The search for undervalued companies is a foundation of value investing, a method that aims to find stocks trading for less than their true worth. This strategy, supported by investors like Benjamin Graham and Warren Buffett, uses detailed fundamental study to find chances where the market price does not match the real value of the business. One organized way to use this idea is by looking for companies that show good fundamental condition and earnings, but are offered at a low price. A "Decent Value" screen does this, selecting for stocks with high valuation scores, meaning they are inexpensive compared to their financial numbers, while still holding acceptable ratings in growth, earnings, and financial condition. This mix tries to find possible deals that are not poor investments, but rather operationally good businesses available at low prices.

Collegium Pharmaceutical Inc (NASDAQ:COLL), a specialty pharmaceutical company that works on creating and selling pain management treatments, recently appeared from this type of screening. With a fundamental rating of 6 out of 10, COLL shows a varied but interesting picture, with its most notable trait being a very low valuation. For value investors, a low buy price compared to earnings and cash flow gives the needed "margin of safety," a protection against mistakes in study or unexpected market declines. COLL's financial information suggests it may provide this protection, deserving more examination from investors using a value-focused plan.

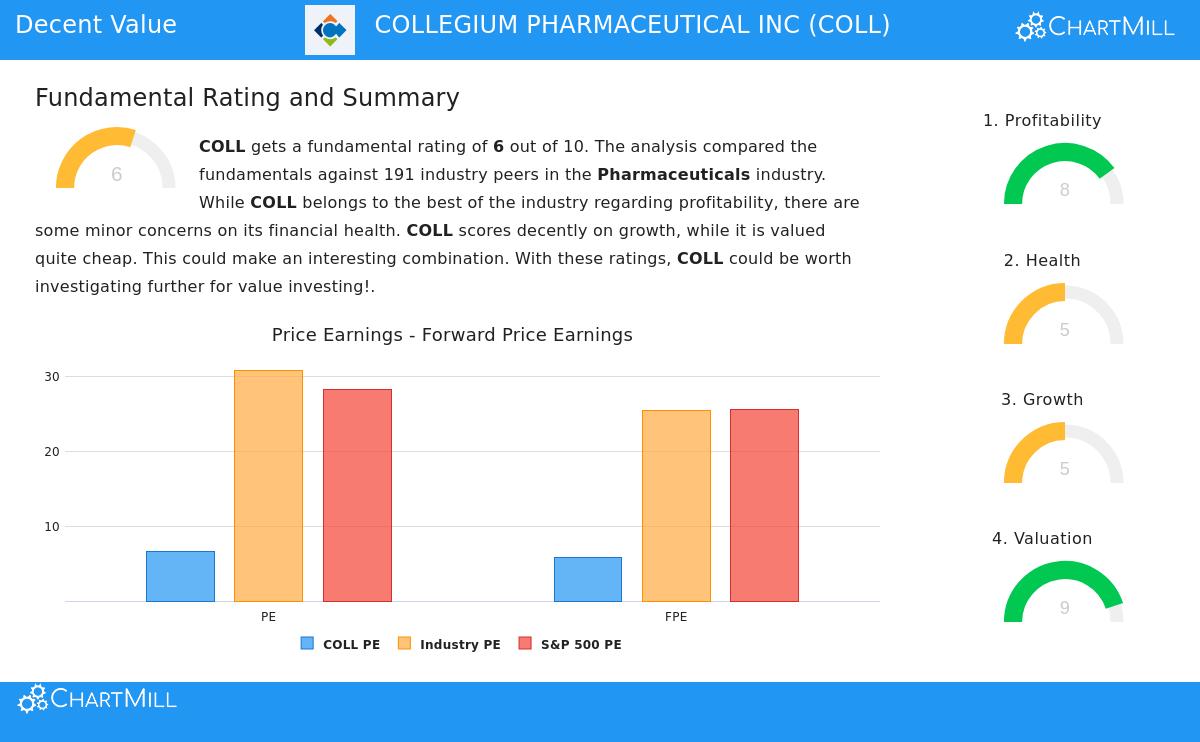

Strong Valuation Numbers

The most noticeable part of Collegium Pharmaceutical's profile is its valuation, which gets a 9 out of 10. This high rating shows the stock is priced very low compared to both its own financial results and similar companies. Important numbers show this clearly:

- Price-to-Earnings (P/E) Ratio: At 6.61, COLL's P/E ratio is much lower than the S&P 500 average of 28.18, and it also puts the company in the least expensive 5% of its pharmaceuticals industry.

- Forward P/E Ratio: An even lower forward P/E of 5.84 means analysts think earnings will stay stable, yet the market still prices the stock at a large discount.

- Enterprise Value to EBITDA & Price/Free Cash Flow: The company also looks inexpensive on these cash-flow measures, trading lower than about 97% and 96% of industry peers, in order.

This group of valuation numbers is key to the value investing argument. A low P/E ratio, especially, can mean the market is pricing a company's earnings below their worth, possibly making a chance for investors if the core business stays healthy.

Evaluating Earnings and Financial Condition

While a low price is attractive, value investors must confirm they are not buying a weakening business. Here, COLL's report shows positives and clear negatives. The company's earnings score is a solid 8 out of 10. It has a very good Return on Equity of 21.27% and a strong Operating Margin of 20.74%, doing better than most of its industry. Steady positive earnings and cash flow over the last five years add support to the quality of its work.

However, the financial condition score is a more average 5 out of 10, showing points for care. The company has a high amount of debt, with a Debt-to-Equity ratio of 2.71, which is poorer than more than 80% of similar companies. This raises financial risk. Balancing this worry is a good Debt-to-Free-Cash-Flow ratio of 2.79, showing the company makes enough cash to handle its debt. Liquidity ratios (Current and Quick Ratio) are sufficient but are in the lower part of the industry. For a value investor, this condition picture highlights the need for the "margin of safety" given by the low valuation; the stock's price may already include these balance sheet risks.

Growth Path and Dividend Practice

COLL's growth rating is a middle 5 out of 10, telling a story of good past results but lower future outlook. The company has produced strong historical growth, with Revenue rising over 16% each year and Earnings Per Share growing over 154% each year on average in recent years. Looking forward, however, analyst projections estimate a small drop in EPS and a much slower rate of revenue growth. This reduction in the growth path is an important item for investors to consider.

Also, COLL does not give a dividend, leading to a dividend score of 0. This means the investment case depends completely on price gains and cannot expect income generation, a point for some value-focused portfolios that look for dividend yield.

Conclusion: A Value Case with Notes

Collegium Pharmaceutical Inc shows a standard value investing situation: a company with good earnings and a shown operational history trading at a large discount to the market and its industry. Its high valuation rating and strong earnings numbers make it a strong candidate for screens looking for undervalued stocks. The large discount may give the margin of safety value investors want, possibly including the known risks linked to its debt-heavy balance sheet and expected growth reduction.

Investors interested in this method can review a wider group of possible chances. More stocks matching this "Decent Value" profile can be found using this pre-configured screen. A complete look at COLL's fundamental study, including all related ratios and peer comparisons, is in its full fundamental report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The study is based on given data and screening methods described. Investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment choices.