For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, maintainable growth, and good finances, all bought at a fair price. This "growth at a reasonable price" (GARP) idea steers clear of speculative manias by requiring both quality and value. A stock filter based on Lynch’s rules can find companies that satisfy these strict standards, and one such company that recently appeared is DHT Holdings Inc (NYSE:DHT).

A Lynch-Style Match: Main Filtering Standards

The Peter Lynch filter looks for companies with a particular financial shape: solid but not extreme past earnings growth, high profitability, good financial condition, and a pleasing price when growth is considered. DHT Holdings, an owner and operator of Very Large Crude Carrier (VLCC) tankers, seems to match these central ideas. Let's review how the company measures up against the main Lynch measures.

- Maintainable Earnings Growth: Lynch preferred companies with a demonstrated history of growth, but was cautious of extreme growth that could not continue. The filter needs a 5-year earnings per share (EPS) growth rate between 15% and 30%. DHT's EPS has increased at an average yearly rate of 16.14% over this time, firmly inside the target zone and pointing to a consistent, maintainable rise in profitability.

- Price Justified by Growth: Maybe the central part of the Lynch method is the Price/Earnings to Growth (PEG) ratio. A PEG ratio at or under 1.0 implies the stock's price is fair compared to its earnings growth. DHT's PEG ratio, calculated from its past five-year growth, is 0.82, signaling the market might be pricing its historical growth path too low.

- High Profitability: Return on Equity (ROE) shows how well a company produces profits from shareholder equity. Lynch searched for high profitability, with a minimum ROE of 15%. DHT's ROE of 18.25% not only meets this but also puts it in the best group of its industry, doing better than 85% of similar companies.

- Careful Financial Condition: Lynch stressed investing in companies with good balance sheets to endure economic slumps. Two key filters are the Debt/Equity ratio (ideally below 0.6, with Lynch himself liking under 0.25) and the Current Ratio (above 1.0). DHT does very well here, with a Debt/Equity ratio of 0.22 and a solid Current Ratio of 2.41. This shows very little financial borrowing and enough cash to meet near-term debts.

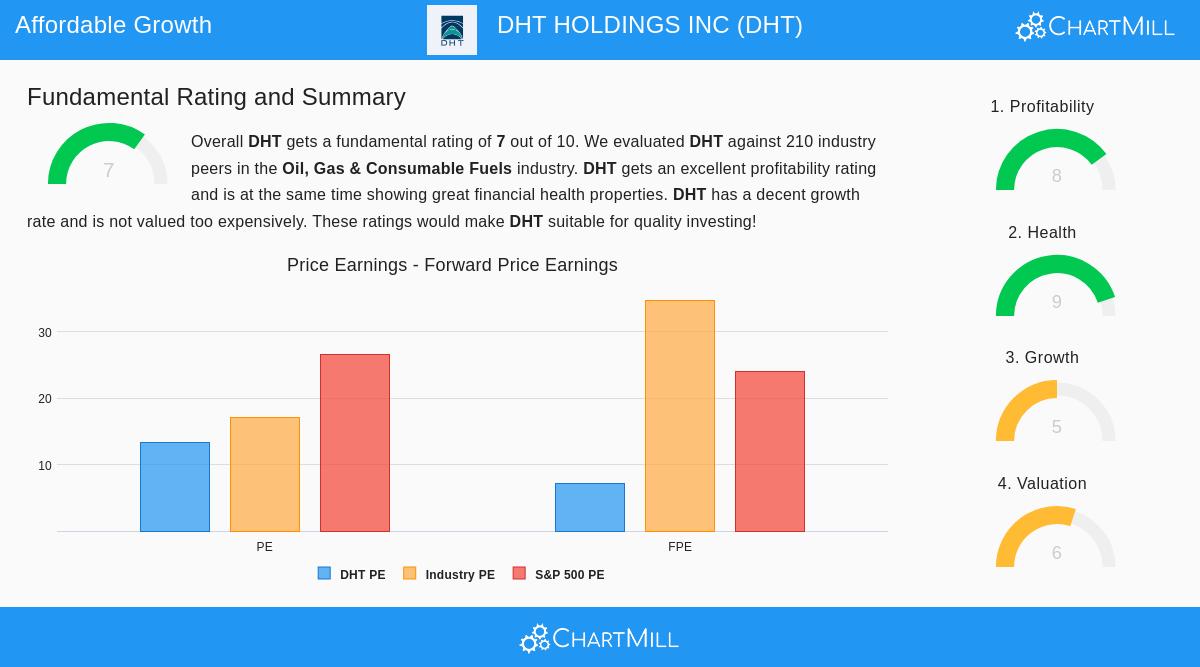

Fundamental Condition Review: More Than the Filter

While the filter gives a good beginning point, Lynch told investors to look more closely. An examination of DHT's full fundamental analysis report gives a more detailed view. The company gets a good total fundamental score of 7 out of 10, supported by high marks in Profitability (8/10) and Financial Condition (9/10).

Its profit margins lead the industry, and its balance sheet soundness, shown by low debt and high cash ratios, is a major plus. The Valuation (6/10) is seen as fair, with a forward P/E ratio that appears inexpensive next to both the industry and the wider market. The primary points of attention are in Growth (5/10), where recent year measures have weakened, and Dividend Stability (6/10), where the high payout ratio causes a question about the long-term path of its appealing yield. You can review the complete, itemized analysis in DHT's fundamental analysis report.

Conclusion: A Subject for More Study

For an investor following the Peter Lynch philosophy, DHT Holdings offers a strong argument for more careful examination. It meets a rigid, formula-based filter centered on maintainable growth, high profitability, financial strength, and fair pricing. The company works in the vital, though fluctuating, global energy transport field, a "simple" industry that Lynch might like for its clear business model. The good balance sheet offers a safety buffer, while the low PEG ratio implies the market has not overvalued its historical growth.

Yet, following Lynch's advice, a filter is just the initial move. The following stage requires knowing the company's business model, its competitive strengths in the tanker market, the prospects for worldwide oil shipping, and the reasons for its recent earnings changes. The filter has found a possible subject; the investor's task is now to study whether DHT is a business they comprehend and trust for the long term.

Interested in finding other companies that match the Peter Lynch investment model? You can use the filter yourself and view the newest outcomes by going to the Peter Lynch Strategy Screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. Investing involves risk, including the potential loss of principal. Always conduct your own research and consider consulting with a qualified financial advisor before making any investment decisions.