For investors aiming to assemble a portfolio of lasting, high-achieving businesses, the quality investing method provides a structured system. This system centers on finding companies with durable competitive strengths, reliable earnings, and sound financial condition, with the plan of owning them for many years. One useful instrument for this hunt is the "Caviar Cruise" stock screen, which uses measurable filters to find firms displaying signs of quality: continued revenue and earnings expansion, elevated returns on invested capital, solid cash flow production, and a reasonable debt level. A present example from this screening method is Cencora Inc (NYSE:COR).

A Portrait in Reliable Performance

Cencora Inc. is a vital part in the worldwide healthcare supply network, offering pharmaceutical sourcing and distribution services. Working through U.S. and International Healthcare Solutions units, the company links manufacturers with a wide network of providers, including hospitals, pharmacies, and clinics. This necessary function in a non-cyclical field offers a base of steadiness. The company's basic results, however, reveal it is not only a steady utility; it displays the expansion and effectiveness traits that quality investors seek.

Matching the Caviar Cruise Standards

The Caviar Cruise screen employs a number of important measures to filter for quality. Cencora's recent financial information displays a solid fit with these central ideas:

-

Continued Expansion: The screen demands at least a 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Cencora easily surpasses this, with a 5-year revenue CAGR of 7.1% and a more notable EBIT CAGR of 13.1%. Importantly, EBIT expansion exceeding revenue expansion, as observed here, is a good sign. It points to better operational effectiveness and possible pricing strength, as the company turns more of each sales dollar into operating profit.

-

Elevated Return on Capital: A main idea of quality investing is evaluating how well management uses shareholder capital. The screen requires a Return on Invested Capital (leaving out cash, goodwill, and intangibles) over 15%. Cencora's result in this measure is unusually high at 4,337.71%. While this remarkable figure needs explanation (it can be affected by a fairly small capital base in this asset-light distribution model), it clearly shows an unusually effective use of the capital that is put into the central business.

-

Solid Cash Flow and Reasonable Debt: Quality businesses produce plenty of cash and are not weighed down by debt. The screen searches for a Debt-to-Free Cash Flow ratio below 5, meaning the company could pay off all debt with fewer than five years of cash flow. Cencora's ratio of 2.2 is safely inside this limit, showing a solid capacity to meet its commitments. Also, the company's 5-year average Profit Quality, which calculates how much net income becomes free cash flow, is a sound 175.46%. This shows Cencora is producing much more cash than its reported earnings imply, offering great room for dividends, share repurchases, or strategic projects.

Basic Analysis Summary

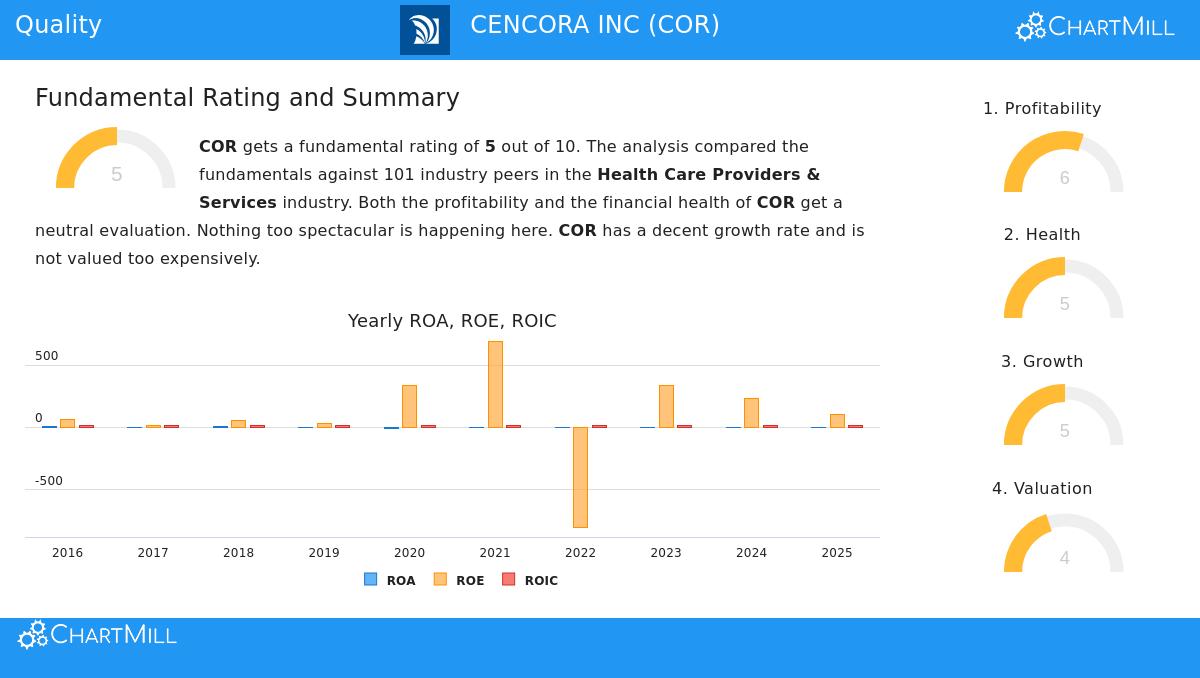

A full basic analysis report for Cencora gives a wider, even-handed perspective. The report gives the stock a middle overall rating of 5 out of 10, showing mixed signs across different groups. On the good side, the report notes the company's very good Return on Equity, quite solid Return on Invested Capital next to industry competitors, and a good financial health position shown by a satisfactory Altman-Z score and the positive Debt-to-FCF ratio. Expansion in Earnings Per Share has also been steady.

The middle rating comes from points of worry or typical results. The company's profit and operating margins are low, which is common for a distribution business, and its liquidity measures (Current and Quick Ratios) are poor, pointing to possible issues in meeting immediate obligations without incoming cash flow. While the stock price looks fair next to both the industry and the wider market, a high PEG ratio implies the market may already be accounting for much of its future expansion.

Investment Points for the Quality Approach

For an investor using a quality plan, Cencora offers a strong argument built on its necessary industry part, reliable expansion path, and excellent capital effectiveness. Its capacity to expand profits quicker than sales and produce significant free cash flow are important quality signs. The extremely high ROIC and solid debt coverage point to a well-run business with a lasting competitive place in the healthcare system.

Still, the quality method also involves examining possible dangers. The poor liquidity ratios and very thin margins need acceptance and ease with the wholesale distribution business model. The company's results are also connected to the wider healthcare environment, including regulatory shifts and pricing forces.

Finding Additional Quality Prospects

Cencora shows the kind of business a structured screening process can find. Investors curious to use the same "Caviar Cruise" method to locate other possible quality holdings can use the screen themselves here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.