In the search for long-term investment opportunities, the principles laid out by legendary investor Peter Lynch continue to offer a useful roadmap. His strategy, often categorized as Growth at a Reasonable Price (GARP), focuses on finding companies that show strong, sustainable growth while trading at valuations that do not overpay for that potential. The core filters of a Lynch-inspired screen usually look for a history of solid earnings per share (EPS) growth, a sensible valuation when adjusted for that growth (the PEG ratio), strong profitability (Return on Equity), and a good balance sheet with manageable debt. This methodical approach tries to find businesses that are both doing well and financially stable, offering a margin of safety for the patient investor.

One company that recently appeared from such a screen is CARGURUS INC (NASDAQ:CARG), the Boston-based operator of an online automotive marketplace. For investors aligned with Lynch's philosophy, CarGurus presents a noteworthy case study in how a modern digital platform can fit with classic fundamental investment criteria.

A Good Track Record of Profitability and Growth

Central to Lynch's strategy is finding companies that have shown an ability to grow earnings consistently, but not at an unsustainable, extreme pace. CarGurus seems to meet this balance. The company's earnings per share have grown at an average yearly rate of about 26.7% over the past five years. This is a solid figure that easily goes beyond Lynch's typical minimum of 15%, yet stays below the 30% limit he suggested might be unsustainable for the long term. This history indicates the company has effectively scaled its operations and monetized its platform over time.

Furthermore, the company's profitability numbers are very strong, a key sign of business quality and efficient management. CarGurus has a Return on Equity (ROE) of 40.5%, well above the 15% minimum often used in Lynch screens. A high ROE shows that the company is producing significant profit from the equity shareholders have invested, a mark of a fundamentally efficient and profitable business.

Valuation: Paying a Sensible Price for Growth

Perhaps the most important Lynch filter is the PEG ratio, which compares a stock's Price-to-Earnings (P/E) ratio to its earnings growth rate. The aim is to find stocks where the P/E is not too high relative to the growth available. CarGurus's PEG ratio, based on its past five-year growth, is about 0.58. A PEG ratio below 1.0 is usually seen as good under the Lynch framework, suggesting the market may be pricing the company's growth path too low. This provides the "reasonable price" part of the GARP strategy, offering a possible margin of safety for investors.

Financial Health: A Strong Balance Sheet

Lynch stressed the importance of a good financial foundation to handle economic downturns and pay for future growth. CarGurus does well in this area, showing balance sheet strength that would likely gain his agreement.

- Zero Debt: The company has no debt, resulting in a Debt/Equity ratio of 0. This removes interest expense risk and gives great financial flexibility.

- Good Liquidity: With a Current Ratio of 2.87, CarGurus holds almost three times more current assets than current liabilities. This shows a solid ability to meet short-term obligations and put money into operations without difficulty.

- Shareholder-Friendly Actions: The company has been lowering its share count over the past one and five years, a practice Lynch liked as it increases the ownership stake of each remaining shareholder.

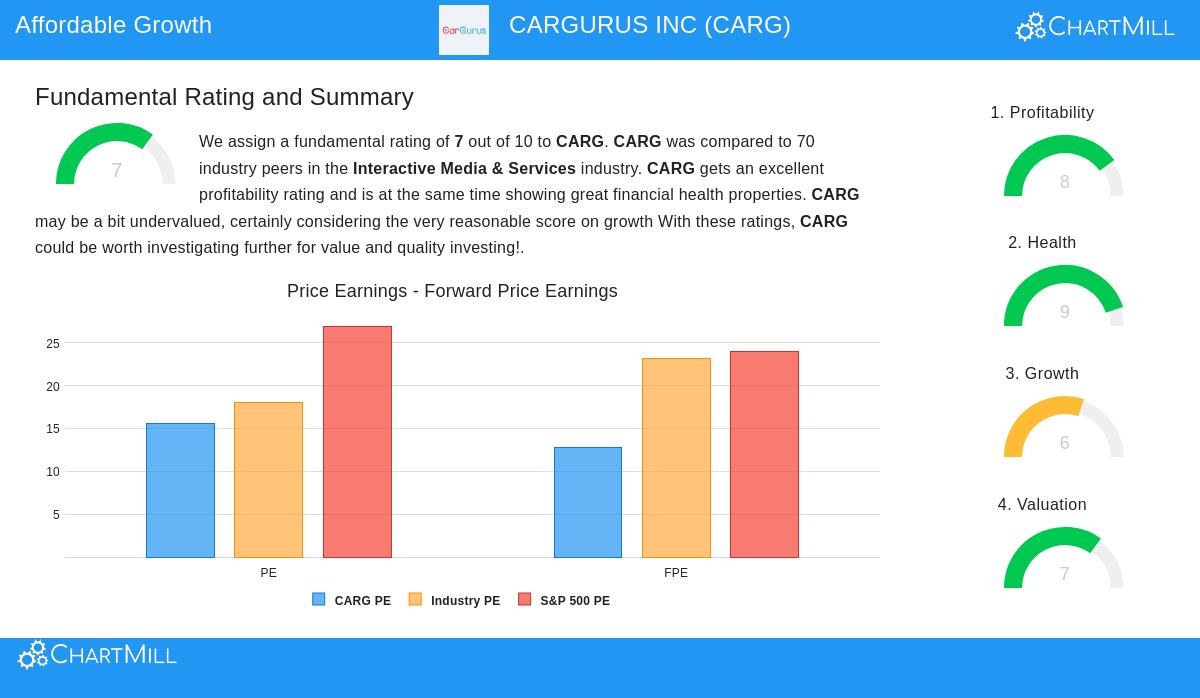

Fundamental Report Summary

A detailed fundamental analysis report on Chartmill gives CarGurus an overall score of 7 out of 10. The report notes its "excellent profitability rating" along with "great financial health properties," while also stating the stock may be "a bit undervalued." The analysis confirms the strong ROE and solid liquidity, while also pointing to a very high Return on Invested Capital (ROIC) of 23.5%. The main areas of note are a recent slowdown in revenue growth and some margin compression, factors a careful investor would want to study as part of their further research into the competitive online auto sales field.

Is CarGurus a Lynch-Style "GARP" Candidate?

Based on the quantitative filters taken from Peter Lynch's strategy, CarGurus presents a good case. It shows a history of significant, but not extreme, earnings growth (26.7% EPS 5Y). It trades at a valuation that seems sensible relative to that growth (PEG ~0.58). It is very profitable (ROE 40.5%) and operates from a position of notable financial strength with no debt and high liquidity. These are the characteristics of the type of company Lynch supported: a well-run business in a known sector, growing at a steady rate, and available at a price that doesn't assume perfection.

For investors interested in looking at other companies that pass similar methodical, growth-at-a-reasonable-price filters, you can see the complete Peter Lynch Strategy screen results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data provided and certain investment methodologies. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.