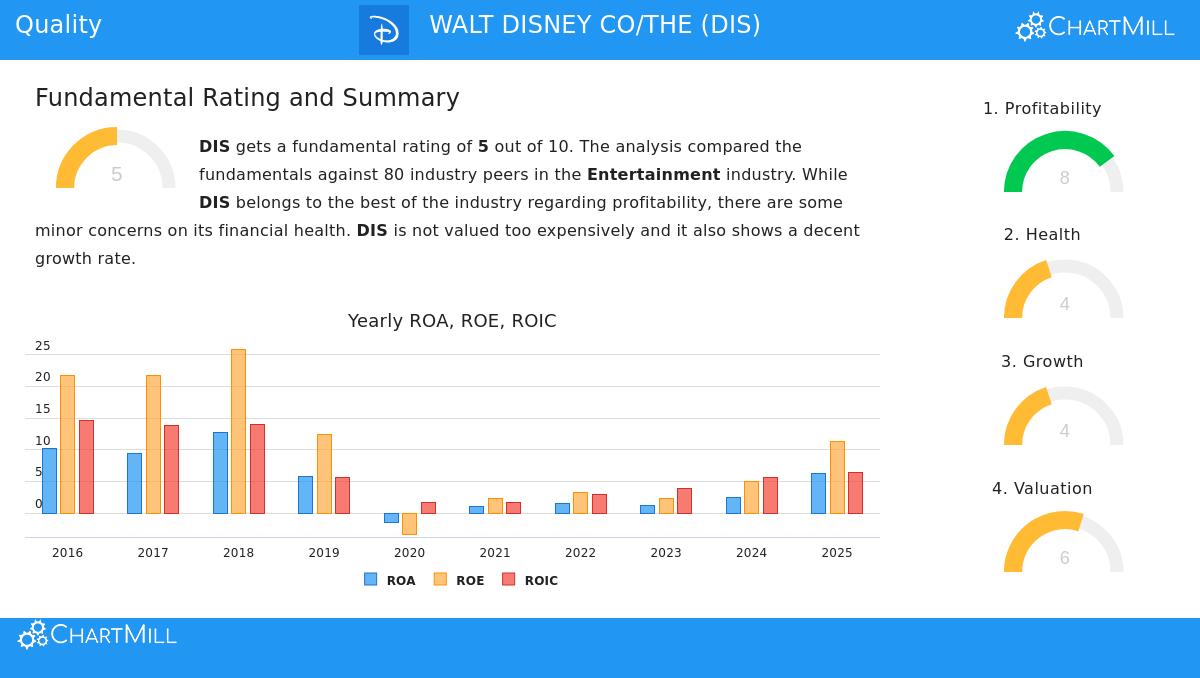

An inspection of Disney's detailed fundamental report gives a wider view. The report gives DIS a fundamental score of 5 out of 10, noting positive areas and difficulties.

- Positive Areas: The company rates well on Earnings Power (8/10), with top-level operating and profit margins that have gotten better. Its price seems fair compared to both the overall market and its industry group, receiving a Valuation score of 6/10.

- Points to Note: The report notes some points in Financial Condition (4/10), mainly connected to near-term liquidity ratios, although its long-term stability measures like Debt-to-Equity are sound. Increase (4/10) is seen as average, with good past EPS increase but more limited forecasts for coming periods.

Is Disney a Quality Investment Candidate?

Judging by the measurable filters of the Caviar Cruise screen, The Walt Disney Co. makes a solid argument for quality investors. It does very well in the most important areas: producing a high return on capital put to work and turning profits into significant free cash flow. Its notable EBIT increase shows better operational effectiveness. While its recent sales increase has been slowed by industry changes and broader economic conditions, its unmatched set of brands, worldwide presence, and shift to direct customer relationships fit the non-measurable parts of quality investing, like lasting competitive strengths and pricing ability.

The screen that found Disney can be a first step for more study. You can review other companies that meet these strict quality filters by using the Caviar Cruise stock screener.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of the original amount invested. You should perform your own research and talk with a qualified financial consultant before making any investment choices.