The search for quality companies trading at reasonable prices is a foundation of many long-term investment methods. One well-regarded method is the "Growth at a Reasonable Price" (GARP) strategy, made famous by noted investor Peter Lynch. His approach, described in One Up on Wall Street, centers on finding companies with steady earnings growth, good financial condition, and reliable profitability, while also making sure the stock price does not overstate that potential. The aim is to locate reliable long-term holdings for a portfolio, steering clear of the extremes of speculative high-growth stocks and stagnant deep-value investments.

A recent filter using Lynch's main ideas has pointed to Cabot Corp (NYSE:CBT) as a candidate for more examination. The Boston-based global specialty chemicals and performance materials company, which serves markets including tires and automotive, electronics and energy storage, seems to match a number of important Lynch criteria.

Match with Lynch's Main Criteria

Peter Lynch highlighted a balanced group of numerical checks to find well-managed companies with steady prospects. Cabot Corp's present measurements show a good match with several of these rules.

- Steady Earnings Growth: Lynch looked for companies with a demonstrated history of growth, but was cautious of unsustainably high rates. The filter demanded a 5-year average annual EPS growth between 15% and 30%. Cabot's historical growth of 28.5% fits within this target zone, showing a solid past record that is not so extreme as to be unlikely to continue.

- Reasonable Valuation (PEG Ratio): Maybe the most important Lynch measurement is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock in relation to its growth rate. A PEG ratio at or below 1.0 is usually seen as appealing. Cabot's PEG ratio, based on its past five-year growth, is at a very low 0.37. This indicates the market is pricing the company's earnings ability at a notable discount to its historical growth path, a main signal for GARP investors.

- Good Profitability (ROE): Lynch preferred companies that produce high returns on shareholder equity, a sign of effective management and a lasting competitive edge. The filter looked for a Return on Equity (ROE) above 15%. Cabot's ROE of 19.4% easily meets this level, putting it in the high group of its industry for profitability.

- Financial Condition (Debt & Liquidity): A careful balance sheet is important for enduring economic changes. Lynch favored companies financed more by equity than debt. The filter required a Debt-to-Equity ratio below 0.6, and Cabot's ratio of 0.55 satisfies this standard. Also, the company's Current Ratio of 1.67 shows it has enough short-term assets to meet its near-term obligations, passing Lynch's basic financial condition check.

A High-Level Fundamental View

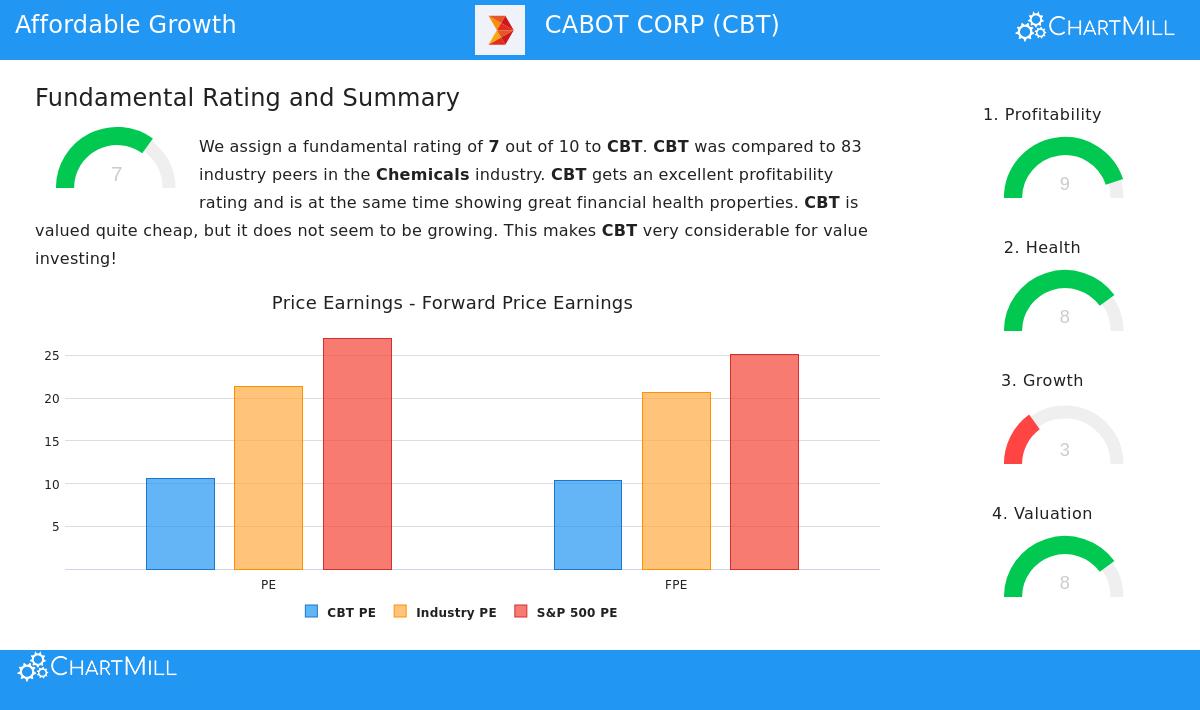

Beyond the specific filter criteria, a wider look at Cabot's fundamental picture supports its position as a possibly sound long-term holding. The company's overall fundamental rating is a good 7 out of 10, with specific strong points that match a value-aware, quality-centered method.

- Profitability is a Main Strong Point: With a score of 9/10, Cabot is very good at turning sales into earnings. Its Return on Invested Capital (ROIC) of 14.8% is with the best in the chemicals industry, showing very efficient use of capital. Both operating and profit margins have gotten better in recent years.

- Valuation Seems Attractive: The valuation rating of 8/10 points out that the stock trades at a discount. Its P/E ratio of 10.7 and forward P/E of 10.4 are much lower than both the industry and the wider S&P 500 averages. This low valuation is placed next to its high profitability, forming an interesting possibility.

- Financial Condition is Strong: Scoring 8/10 for condition, Cabot keeps a stable balance sheet. The company has been lowering its share count over time—a positive in Lynch's opinion—and its Altman-Z score shows no near-term bankruptcy risk. The debt level, while existing, is seen as manageable.

- Growth Shows a Varied Picture: This is the area where Cabot displays some difference from a pure growth story, scoring only 3/10. While its 5-year EPS growth is good, recent yearly results have weakened, and future growth projections are moderate. For a GARP investor, this highlights the importance of the "reasonable price" part of the method, the low valuation may already reflect this slower growth view.

A more detailed look at these fundamental elements is provided in the full fundamental analysis report for Cabot Corp.

Summary and Next Steps

For an investor using a Peter Lynch-inspired GARP method, Cabot Corp offers an interesting example. The company meets strict filters for historical growth rate, valuation (through the PEG ratio), profitability, and financial condition. Its fundamental picture is supported by excellent profitability and a low valuation, though with recognized near-term growth challenges. This mix—a historically good performer trading at a notable discount to its own growth history—is exactly what the method aims to find.

It is important to remember that a filter is only a first step for investigation. Lynch himself emphasized the need to know the business behind the numbers. Interested investors should look more closely into Cabot's two parts—Reinforcement Materials and Performance Chemicals—its competitive standing, and the cyclical nature of the specialty chemicals industry.

Cabot Corp is one of multiple companies that currently meet this disciplined investment filter. You can locate more possible candidates by viewing the live Peter Lynch Strategy screen.

Disclaimer: This article is for information only and does not form financial advice, a suggestion to buy or sell any security, or an offer to give investment advisory services. All investment choices carry risk, including the possible loss of principal. Readers should do their own complete investigation and think about their personal financial situation before making any investment choices.